Looking back on infrastructure distributors stocks’ Q3 earnings, we examine this quarter’s best and worst performers, including MRC Global (NYSE: MRC) and its peers.

Focusing on narrow product categories that can lead to economies of scale, infrastructure distributors sell essential goods that often enjoy more predictable revenue streams. For example, the ongoing inspection, maintenance, and replacement of pipes and water pumps are critical to a functioning society, rendering them non-discretionary. Lately, innovation to address trends like water conservation has driven incremental sales. But like the broader industrials sector, infrastructure distributors are also at the whim of economic cycles as external factors like interest rates can greatly impact commercial and residential construction projects that drive demand for infrastructure products.

The 4 infrastructure distributors stocks we track reported a slower Q3. As a group, revenues missed analysts’ consensus estimates by 0.7%.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

MRC Global (NYSE: MRC)

Producing bomb casings and tracks for vehicles during WWII, MRC (NYSE: MRC) offers pipes, valves, and fitting products for various industries.

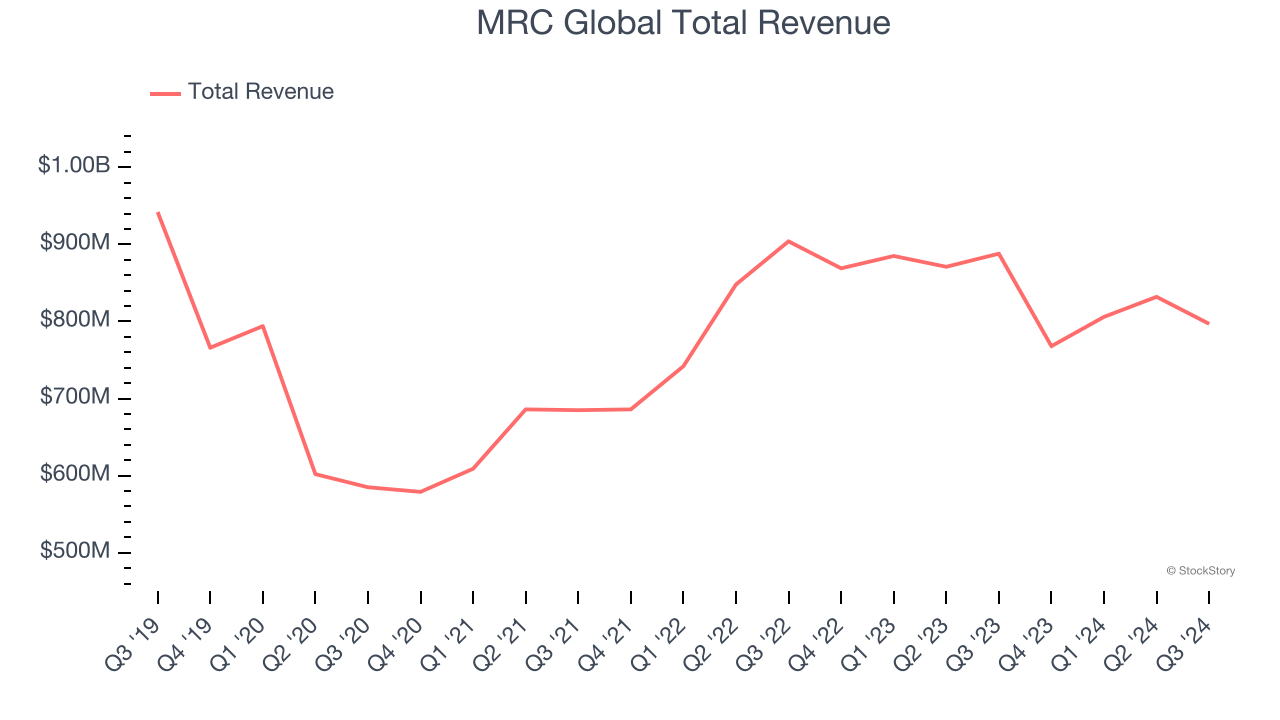

MRC Global reported revenues of $797 million, down 10.2% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with a solid beat of analysts’ EPS estimates but a significant miss of analysts’ adjusted operating income estimates.

Rob Saltiel, MRC Global’s President and CEO, stated, “As we guided on our last earnings call, revenue and Adjusted EBITDA declined in the third quarter due to slowing activity in the U.S. oilfield and project delays in our DIET sector. Despite these headwinds, we generated operating cash flow of $96 million, bringing our 2024 total to $197 million, essentially achieving our full year cash flow target of $200 million a quarter early. Given our robust cash flow generation, we are raising our guidance for the full year operating cash flow to $220 million or more.

MRC Global delivered the slowest revenue growth of the whole group. The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $12.59.

