Animal health company Elanco (NYSE: ELAN) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 10.4% year on year to $1.14 billion. Guidance for next quarter’s revenue was better than expected at $1.10 billion at the midpoint, 1.9% above analysts’ estimates. Its non-GAAP profit of $0.19 per share was 43.9% above analysts’ consensus estimates.

Is now the time to buy Elanco? Find out by accessing our full research report, it’s free for active Edge members.

Elanco (ELAN) Q3 CY2025 Highlights:

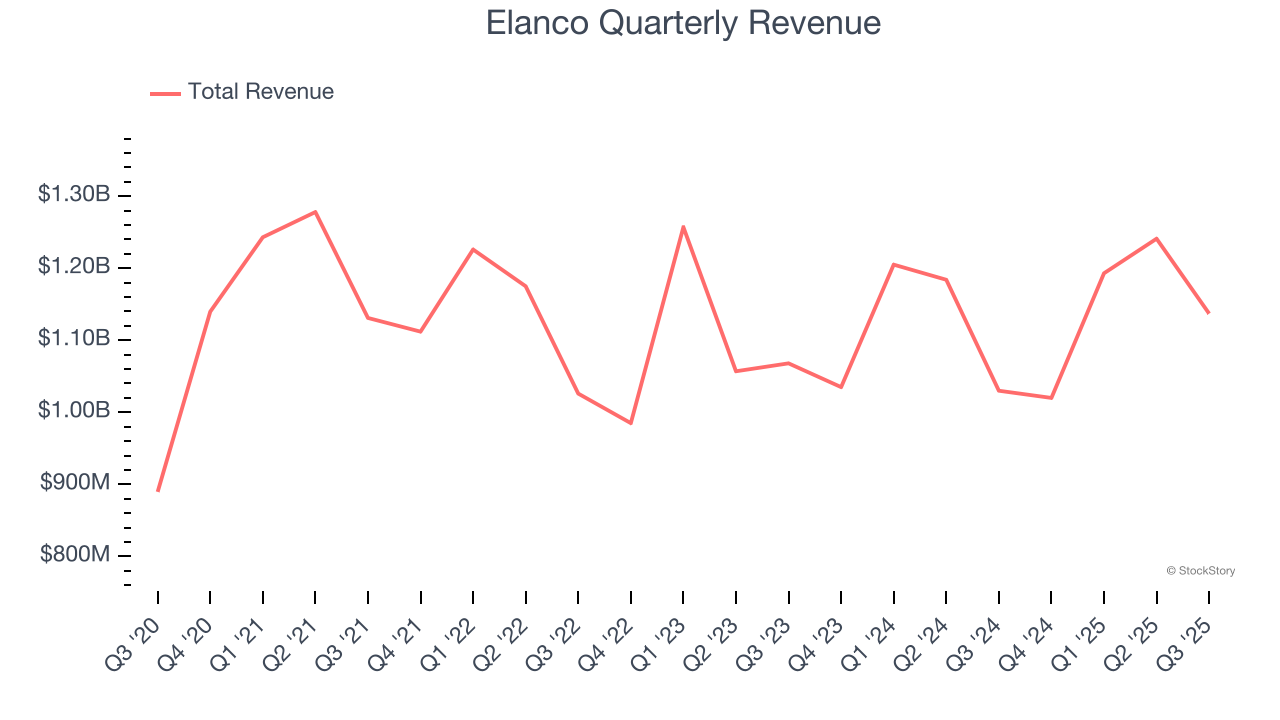

- Revenue: $1.14 billion vs analyst estimates of $1.09 billion (10.4% year-on-year growth, 4.1% beat)

- Adjusted EPS: $0.19 vs analyst estimates of $0.13 (43.9% beat)

- Adjusted EBITDA: $198 million vs analyst estimates of $173.3 million (17.4% margin, 14.3% beat)

- Revenue Guidance for Q4 CY2025 is $1.10 billion at the midpoint, above analyst estimates of $1.08 billion

- Management raised its full-year Adjusted EPS guidance to $0.93 at the midpoint, a 5.1% increase

- EBITDA guidance for the full year is $890 million at the midpoint, above analyst estimates of $874.1 million

