Shareholders of Under Armour would probably like to forget the past six months even happened. The stock dropped 36% and now trades at $6.52. This might have investors contemplating their next move.

Is now the time to buy Under Armour, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Under Armour Will Underperform?

Despite the more favorable entry price, we don't have much confidence in Under Armour. Here are three reasons why we avoid UAA and a stock we'd rather own.

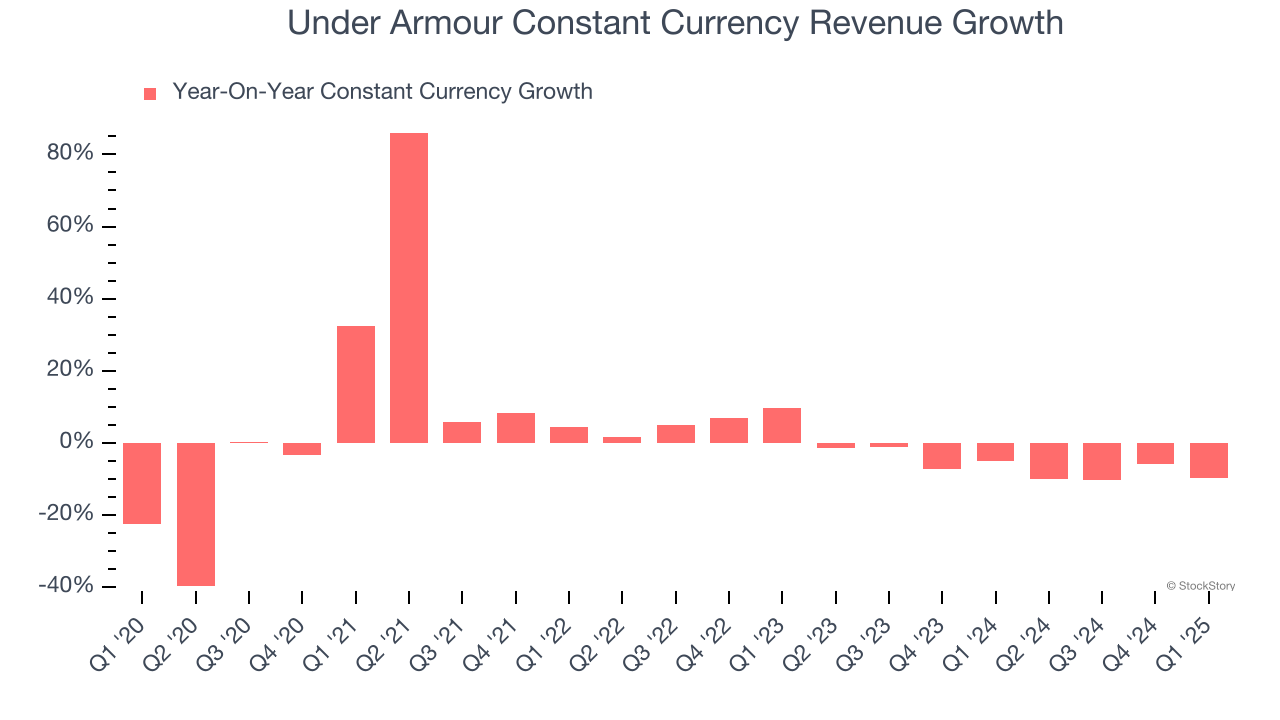

1. Declining Constant Currency Revenue, Demand Takes a Hit

Investors interested in Apparel and Accessories companies should track constant currency revenue in addition to reported revenue. This metric excludes currency movements, which are outside of Under Armour’s control and are not indicative of underlying demand.

Over the last two years, Under Armour’s constant currency revenue averaged 6.3% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Under Armour might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

