Surgery Partners’s 9.9% return over the past six months has outpaced the S&P 500 by 6.2%, and its stock price has climbed to $22.36 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Surgery Partners, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Surgery Partners Not Exciting?

Despite the momentum, we're cautious about Surgery Partners. Here are three reasons why we avoid SGRY and a stock we'd rather own.

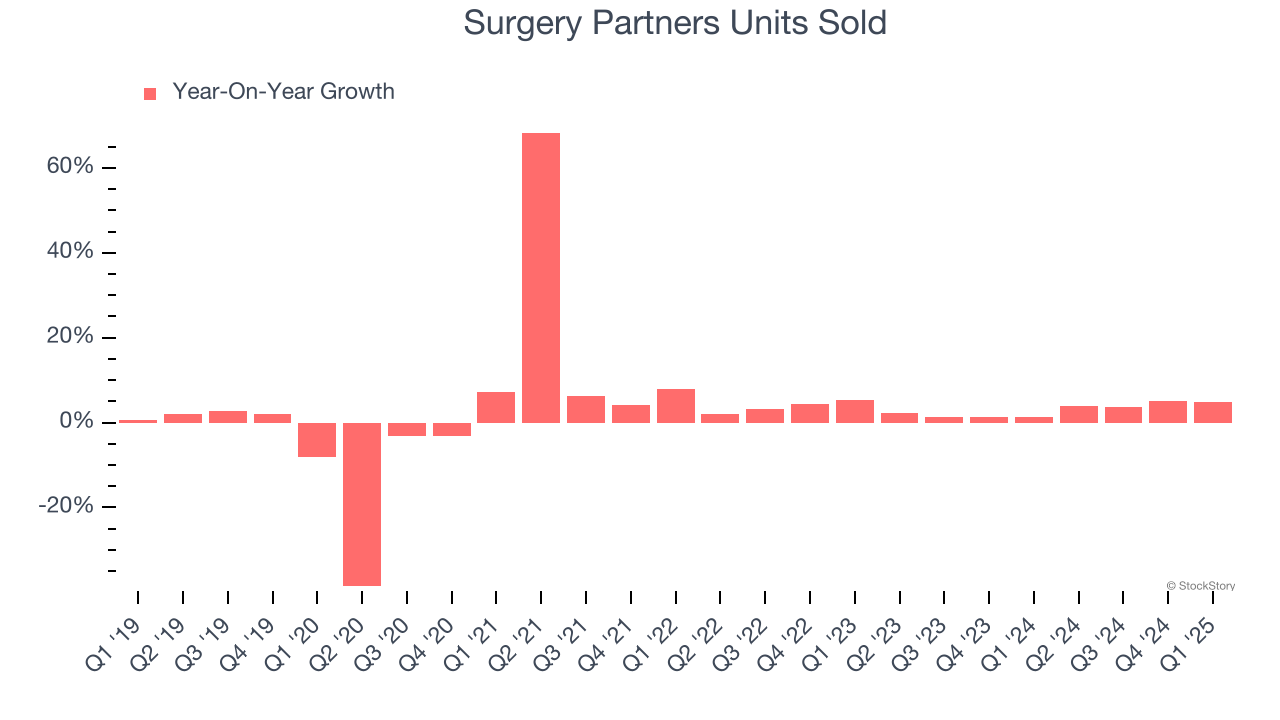

1. Weak Sales Volumes Indicate Waning Demand

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Outpatient & Specialty Care company because there’s a ceiling to what customers will pay.

Over the last two years, Surgery Partners’s units sold averaged 3% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