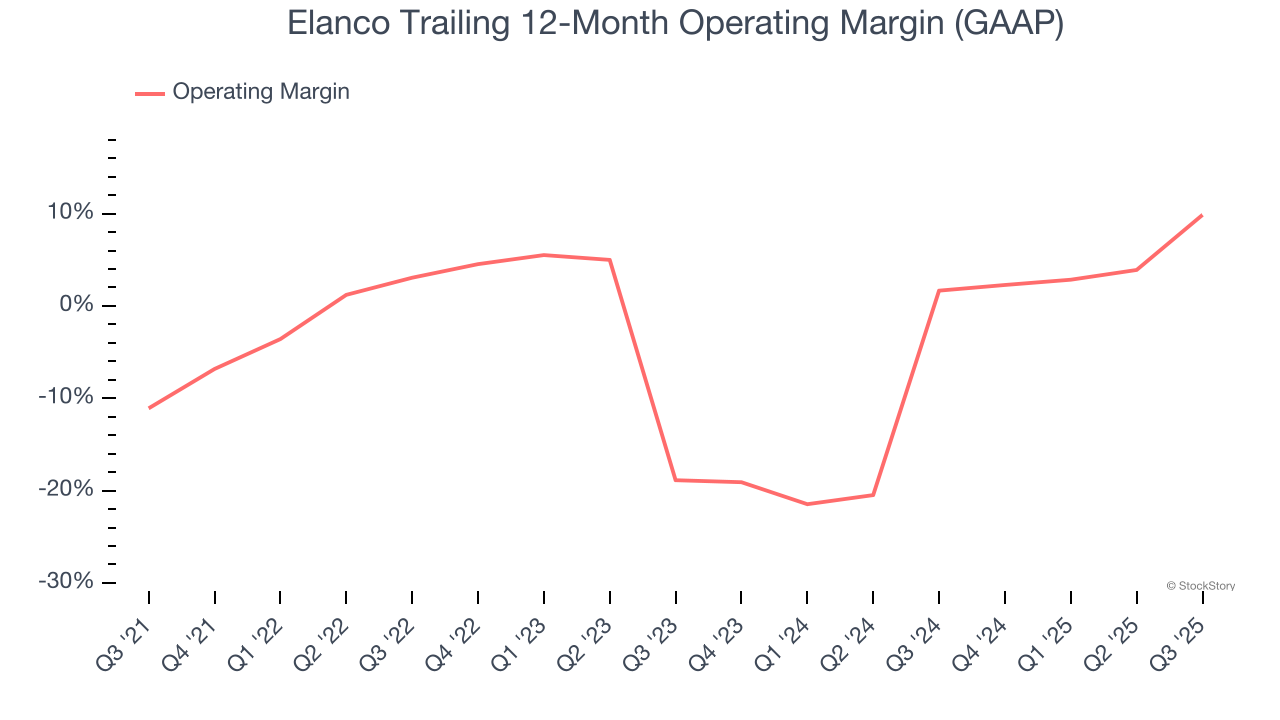

- Operating Margin: 22.5%, up from -2.1% in the same quarter last year

- Constant Currency Revenue rose 9% year on year (1% in the same quarter last year)

- Market Capitalization: $11.18 billion

"Thank you to our global team and customers as Elanco delivered strong results ahead of expectations, with an unrelenting focus on growth, innovation, and cash," said Jeff Simmons, President and CEO of Elanco.

Company Overview

Originally established as a division of pharmaceutical giant Eli Lilly before becoming independent in 2018, Elanco Animal Health (NYSE: ELAN) develops and sells medications, vaccines, and other health products for pets and farm animals across more than 90 countries.

