Since July 2020, the S&P 500 has delivered a total return of 93.1%. But one standout stock has more than doubled the market - over the past five years, Hartford has surged 195% to $122.86 per share. Its momentum hasn’t stopped as it’s also gained 9.7% in the last six months, beating the S&P by 5.6%.

Is now the time to buy Hartford, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Hartford Not Exciting?

We’re happy investors have made money, but we're sitting this one out for now. Here are three reasons why we avoid HIG and a stock we'd rather own.

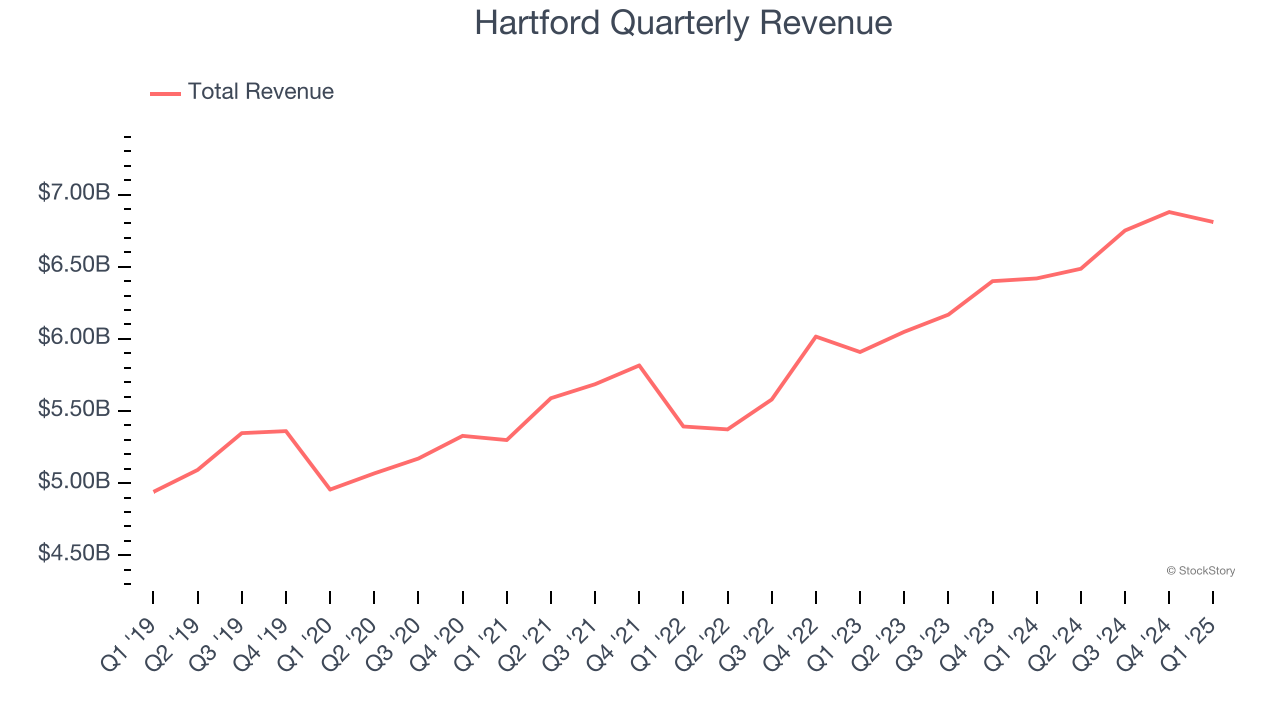

1. Long-Term Revenue Growth Disappoints

Insurers earn revenue three ways. The core insurance business itself, often called underwriting and represented in the income statement as premiums earned, is one way. Investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities is the second way. Fees from various sources such as policy administration, annuities, or other value-added services is the third.

Regrettably, Hartford’s revenue grew at a tepid 5.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the insurance sector.