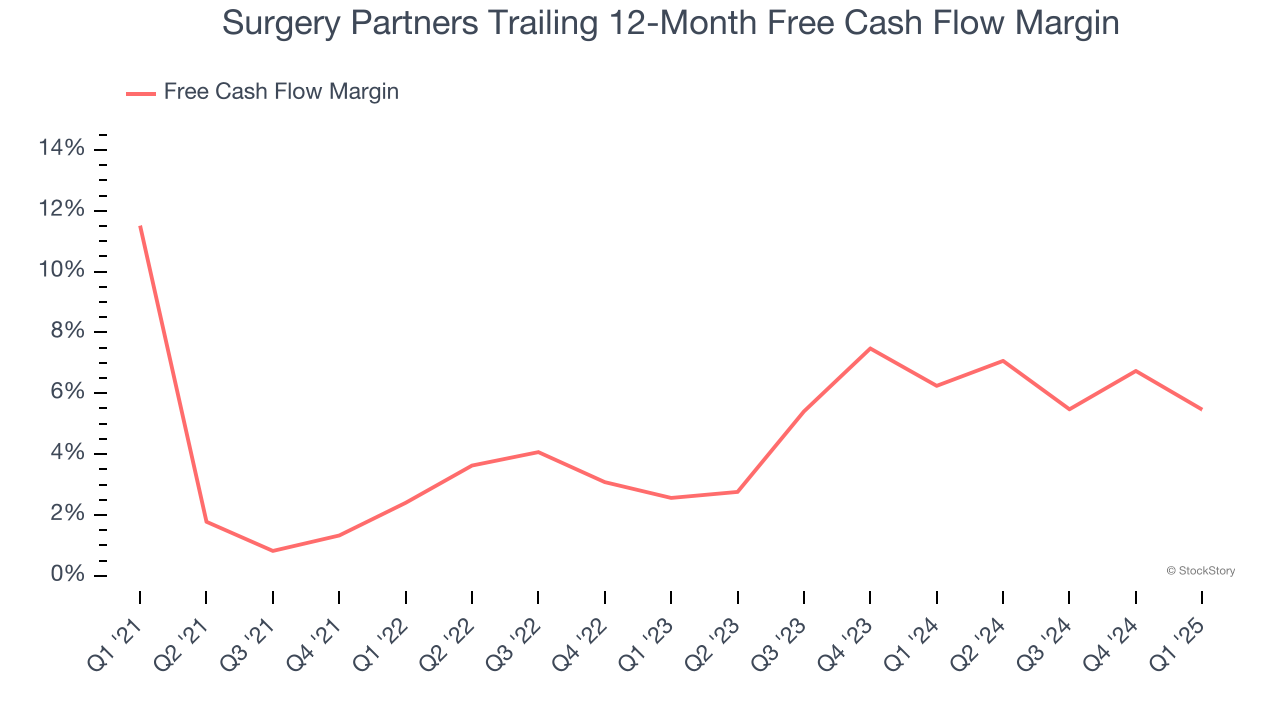

2. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Surgery Partners’s margin dropped by 6 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Surgery Partners’s free cash flow margin for the trailing 12 months was 5.5%.

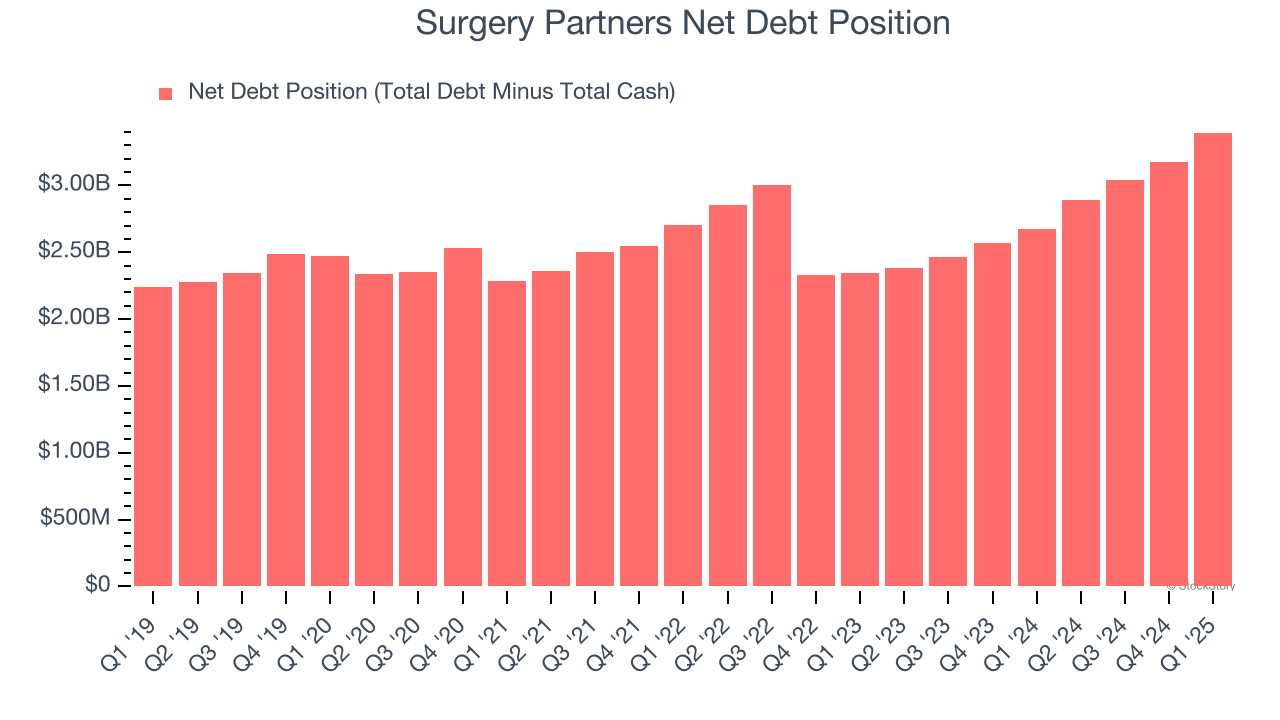

3. High Debt Levels Increase Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Surgery Partners’s $3.62 billion of debt exceeds the $229.3 million of cash on its balance sheet. Furthermore, its 7× net-debt-to-EBITDA ratio (based on its EBITDA of $514.6 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Surgery Partners could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Surgery Partners can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

Surgery Partners isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 20.5× forward P/E (or $22.36 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at our favorite semiconductor picks and shovels play.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2024 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.