Revenue Growth

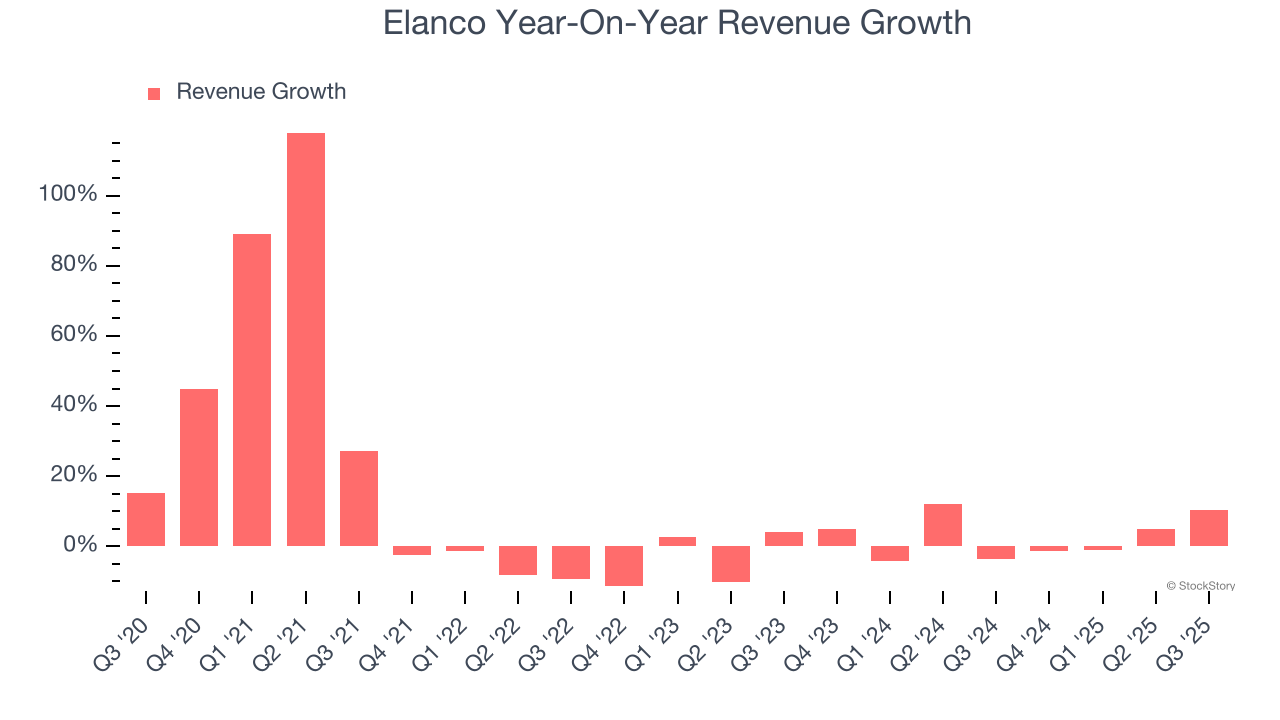

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Elanco’s 9.5% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Elanco’s recent performance shows its demand has slowed as its annualized revenue growth of 2.5% over the last two years was below its five-year trend.

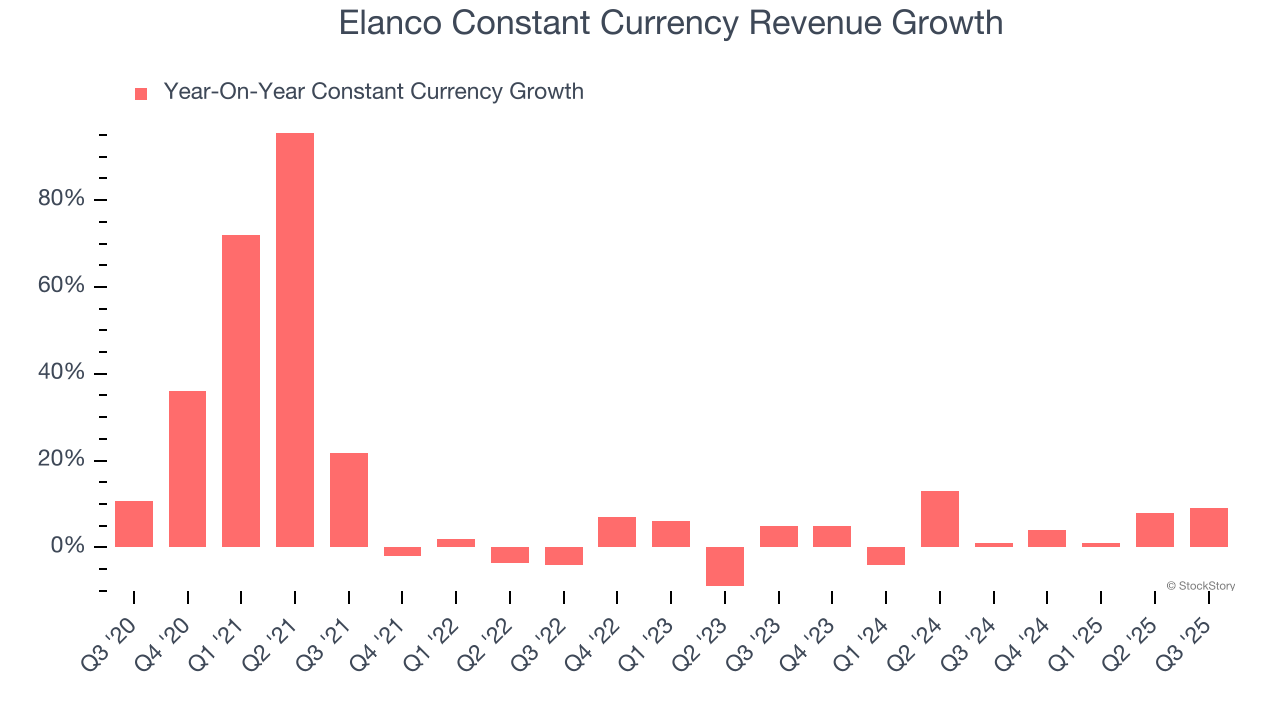

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 4.6% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Elanco.

