After a bruising stretch on Wall Street, Pinterest (PINS) has finally caught a break. The visual discovery platform saw its stock surge more than 9% on Mar. 3, followed by another 1.5% gain on Mar. 4, after reports surfaced that the legendary activist investor firm Elliott Investment Management had taken a significant position in the company. Elliott, known for pushing companies to unlock shareholder value, has built a $1 billion stake in Pinterest.

The investment is expected to support the company’s capital return strategy, with funds likely being funneled into accelerated share repurchases under Pinterest’s existing $3.5 billion buyback authorization. Marc Steinberg, an Elliott partner who already sits on Pinterest’s board, expressed strong confidence in the company’s future. He described Elliott as a “steadfast supporter” since its initial investment in 2022 and emphasized that the firm sees substantial long-term opportunity ahead for Pinterest.

The timing of this move is hardly random. Pinterest has endured a challenging few months, warning that revenue growth in the first quarter would slow as large retailers trimmed advertising spending to protect margins amid tariff pressures. In January, the company also announced plans to cut roughly 700 jobs, around 15% of its workforce, describing the layoffs as part of a broader effort to redirect resources toward artificial intelligence (AI) initiatives.

At the same time, the platform is grappling with rising competition from AI chatbots, another factor that has weighed on the stock in recent months. Given these challenges, Elliott’s sizable investment appears to be a clear vote of confidence in the company’s long-term potential. With that backdrop in mind, here’s a closer look at the stock.

About Pinterest Stock

Founded in 2010, Pinterest has built its identity as a visual search and discovery platform where users gather ideas, plan projects, and explore products they may want to buy. The platform aims to create an inspiration-focused online space, allowing people to browse and save visual content ranging from home décor and fashion to travel and recipes.

Over the years, the California-based company has grown into a massive global network, now reaching close to 600 million monthly active users worldwide and positioning itself as a key destination where creativity and online commerce intersect. Yet, despite this broad user base, the company’s stock performance has struggled to gain traction on Wall Street.

