In a sliding market, The Cheesecake Factory has defied the odds, trading up to $55.93 per share. Its 10.4% gain since November 2024 has outpaced the S&P 500’s 1.9% drop. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in The Cheesecake Factory, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is The Cheesecake Factory Not Exciting?

We’re glad investors have benefited from the price increase, but we're cautious about The Cheesecake Factory. Here are three reasons why we avoid CAKE and a stock we'd rather own.

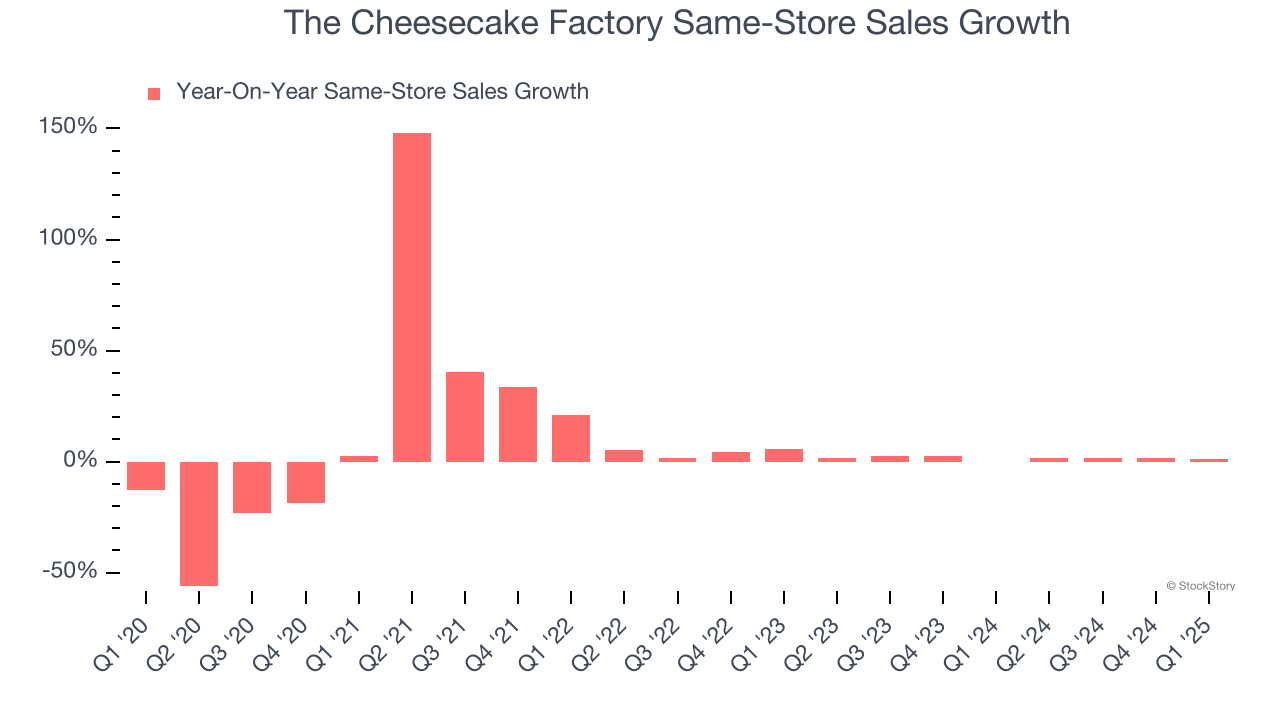

1. Same-Store Sales Falling Behind Peers

Same-store sales show the change in sales at restaurants open for at least a year. This is a key performance indicator because it measures organic growth.

The Cheesecake Factory’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.6% per year.