This quarter, Elanco reported year-on-year revenue growth of 10.4%, and its $1.14 billion of revenue exceeded Wall Street’s estimates by 4.1%. Company management is currently guiding for a 7.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.3% over the next 12 months. Although this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Although Elanco was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 3% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Elanco’s operating margin rose by 20.9 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 28.7 percentage points on a two-year basis.

In Q3, Elanco generated an operating margin profit margin of 22.5%, up 24.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

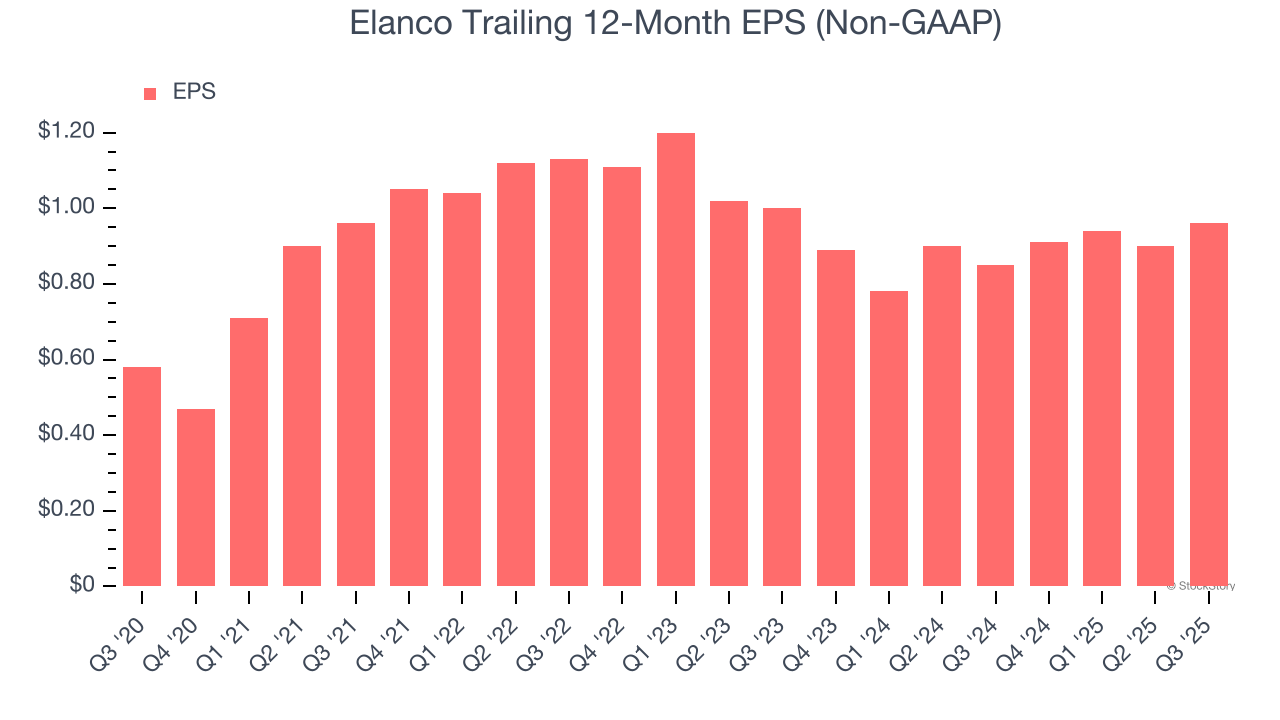

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Elanco’s remarkable 10.6% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

In Q3, Elanco reported adjusted EPS of $0.19, up from $0.13 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Elanco’s full-year EPS of $0.96 to grow 1.1%.

Key Takeaways from Elanco’s Q3 Results

We were impressed by how significantly Elanco blew past analysts’ constant currency revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this print was mixed, and guidance is weighing on the stock. Shares traded down 2.2% to $22.01 immediately after reporting.

So should you invest in Elanco right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.