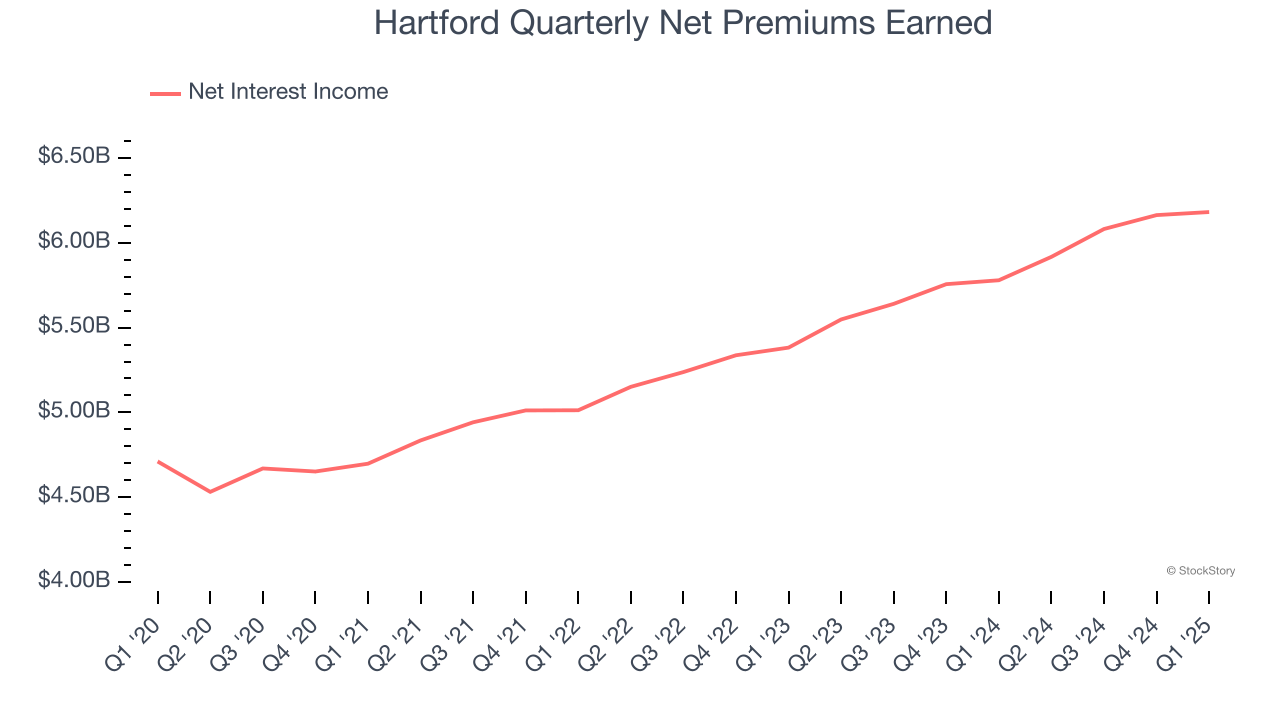

2. Net Premiums Earned Points to Soft Demand

Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

Hartford’s net premiums earned has grown at a 7% annualized rate over the last four years, slightly worse than the broader insurance industry.

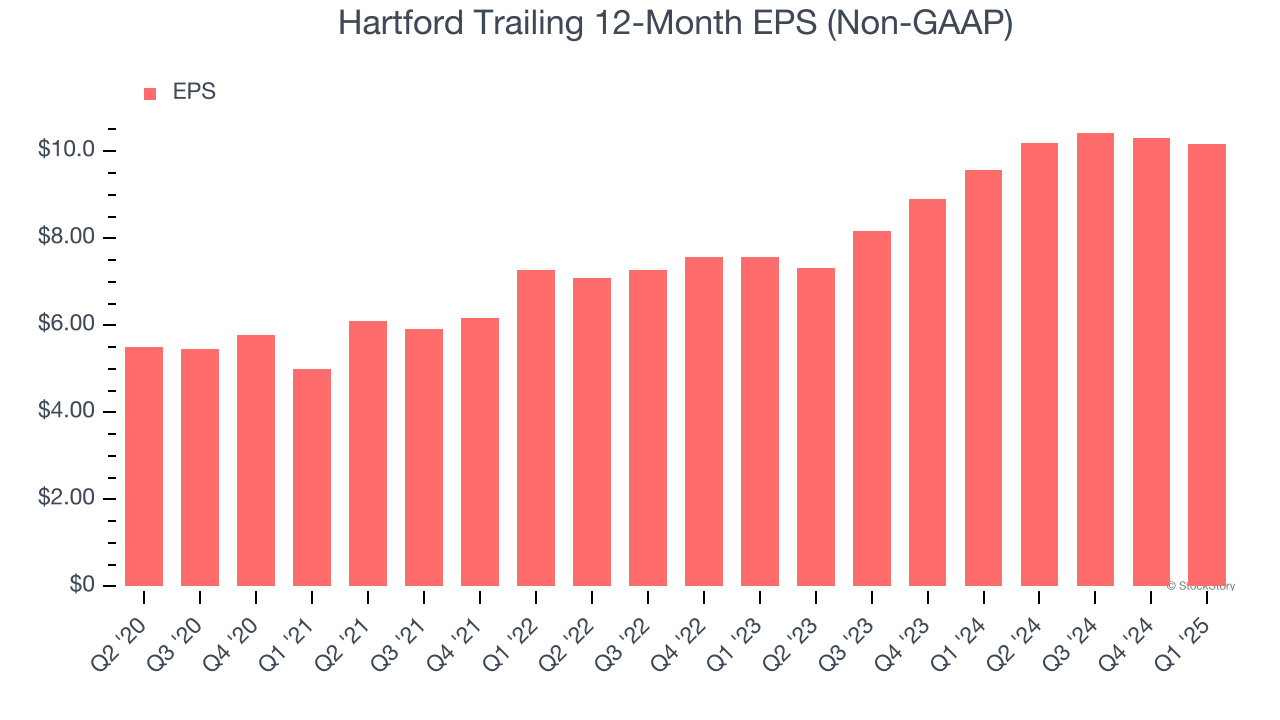

3. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Hartford’s EPS grew at an unimpressive 15.8% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 8.5% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

Hartford isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 2× forward P/B (or $122.86 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. Let us point you toward the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Hartford

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.