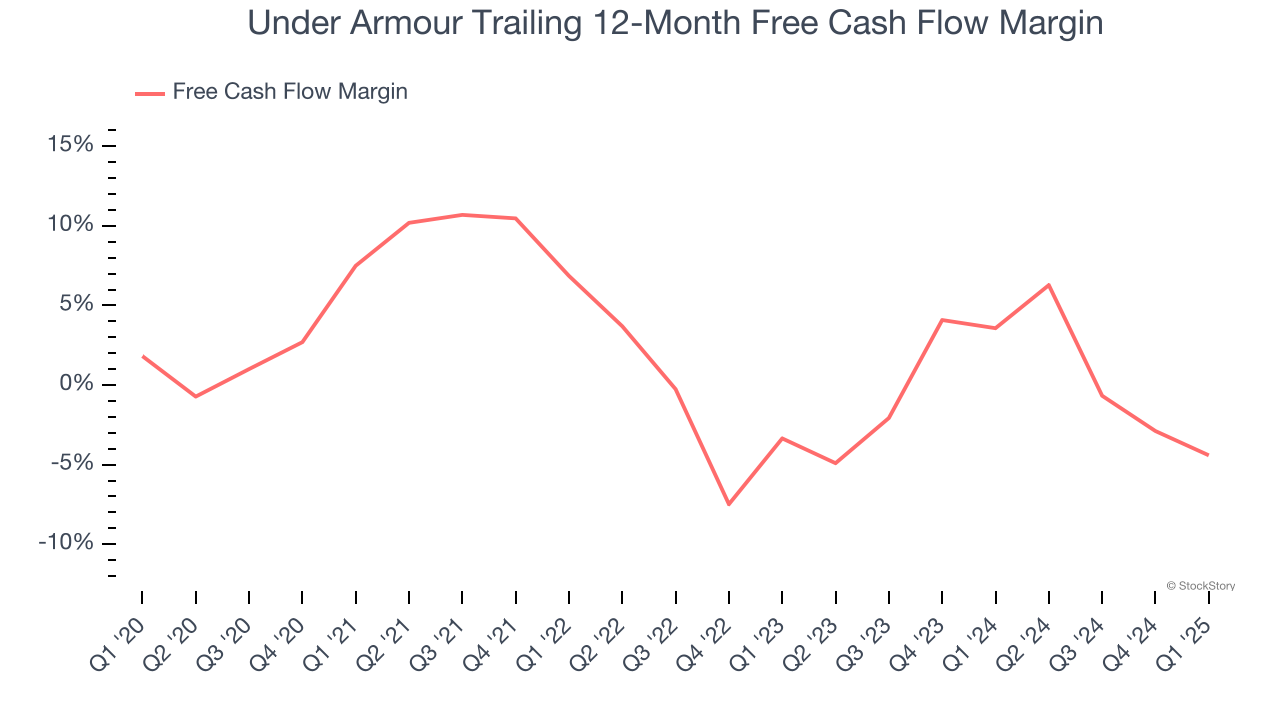

2. Breakeven Free Cash Flow Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Under Armour broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

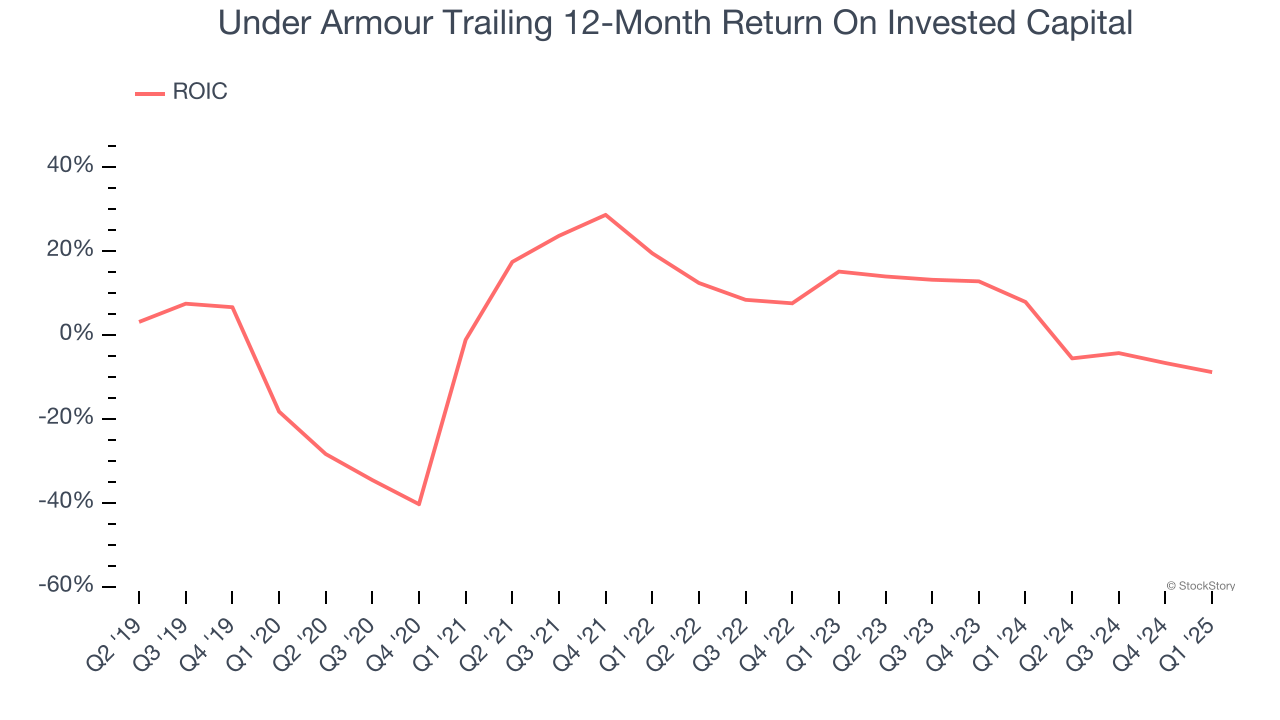

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Under Armour’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Under Armour doesn’t pass our quality test. After the recent drawdown, the stock trades at 18.6× forward P/E (or $6.52 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find better investment opportunities elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Under Armour

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.