Read our full report on MRC Global here, it’s free.

Best Q3: Core & Main (NYSE: CNM)

Formerly a division of industrial distributor HD Supply, Core & Main (NYSE: CNM) is a provider of water, wastewater, and fire protection products and services.

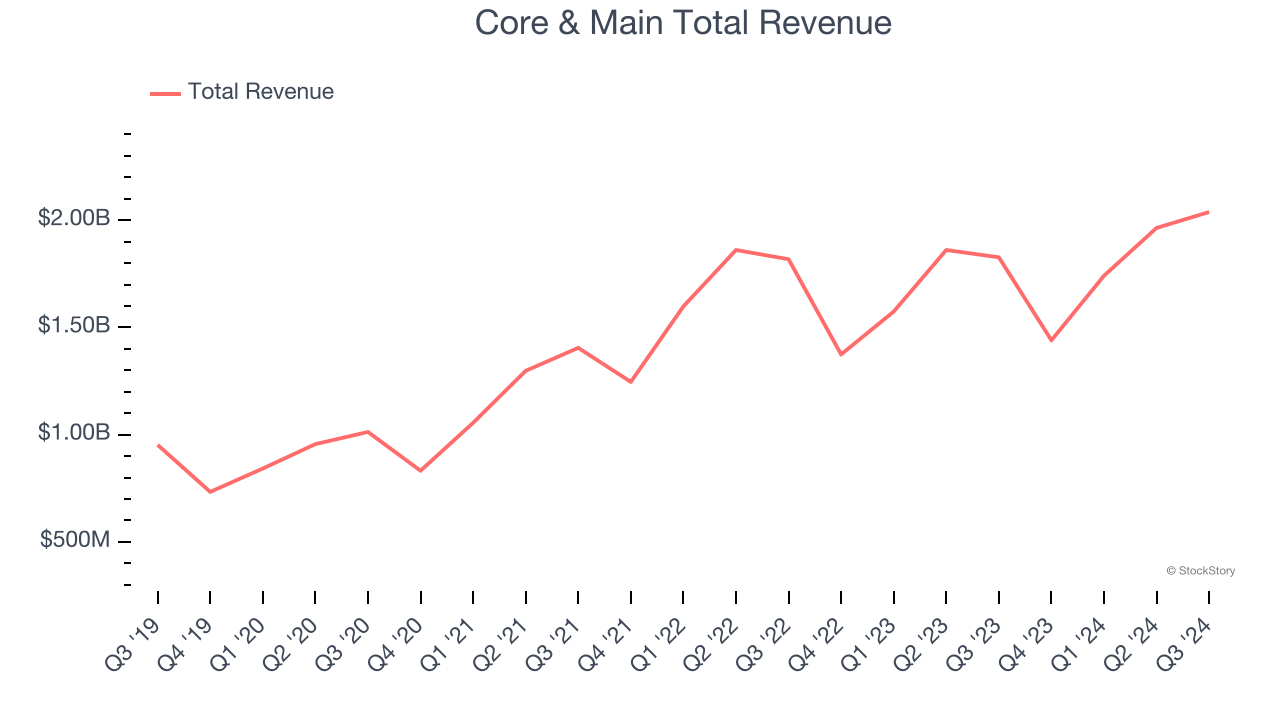

Core & Main reported revenues of $2.04 billion, up 11.5% year on year, outperforming analysts’ expectations by 2.3%. The business had a very strong quarter with an impressive beat of analysts’ organic revenue and adjusted operating income estimates.

Core & Main achieved the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 5.1% since reporting. It currently trades at $50.77.

Is now the time to buy Core & Main? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Watsco (NYSE: WSO)

Originally a manufacturing company, Watsco (NYSE: WSO) today only distributes air conditioning, heating, and refrigeration equipment, as well as related parts and supplies.

Watsco reported revenues of $2.16 billion, up 1.6% year on year, falling short of analysts’ expectations by 3.6%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

Watsco delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 1% since the results and currently trades at $479.80.

Read our full analysis of Watsco’s results here.

DistributionNOW (NYSE: DNOW)

Spun off from National Oilwell Varco, DistributionNOW (NYSE: DNOW) provides distribution and supply chain solutions for the energy and industrial end markets.

DistributionNOW reported revenues of $606 million, up 3.1% year on year. This print missed analysts’ expectations by 1.5%. It was a slower quarter as it also recorded a miss of analysts’ EBITDA and EPS estimates.

The stock is down 6.1% since reporting and currently trades at $12.91.

Read our full, actionable report on DistributionNOW here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% each in November and December), and a notable surge followed Donald Trump's presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by the pace and magnitude of future rate cuts as well as potential changes in trade policy and corporate taxes once the Trump administration takes over. The path forward is marked by uncertainty.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.