Marvell Technology (MRVL) provided a strong outlook for Q1 revenue and earnings after two acquisitions. That may have led to its reporting a one-time decline in Q4 cash flow. Bullish sentiment has led to an unusual options trading volume in out-of-the-money puts.

MRVL is at $91.05 today, down from a recent peak, but up sharply after its after-market close earnings release on March 5. On that day, MRVL closed at $75.68, so it's still up +20% in the last week.

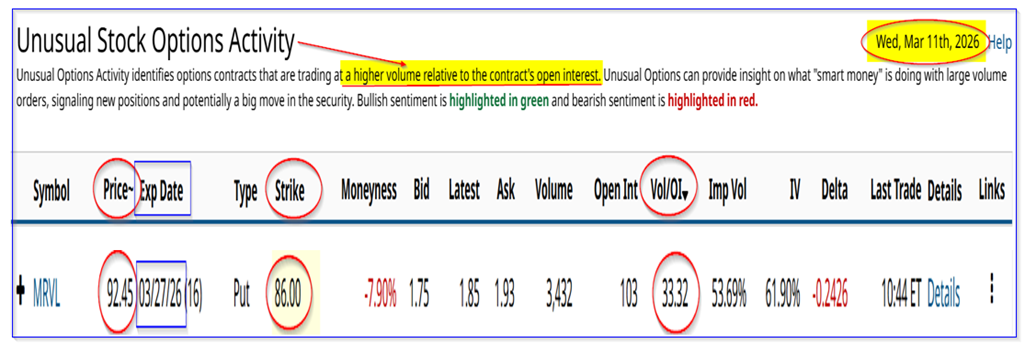

That could also be why there is so much action in its out-of-the-money (OTM) puts. This can be seen in Barchart's Unusual Stock Options Activity Report.

It shows that over 33 times the normal volume of put options at the $86.00 strike price traded for expiry on March 27. That strike price, 16 days to expiry (DTE), is 6% below today's price.

As a result, it shows that some investors believe MRVL will tumble (i.e., the buyers). But sellers of these OTM puts are collecting a hefty premium.

For example, the premium is $1.85 at the midpoint. That means a seller collects a two-week yield of 2.15%:

$1.85/$86.00 = 0.0215

That means an investor who secures $8,600 to “Sell to Open” 1 put contract immediately collects $185.00 in their account. But if MRVL drops to $86.00 or lower on or before March 16, the $8.6K collateral could be assigned to buy 100 shares at $86.00.

However, the breakeven cost (B/E) is just $84.15, or 7.6% lower than today's price.

Similarly, put buyers are hoping that MRVL will fall below this B/E point. That may or may not occur in the next two weeks.

Nevertheless, one thing is for sure: investors have reason to be positive about Marvell Technology's outlook, given management's guidance.

Poor Cash Flow But Strong Outlook

Marvell Technology, a system-on-a-chip designer, is benefiting from strong AI data center demand for its products. Revenue was up 22.08% YoY and +6.9% QoQ from $2.075 billion last quarter to $2.219 billion.

Despite closing on two acquisitions during the quarter, margins were up slightly. Stock Analysis shows that its Q4 gross margin was 51.74% vs. 50.48% a year ago and 51.57% in Q3.

That slight gain in margins was seen in operating and EBITDA margins:

Operating Margins: 18.23% Q4, vs. 12.94% 2024 Q4 and 17.25% Q3;

EBITDA Margins: 32.51% Q4 vs. 30.87% and 32.48%.

However, its free cash flow (FCF), which includes capex spending as well as net changes in working capital, was lower on an absolute basis. That lowered its FCF margins:

FCF Margins: 11.69% Q4 vs. 24.44% Q4 2025, and 24.53% Q3.

That is likely to be a one-time dip, due to the acquisition closing costs and the huge demand on inventory and capex from higher AI data center demand.

For example, capex spending rose from $70 million last year to $114 million in Q4 2025, up 52%. It was also up from $73.5 million last quarter (Q3). This meant as a percentage of revenue, the capex cost rose from 3.54% of sales in Q3 to 5.15%.

Nevertheless, Marvell Technology's management was very upbeat about its Q1 and full-year outlook.

For example, it said it expects non-GAAP diluted earnings per share (EPS) to be 79 cents (with a 5-cent plus or minus range). That compares with its 80 diluted EPS for Q4.

However, assuming capex remains stable at this level, it's possible to project strong free cash flow (FCF) for the next 12 months (NTM).

Projecting NTM FCF

For example, analysts are projecting that 2026 revenue will rise to $10.85 billion this year (up 32% from $8.195 in 2025), and $14.87 billion in 2027 (+81.5%). That implies an NTM average of $12.86 billion.

Over the last 12 months (LTM), Marvell's free cash flow (FCF) was $1.396 billion, or 17% of revenue, according to Stock Analysis. But that included a drop in Q4 FCF margins. So, if the company can average 20% over the next 12 months (NTM), as it did during the LTM period to Q3 (20.29%), FCF could exceed $2.5 billion:

$12.86 NTM revenue x 0.20 = $2.572 billion NTM FCF

That would be 84% higher than the $1.4 billion FCF in 2025. As a result, MRVL stock could be worth much more over the next year. Here's why.

Price Targets for MRVL Stock

For example, given MRVL stock's market cap today of $79.3 billion, MRVL stock's FCF yield is about 1.8%:

$1.4b LTM FCF / $79.3 b mkt cap = 0.01765

So, using our $2.57 NTM FCF projection, here is where the market cap could be over the next year:

$2.572b FCF / 0.0176 = $146 billion mkt cap

In other words, MRVL's value could rise +84% over the next 12 months. That sets a price target (PT) of:

$91.05 x 1.84 = $167.53 PT

Other Wall Street analysts believe MRVL is deeply undervalued. For example, Yahoo! Finance shows that 43 analysts have an average PT of $120.28. That's +32% over today's price.

Similarly, Barchart's mean analyst PT is $119.35, and AnaChart.com's survey of 31 analysts is $121.79. So, Wall Street also sees significant upside in MRVL stock.

Conclusion

Despite the strong outlook and recent uptick in MRVL stock, there is no guarantee that these put options will be profitable for buyers or sellers. It is too short a period (16 DTE) to be anything other than a speculative bet.

However, short-sellers of these puts have a good potential breakeven buy-in point ($84.15). Nevertheless, shorting these puts comes with downside risk. Investors could end up with an unrealized loss if MRVL falls to below this B/E point.

That's why I always recommend taking a longer period - usually one month to six weeks.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart