Over the past six months, Mirion has been a great trade, beating the S&P 500 by 17.2%. Its stock price has climbed to $21.57, representing a healthy 20.9% increase. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is it too late to buy MIR? Find out in our full research report, it’s free.

Why Does MIR Stock Spark Debate?

With its technology protecting workers in over 130 countries and equipment used in 80% of cancer centers worldwide, Mirion Technologies (NYSE: MIR) provides radiation detection, measurement, and monitoring solutions for medical, nuclear energy, defense, and scientific research applications.

Two Things to Like:

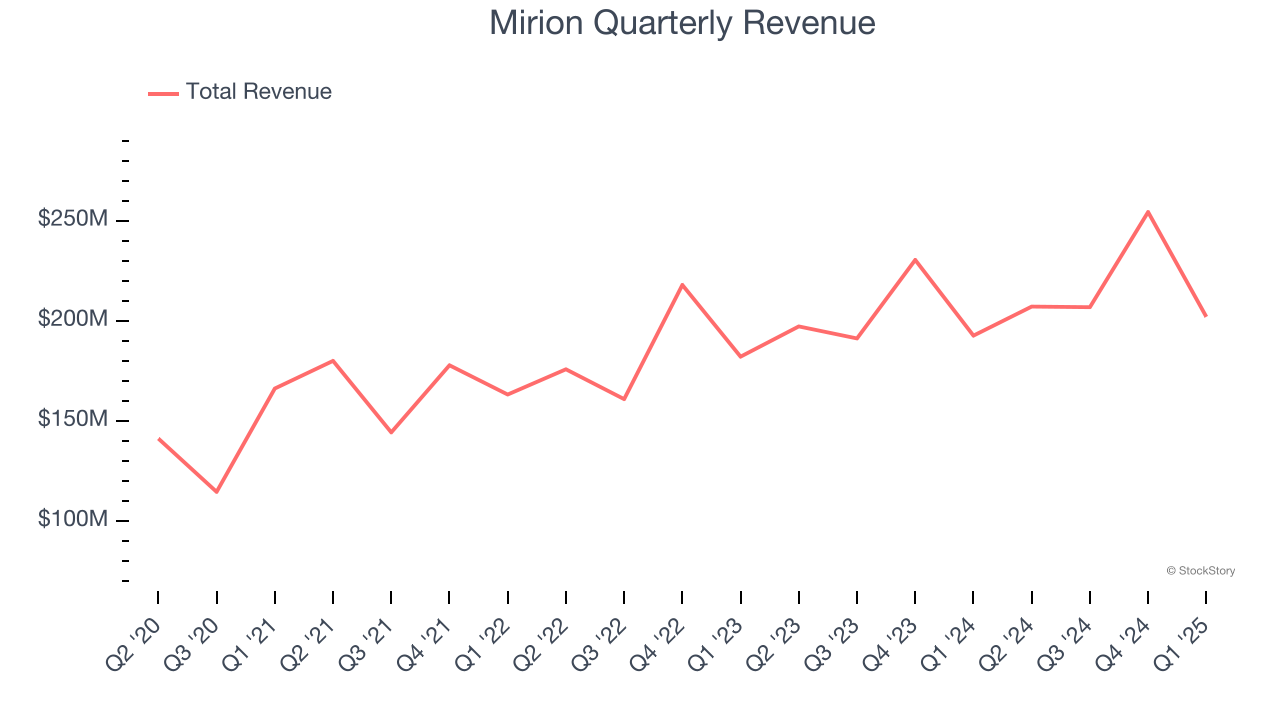

1. Skyrocketing Revenue Shows Strong Momentum

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Mirion’s sales grew at an impressive 9.9% compounded annual growth rate over the last four years. Its growth surpassed the average business services company and shows its offerings resonate with customers.