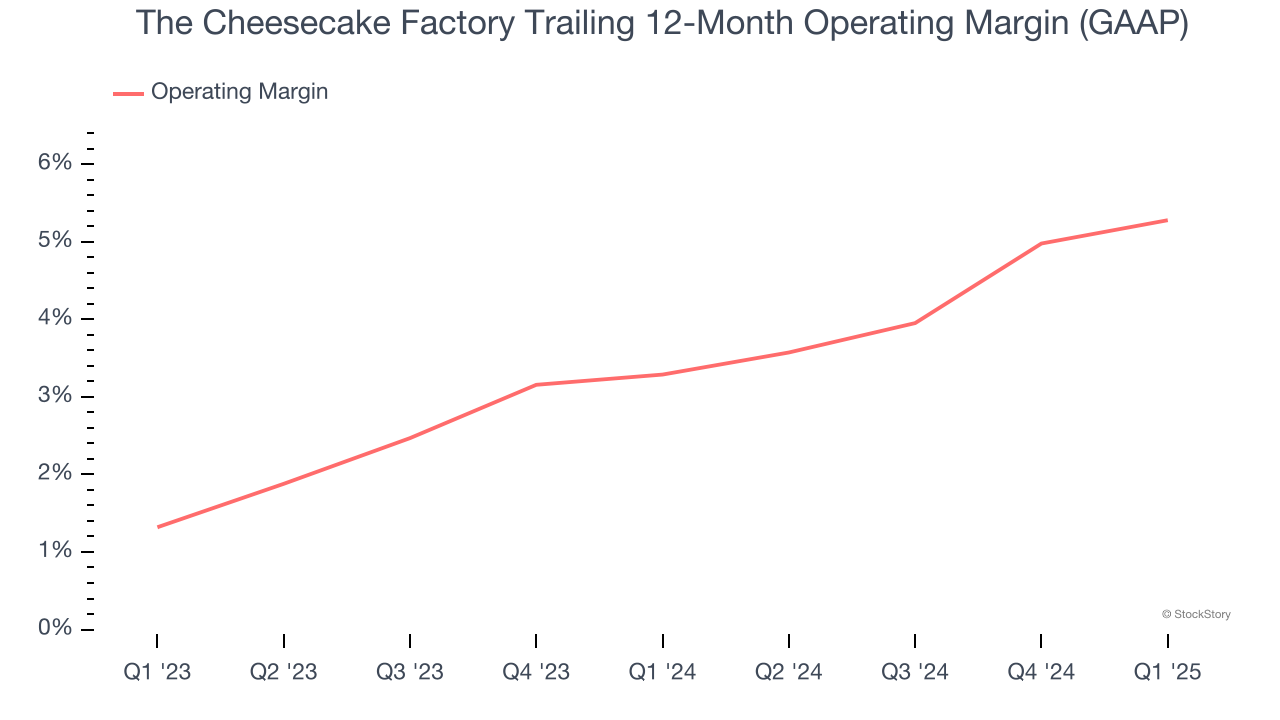

2. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

The Cheesecake Factory was profitable over the last two years but held back by its large cost base. Its average operating margin of 4.3% was weak for a restaurant business. This result is surprising given its high gross margin as a starting point.

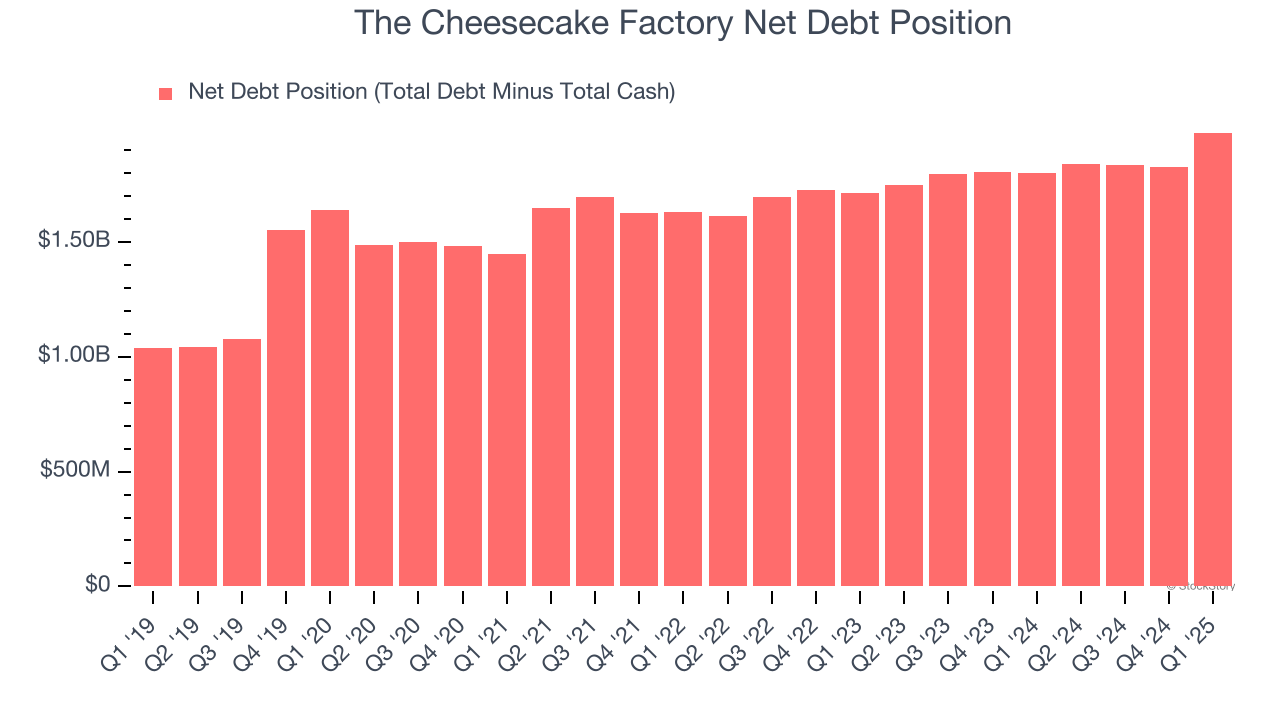

3. High Debt Levels Increase Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

The Cheesecake Factory’s $2.11 billion of debt exceeds the $135.4 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $308 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. The Cheesecake Factory could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope The Cheesecake Factory can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

The Cheesecake Factory isn’t a terrible business, but it doesn’t pass our bar. With its shares topping the market in recent months, the stock trades at 14.4× forward P/E (or $55.93 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Like More Than The Cheesecake Factory

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.