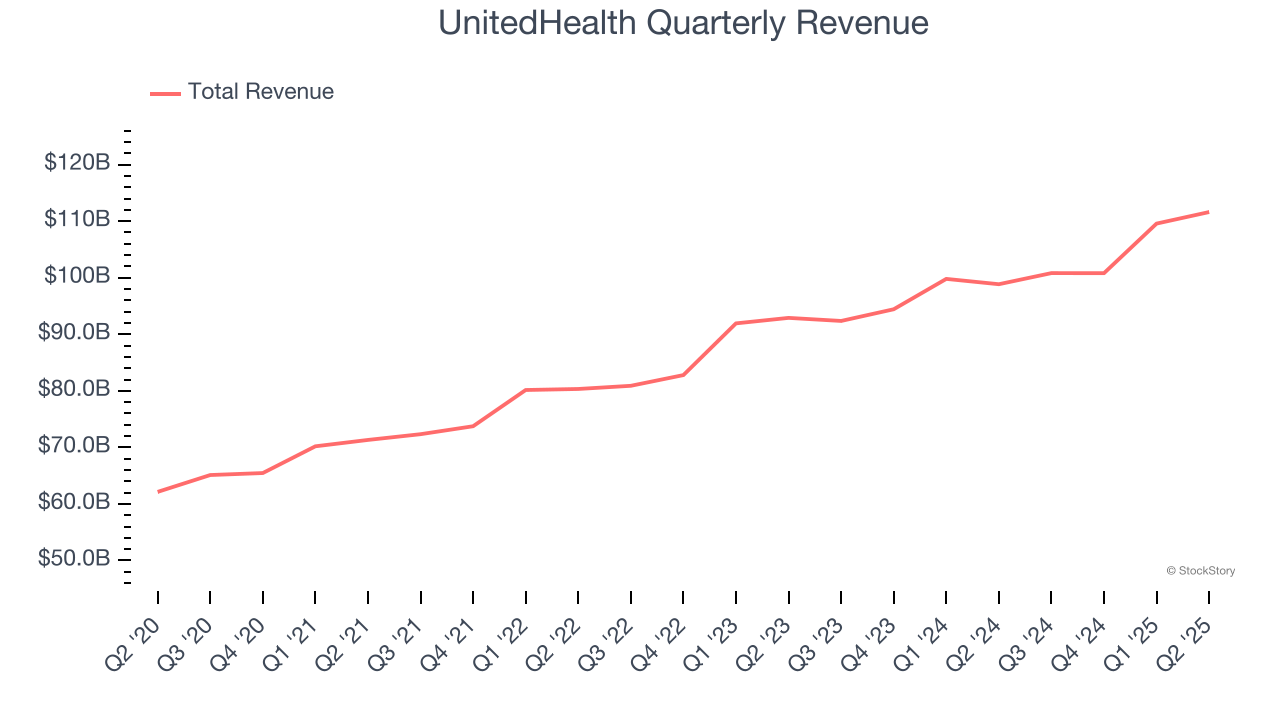

Health insurance company UnitedHealth (NYSE: UNH) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 12.9% year on year to $111.6 billion. On the other hand, the company’s full-year revenue guidance of $446.8 billion at the midpoint came in 0.5% below analysts’ estimates. Its non-GAAP profit of $4.08 per share was 8.3% below analysts’ consensus estimates.

Is now the time to buy UnitedHealth? Find out by accessing our full research report, it’s free.

UnitedHealth (UNH) Q2 CY2025 Highlights:

- Revenue: $111.6 billion vs analyst estimates of $111.9 billion (12.9% year-on-year growth, in line)