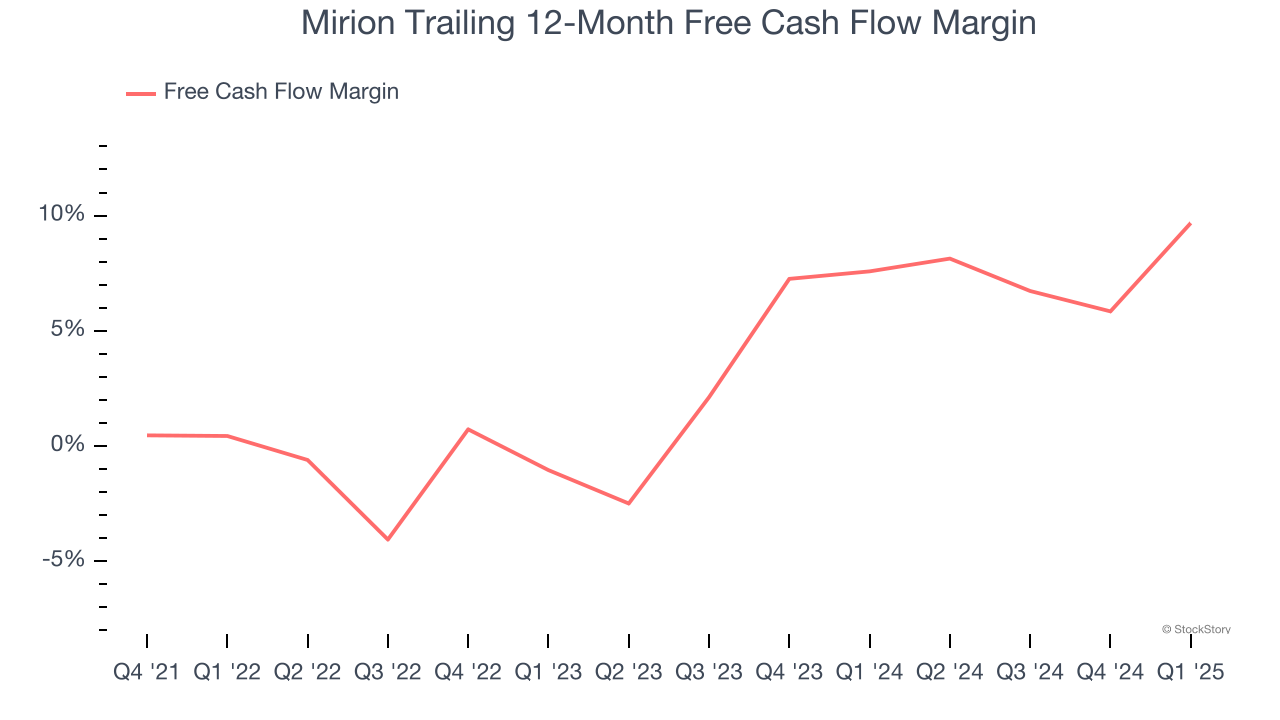

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Mirion’s margin expanded by 4.4 percentage points over the last five years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell. Mirion’s free cash flow margin for the trailing 12 months was 9.7%.

One Reason to be Careful:

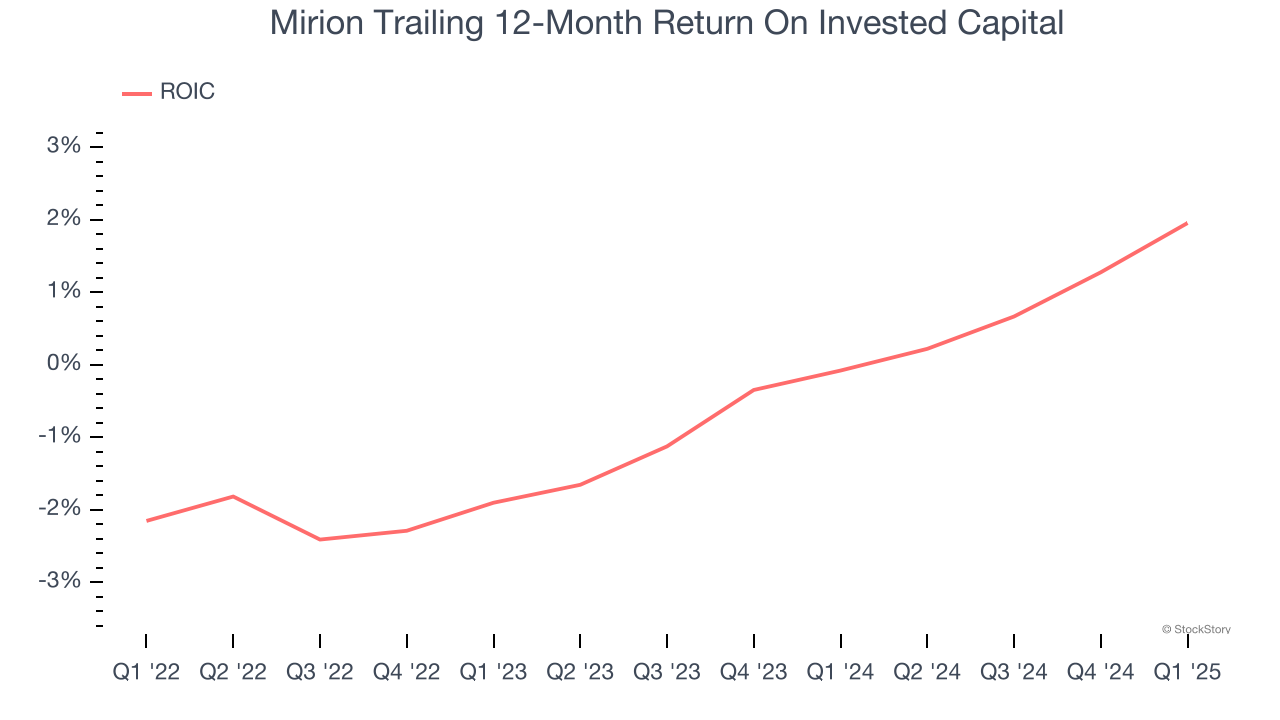

Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Mirion has shown solid business quality lately, it struggled to grow profitably in the past. Its five-year average ROIC was negative 0.5%, meaning management lost money while trying to expand the business.

Final Judgment

Mirion’s merits more than compensate for its flaws, and with its shares topping the market in recent months, the stock trades at 28× forward EV-to-EBITDA (or $21.57 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2024 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.