What a brutal six months it’s been for Reynolds. The stock has dropped 20.7% and now trades at $21.73, rattling many shareholders. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Reynolds, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Reynolds Will Underperform?

Even though the stock has become cheaper, we're swiping left on Reynolds for now. Here are three reasons why you should be careful with REYN and a stock we'd rather own.

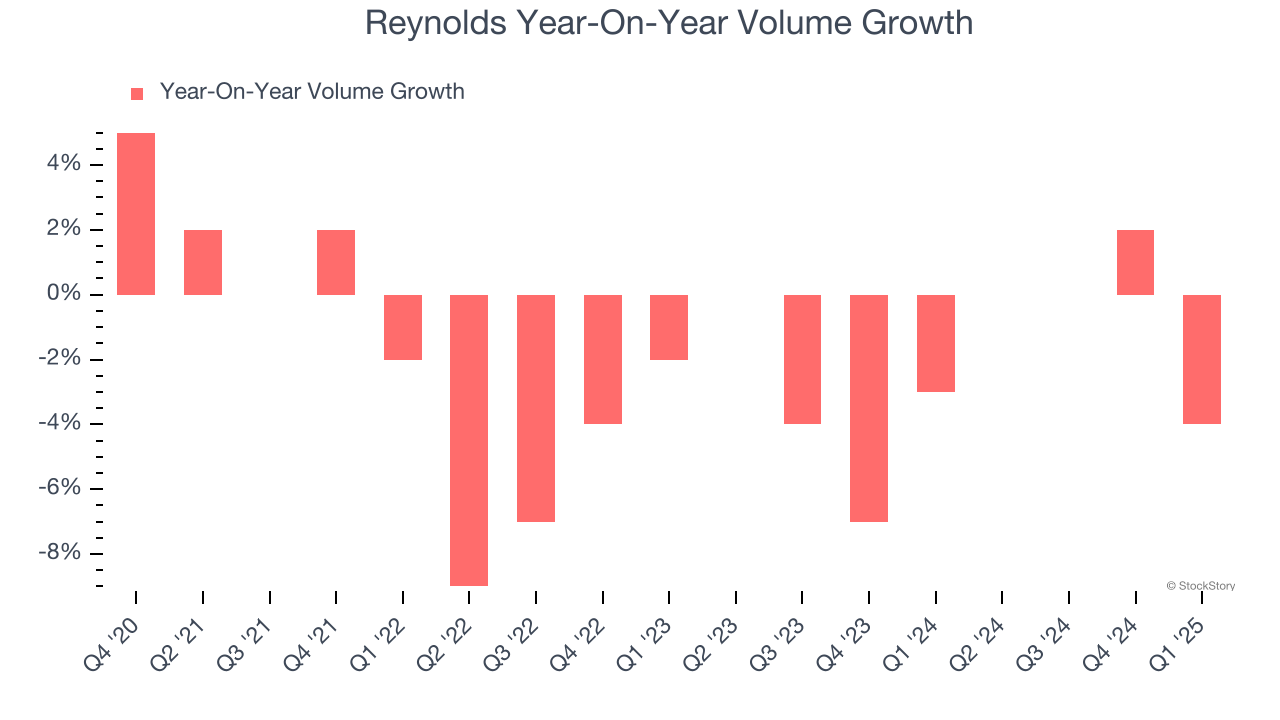

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Reynolds’s average quarterly sales volumes have shrunk by 2% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Reynolds’s revenue to drop by 1.4%, a decrease from This projection doesn't excite us and indicates its products will face some demand challenges.

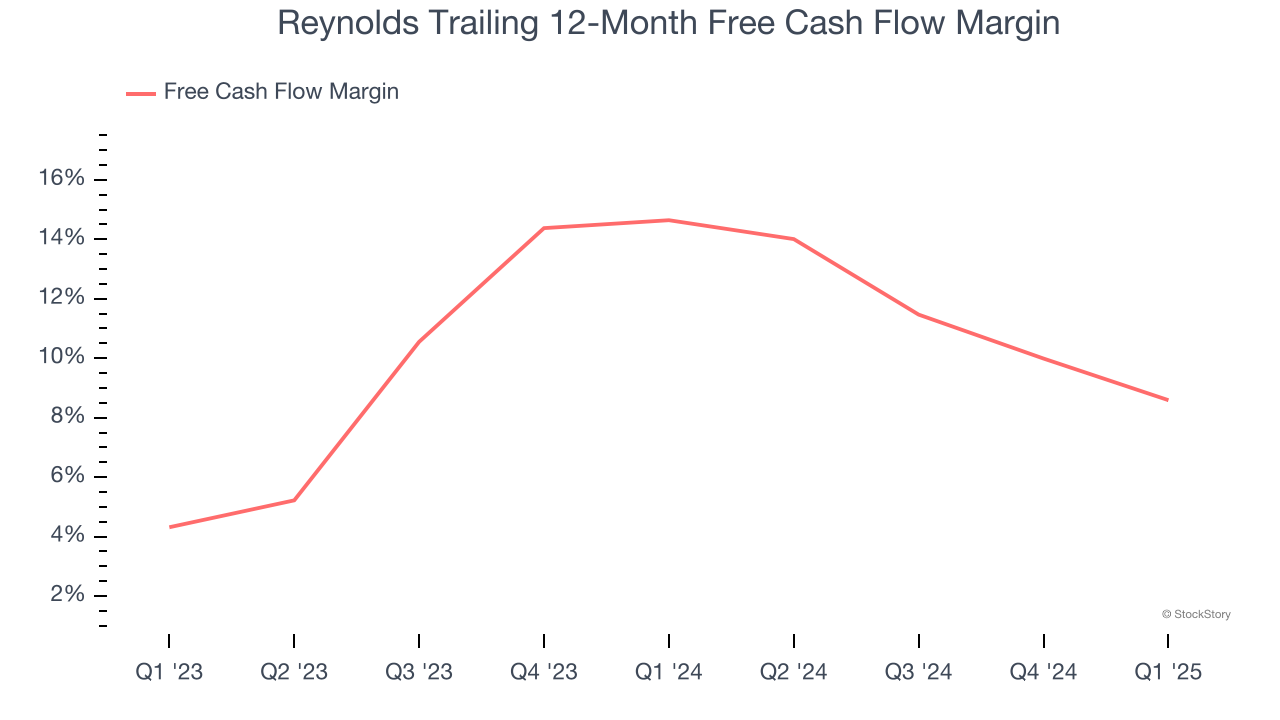

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Reynolds’s margin dropped by 6.1 percentage points over the last year. This decrease warrants extra caution because Reynolds failed to grow its revenue organically. Its cash profitability could decay further if it tries to reignite growth through investments.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Reynolds, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 13.2× forward P/E (or $21.73 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Reynolds

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.