Sallie Mae’s stock price has taken a beating over the past six months, shedding 34% of its value and falling to $20.93 per share. This may have investors wondering how to approach the situation.

Following the drawdown, is this a buying opportunity for SLM? Find out in our full research report, it’s free.

Why Does SLM Stock Spark Debate?

Originally created as a government-sponsored enterprise before privatizing in 2004, Sallie Mae (NASDAQ: SLM) is a financial services company that provides private education loans, savings products, and educational resources to help students and families pay for college.

Two Things to Like:

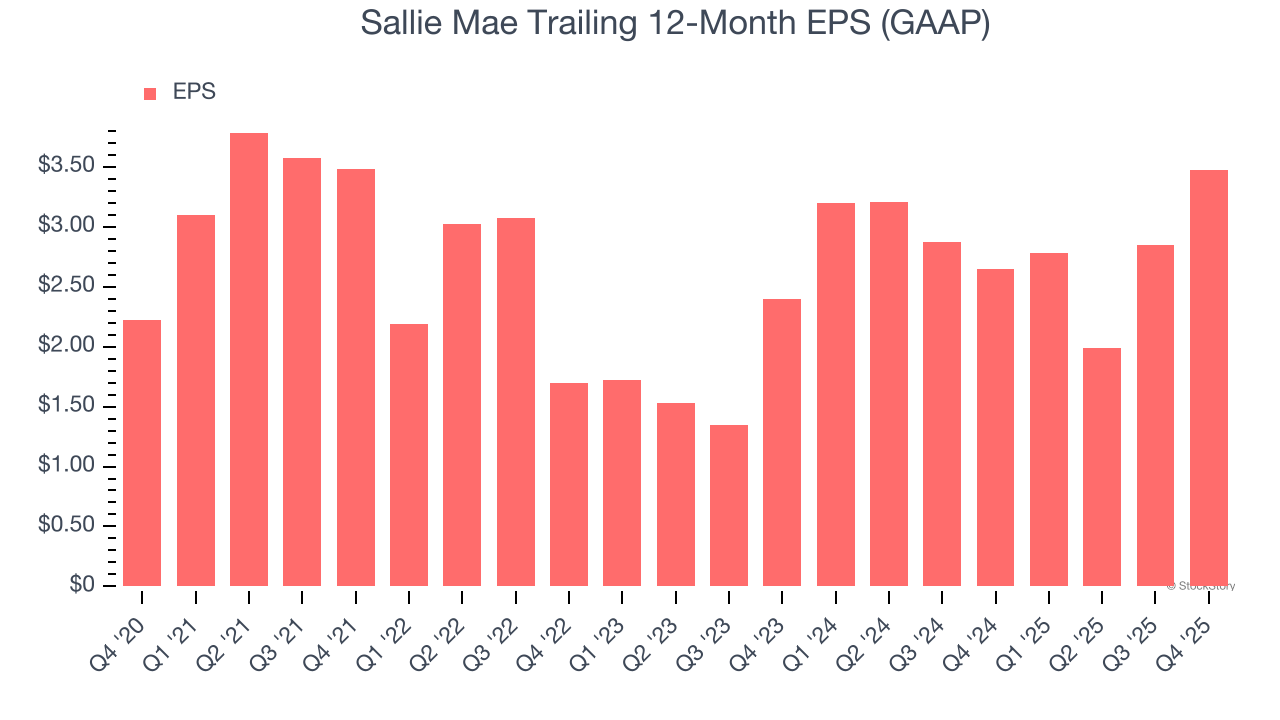

1. EPS Surges Higher Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sallie Mae’s EPS grew at a remarkable 20.2% compounded annual growth rate over the last two years, higher than its 4.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