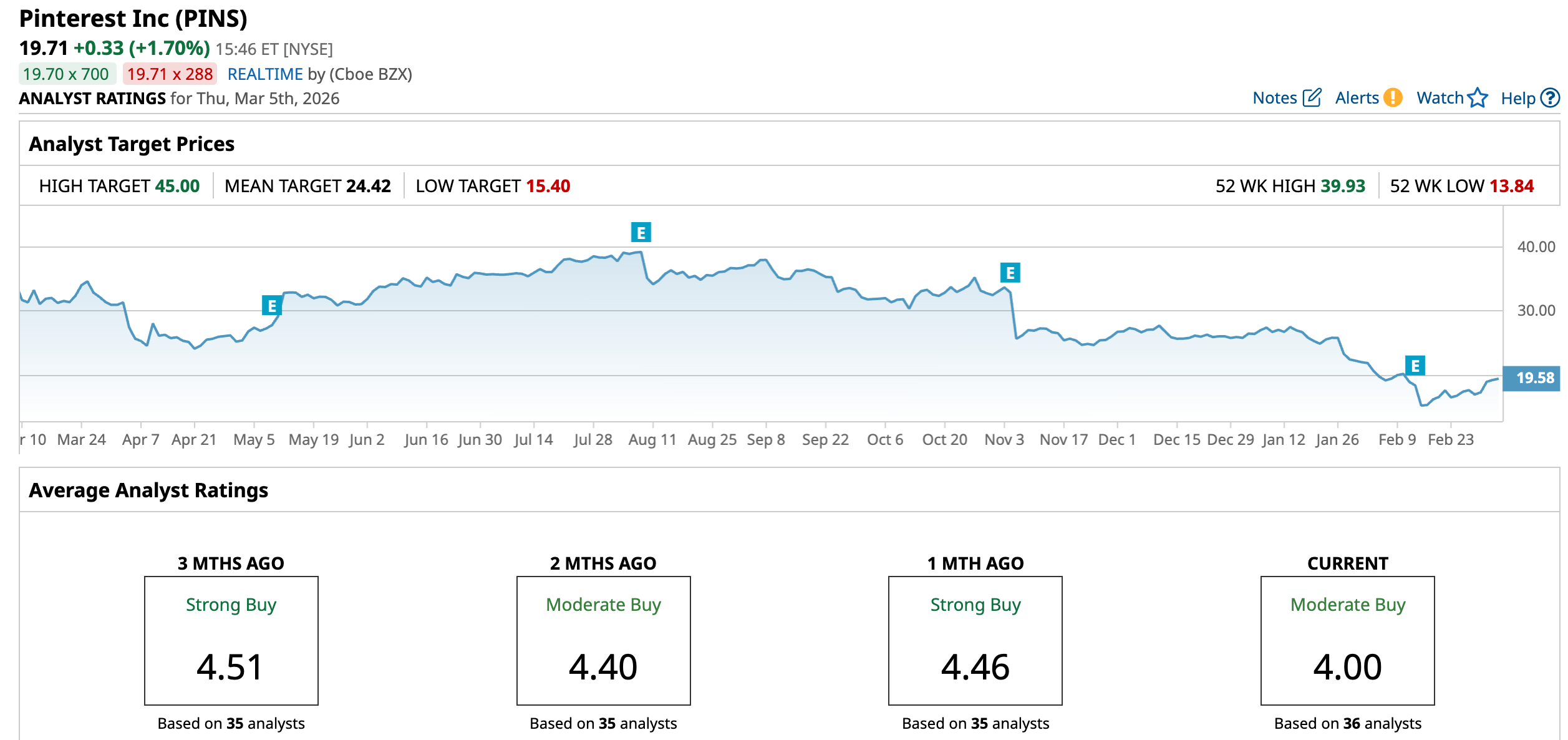

With a market capitalization of roughly $12.9 billion, shares of Pinterest have faced persistent pressure in recent months. The weakness reflects a combination of factors, including softer financial guidance, tariff-related challenges that have weighed on advertising spending, and quarterly results that have failed to fully impress investors.

At the same time, the company is navigating a more competitive digital landscape. The rise of AI-integrated platforms and the dominance of social media heavyweights such as TikTok and Instagram have intensified the battle for user engagement and advertising dollars, adding another layer of pressure to Pinterest’s growth narrative. Shares of Pinterest have taken a beating over the past year. The stock has tumbled about 46% over the past year and remains down roughly 24.6% so far in 2026.

In contrast, the broader S&P 500 Index ($SPX) has held up far better, climbing around 16% over the past year and declining marginally in 2026. However, sentiment around Pinterest has started to shift. With Elliott Investment Management now entering the picture, the stock has staged a noticeable rebound, jumping nearly 9.57% over the past five trading sessions as Wall Street reacts to the activist investor’s $1 billion bet on the company.

Pinterest’s Sinks After Q4 Earnings Report

When Pinterest reported its fiscal 2025 fourth-quarter results on Feb. 12, the numbers told a somewhat mixed story. While the company continued to post solid growth, a few weak spots in the report were enough to unsettle investors. The market reaction was immediate, with the stock tumbling nearly 16.8% in the next trading session. For the quarter, revenue climbed 14% year-over-year (YOY) to $1.32 billion, though the figure came in slightly below Wall Street’s estimate of $1.33 billion.

Regional performance varied across markets. In the U.S. and Canada, revenue reached $979 million, up 9% from the prior year, supported largely by advertising demand from the retail, financial services, and telecom sectors. Europe delivered stronger growth, with revenue jumping 25% on a reported basis to $245 million. Even so, management noted that the European performance still fell short of what the company had internally anticipated.

On the profitability front, the company held up relatively well. Adjusted EBITDA increased 15% YOY to $542 million, while adjusted earnings per share rose 19.6% annually to $0.67, roughly in line with analysts’ expectations. Pinterest also maintained a strong liquidity position, ending the year with approximately $2.5 billion in cash, cash equivalents, and marketable securities.

Speaking on the earnings call, CEO Bill Ready acknowledged that the company was “not satisfied” with its fourth-quarter revenue outcome, adding that the result does not represent the level of performance Pinterest believes it can achieve over time. In addition, the CEO pointed to an external shock related to tariffs, which has weighed on advertising budgets among some of the platform’s largest retail advertisers.

Looking ahead, the company’s outlook added to investor caution. Pinterest expects fiscal first-quarter 2026 revenue to fall between $951 million and $971 million, translating to YOY growth of 11% to 14%, but still below analysts’ projections of $981.8 million. Adjusted EBITDA is expected to range from $166 million to $186 million, also missing the Street’s estimate of $205.4 million.

Even so, there was a notable bright spot in the report. The platform’s global monthly active (MAUs) users continued to expand, rising 12% YOY to a record 619 million in the fourth quarter, highlighting that user engagement remains strong even as the company navigates near-term financial headwinds.

How Are Analysts Viewing Pinterest Stock?