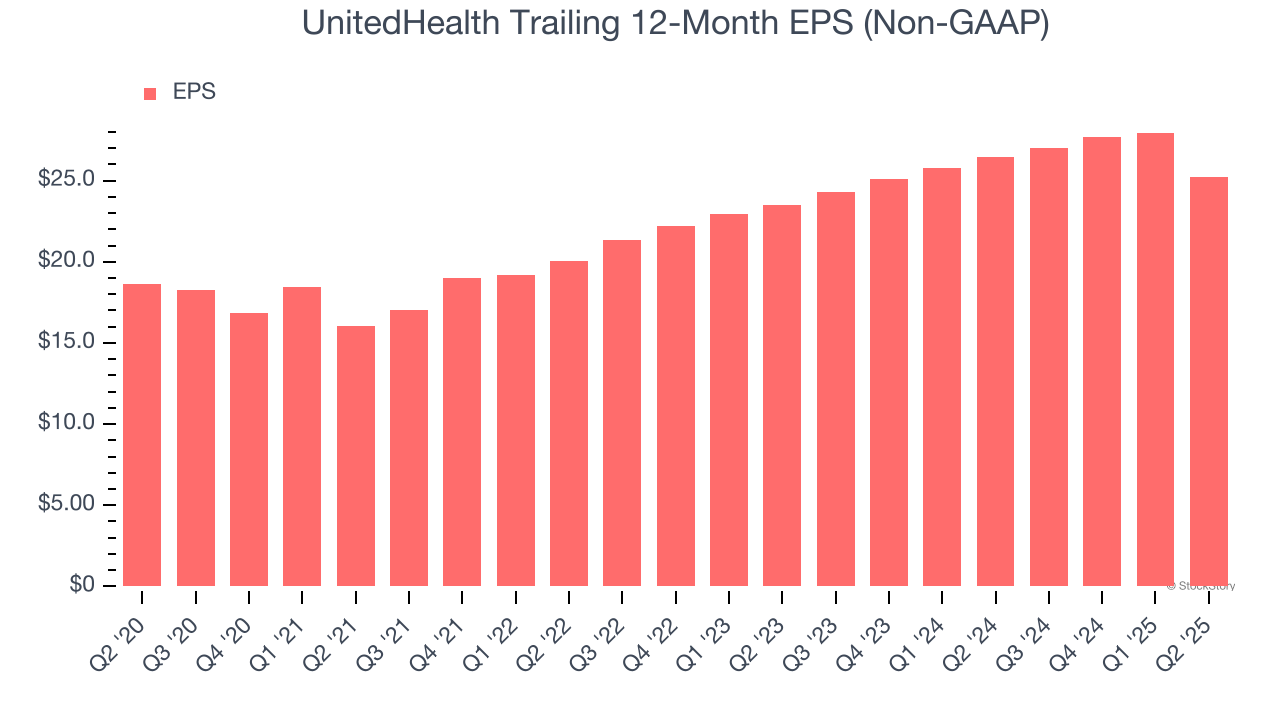

- Adjusted EPS: $4.08 vs analyst expectations of $4.45 (8.3% miss)

- Adjusted EBITDA: $6.43 billion vs analyst estimates of $7.14 billion (5.8% margin, 9.9% miss)

- Management lowered its full-year Adjusted EPS guidance to $16 at the midpoint, a 39% decrease

- “While we face challenges across our lines of business, we believe we can resolve these issues and recapture our earnings growth potential while ensuring people have access to high-quality, affordable health care,” UnitedHealthcare CEO Tim Noel said