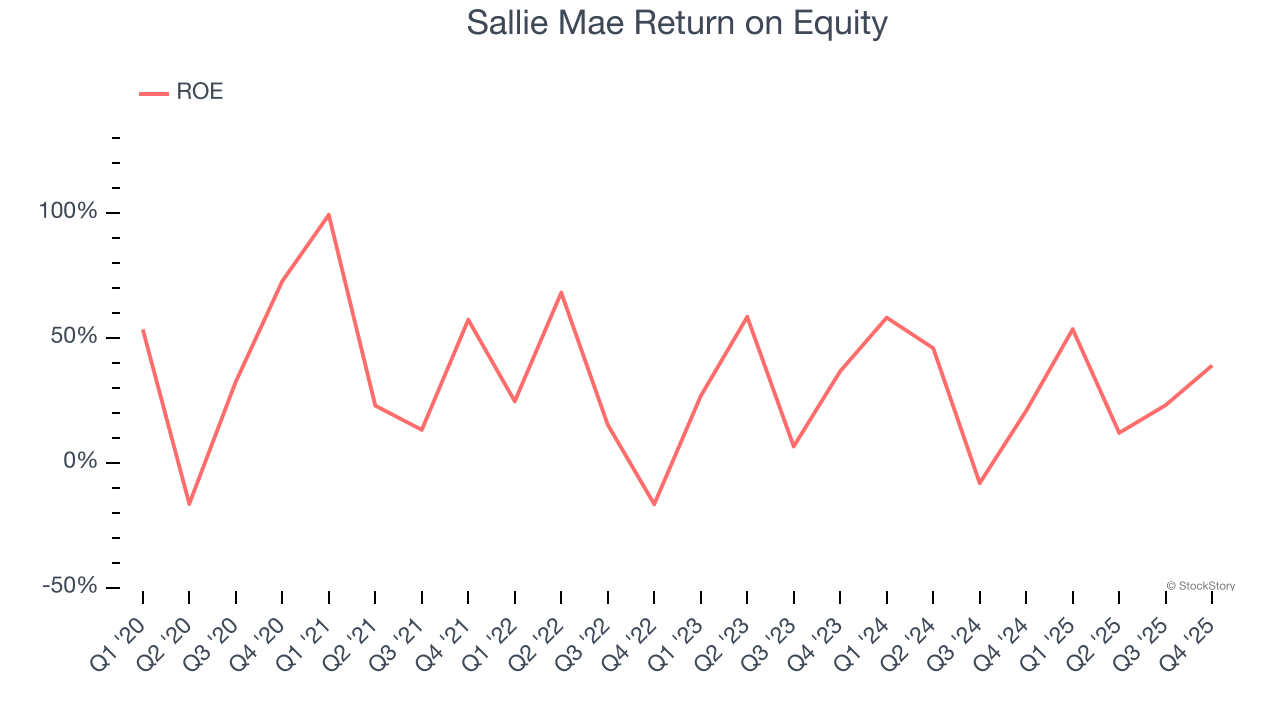

2. Stellar ROE Showcases Lucrative Growth Opportunities

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Sallie Mae has averaged an ROE of 32.8%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Sallie Mae has a strong competitive moat.

One Reason to be Careful:

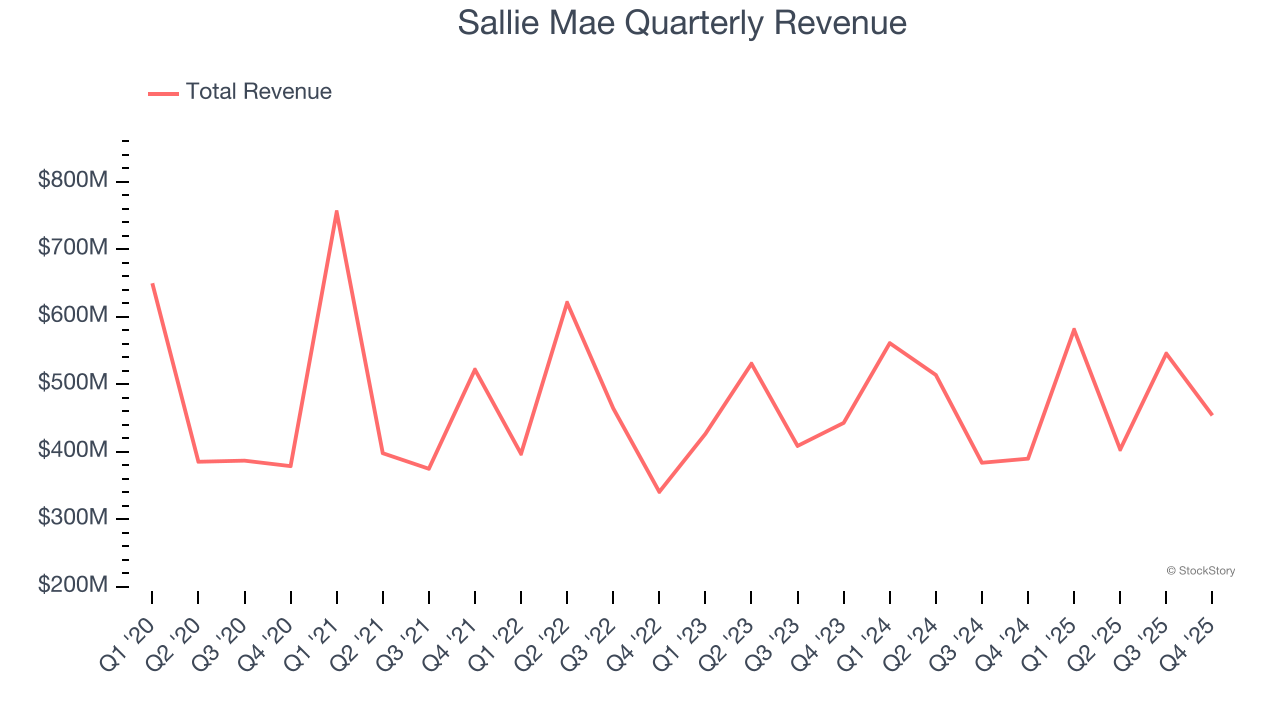

Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

Regrettably, Sallie Mae’s revenue grew at a sluggish 2% compounded annual growth rate over the last five years. This wasn’t a great result, but there are still things to like about Sallie Mae.

Final Judgment

Sallie Mae’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 7.5× forward P/E (or $20.93 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.