What a time it’s been for iRhythm. In the past six months alone, the company’s stock price has increased by a massive 54.5%, reaching $168.51 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy iRhythm, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is iRhythm Not Exciting?

Despite the momentum, we're swiping left on iRhythm for now. Here are three reasons why IRTC doesn't excite us and a stock we'd rather own.

1. Fewer Distribution Channels Limit its Ceiling

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $657.2 million in revenue over the past 12 months, iRhythm is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

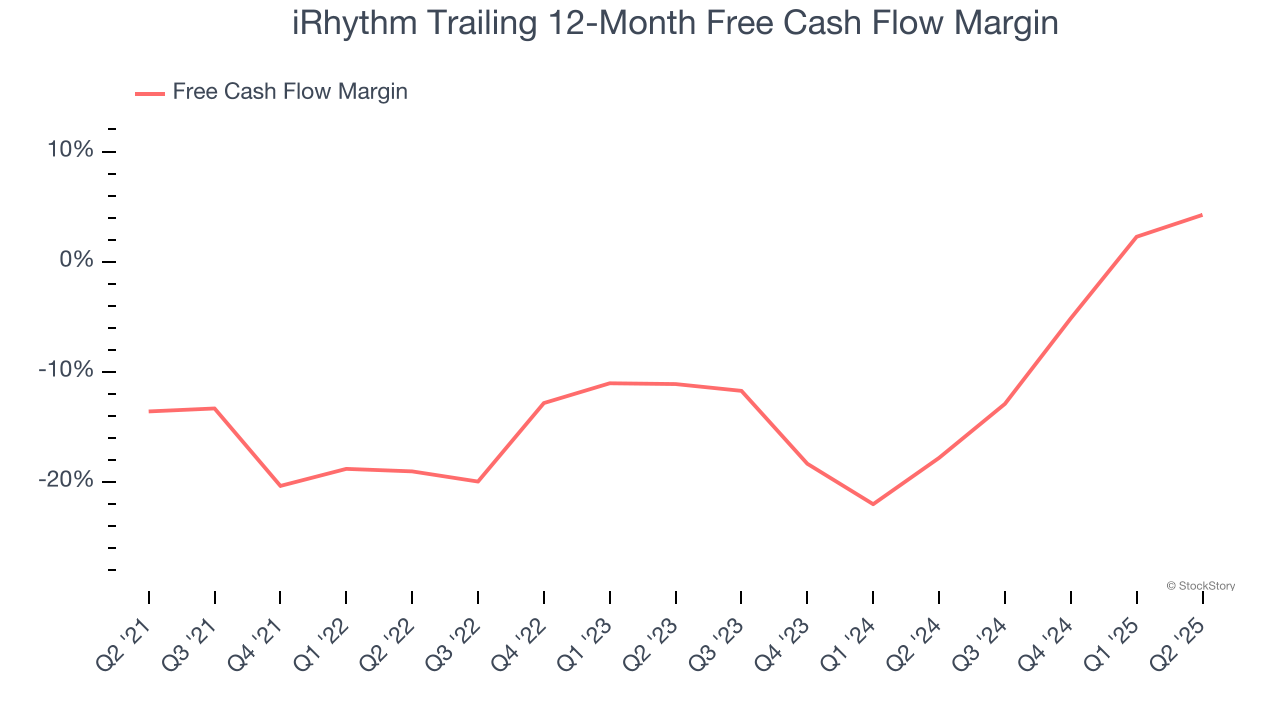

2. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While iRhythm posted positive free cash flow this quarter, the broader story hasn’t been so clean. iRhythm’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 9.9%. This means it lit $9.89 of cash on fire for every $100 in revenue.

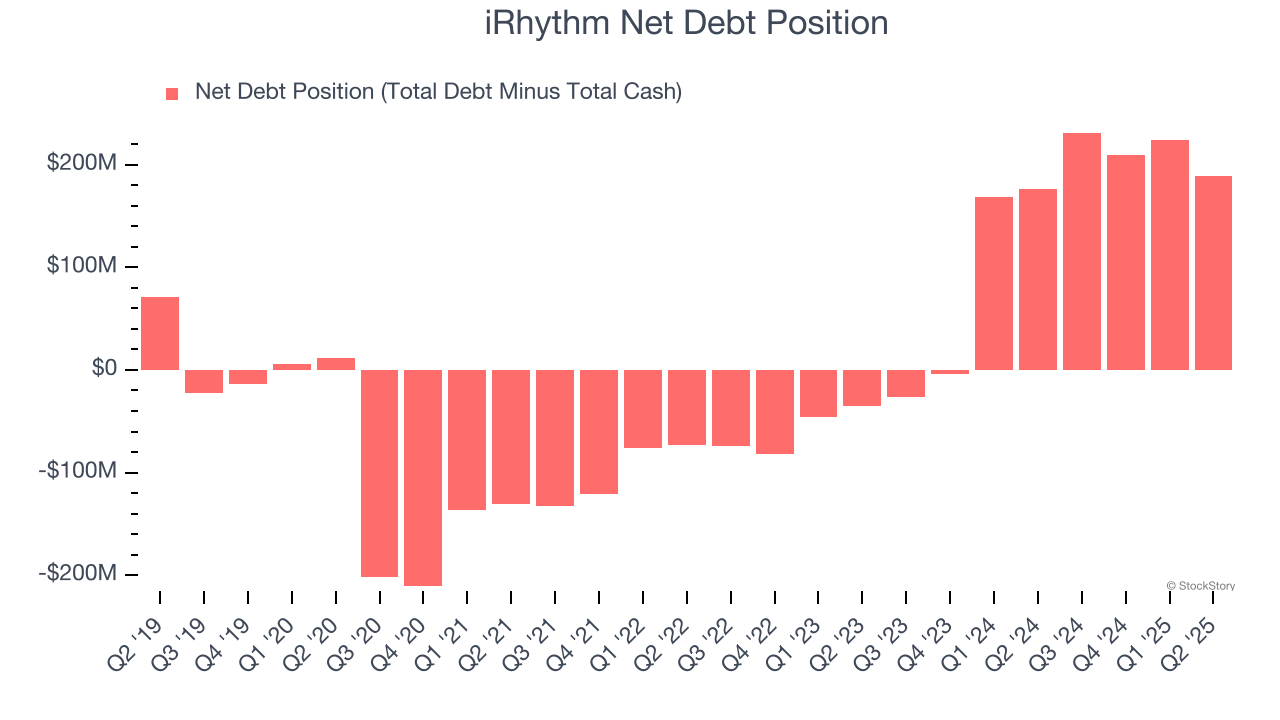

3. High Debt Levels Increase Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

iRhythm’s $734.7 million of debt exceeds the $545.5 million of cash on its balance sheet. Furthermore, its net-debt-to-EBITDA ratio (based on its EBITDA of $12.44 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. iRhythm could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope iRhythm can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

iRhythm isn’t a terrible business, but it doesn’t pass our bar. Following the recent rally, the stock trades at 78.5× forward EV-to-EBITDA (or $168.51 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than iRhythm

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.