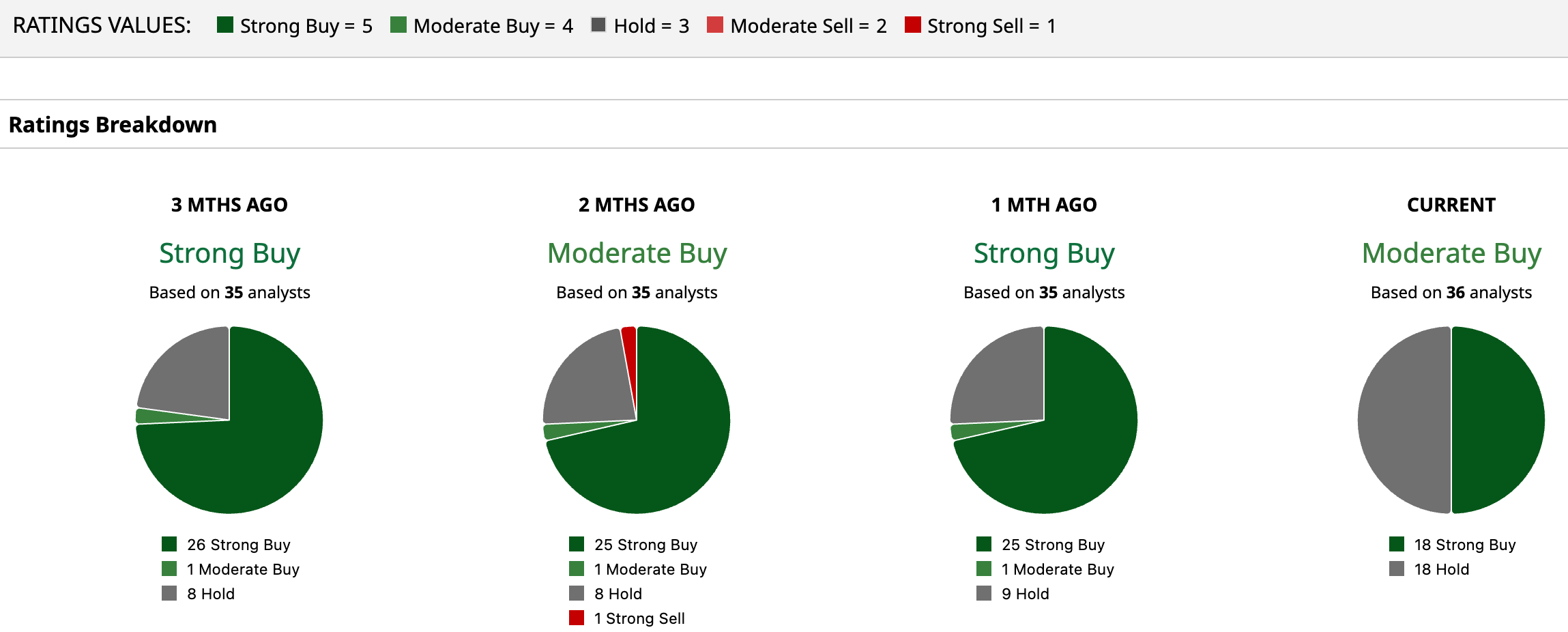

Despite the recent turbulence, Wall Street hasn’t entirely lost confidence in Pinterest. The stock still carries a consensus “Moderate Buy” rating from analysts. Out of the 36 analysts currently covering the company, 18 rate the stock a “Strong Buy,” while the remaining 18 recommend a “Hold,” reflecting a mix of optimism and caution around its near-term outlook.

Analysts also see room for potential upside. The average price target of $24.42 implies the stock could rise about 24% from current levels. Meanwhile, the most bullish forecast on the Street sits at $45, suggesting the shares could surge as much as 128% if the company executes well.

The Bottom Line

The entry of activist heavyweight Elliott Investment Management adds an interesting new layer to Pinterest’s story. Elliott’s $1 billion stake not only signals confidence in Pinterest’s long-term prospects but could also act as a catalyst for sharper strategic focus and stronger shareholder returns. For investors willing to tolerate some volatility, the activist investor’s bold bet may be a good reason to keep this beaten-down stock firmly on the radar now.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- SoundHound Is One of the Most Short Stocks Right Now. Should You Bet on a SOUN Squeeze?

- Down 15% in 2026, Should You Buy the Dip in Microsoft Stock?

- 1 ‘Strong Buy’ AI Stock That Wedbush Loves Now: ‘No Lost Deals’ Amid ‘Disruption’

- Okta Is Pushing Higher. Should You Chase the Rally in OKTA Stock After Earnings Here?