ICF International trades at $91.37 and has moved in lockstep with the market. Its shares have returned 10.4% over the last six months while the S&P 500 has gained 9.6%.

Is there a buying opportunity in ICF International, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think ICF International Will Underperform?

We're sitting this one out for now. Here are three reasons why ICFI doesn't excite us and a stock we'd rather own.

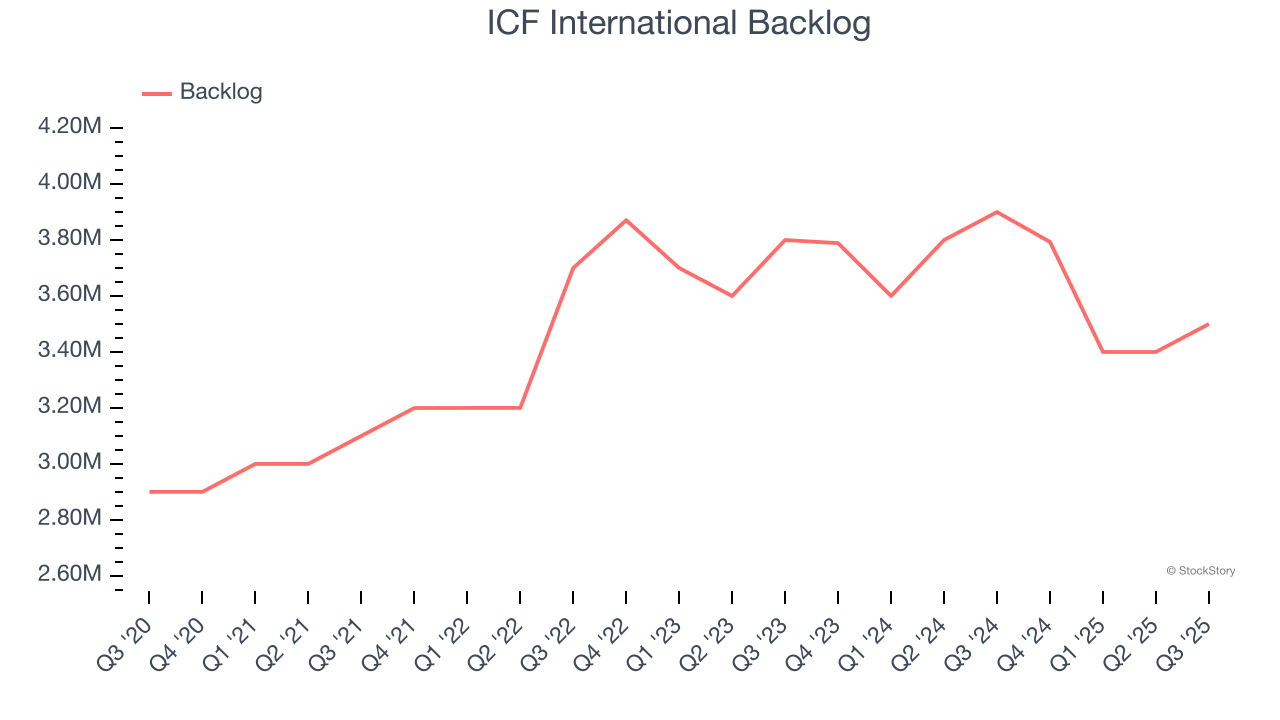

1. Backlog Declines as Orders Drop

Investors interested in Government & Technical Consulting companies should track backlog in addition to reported revenue. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into ICF International’s future revenue streams.

ICF International’s backlog came in at $3.5 million in the latest quarter, and it averaged 2.9% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect ICF International’s revenue to drop by 3%, a decrease from its 5.6% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will face some demand challenges.

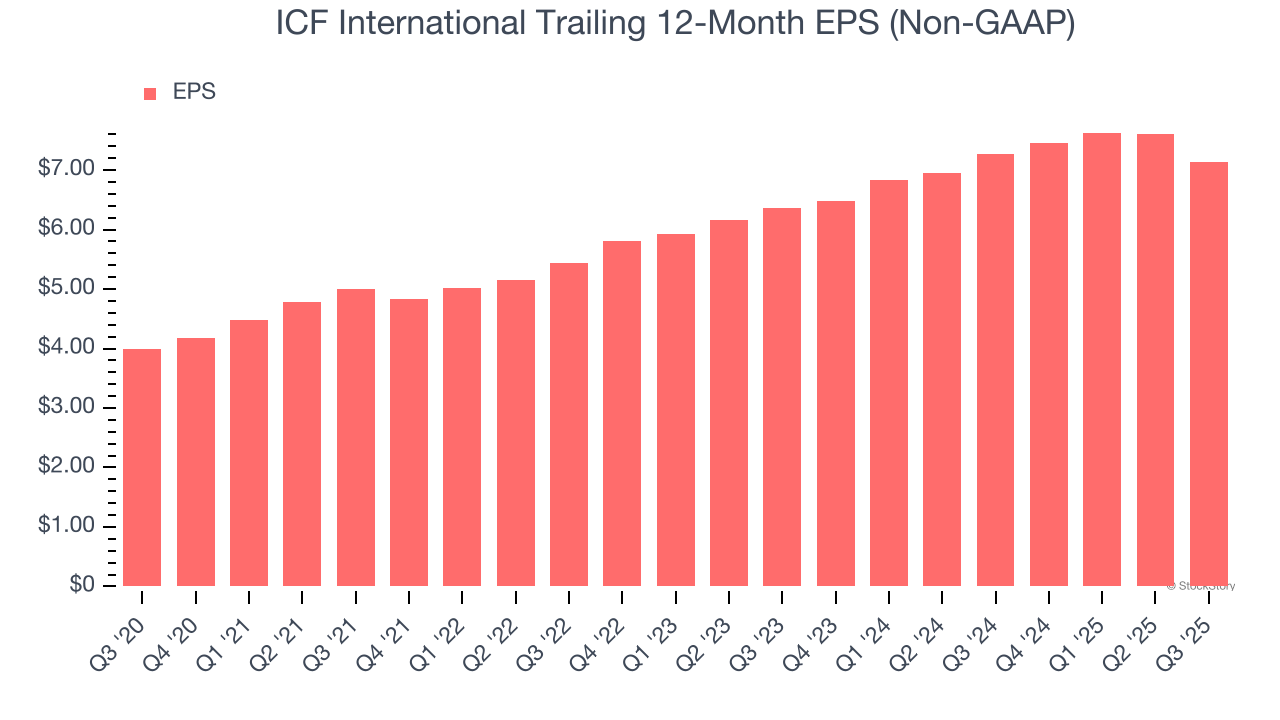

3. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

ICF International’s EPS grew at an unimpressive 6% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its flat revenue and tells us management responded to softer demand by adapting its cost structure.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of ICF International, we’ll be cheering from the sidelines. That said, the stock currently trades at 13.6× forward P/E (or $91.37 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.