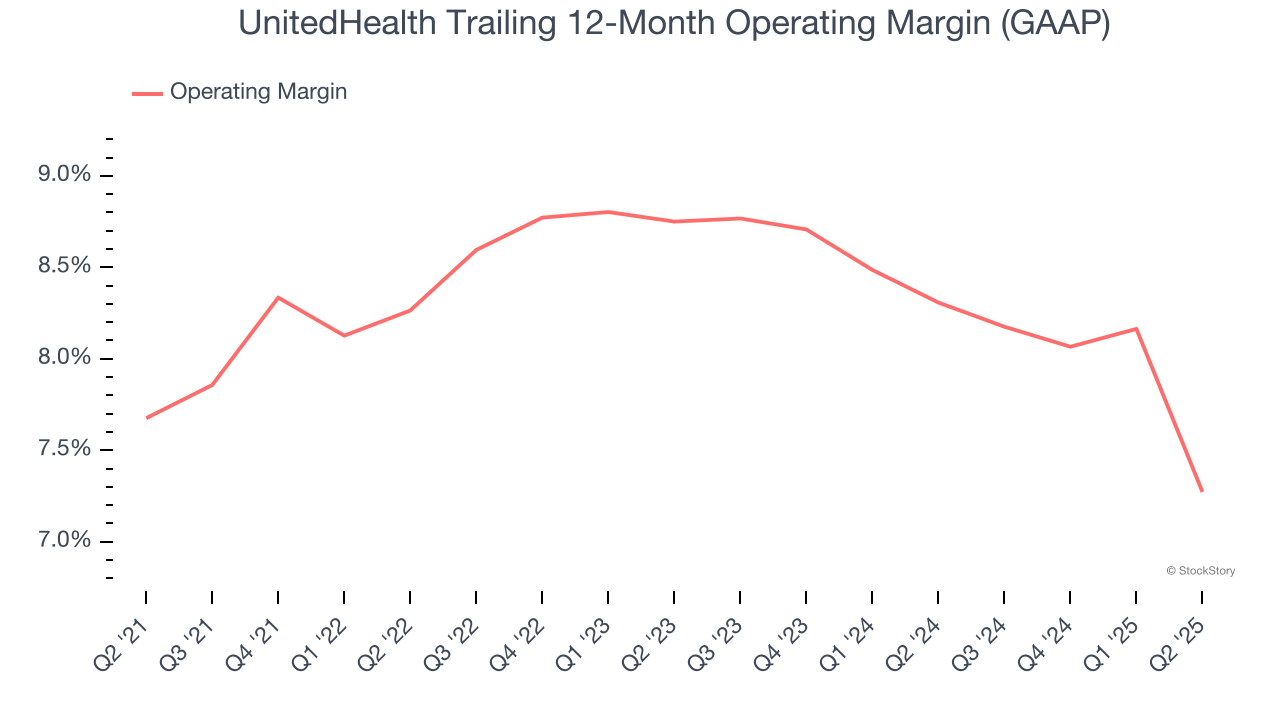

- Operating Margin: 4.6%, down from 8% in the same quarter last year

- Free Cash Flow Margin: 5.6%, similar to the same quarter last year

- Market Capitalization: $255.9 billion

“UnitedHealth Group has embarked on a rigorous path back to being a high-performing company fully serving the health needs of individuals and society broadly,” said Stephen Hemsley, chief executive officer of UnitedHealth Group.

Company Overview

With over 100 million people served across its various businesses and a workforce of more than 400,000, UnitedHealth Group (NYSE: UNH) operates a health insurance business and Optum, a healthcare services division that provides everything from pharmacy benefits to primary care.

Revenue Growth

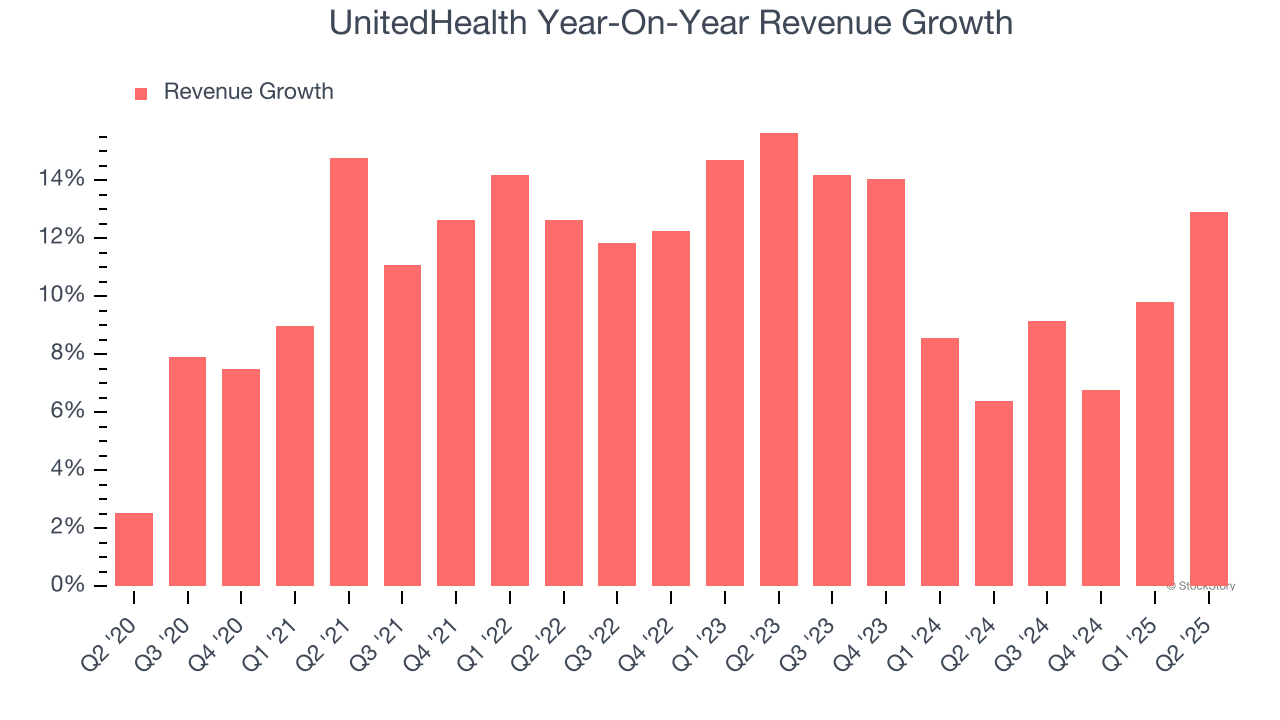

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, UnitedHealth grew its sales at a decent 11.3% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. UnitedHealth’s annualized revenue growth of 10.1% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, UnitedHealth’s year-on-year revenue growth was 12.9%, and its $111.6 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.4% over the next 12 months, similar to its two-year rate. This projection is particularly noteworthy for a company of its scale and implies the market sees success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

UnitedHealth’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 8% over the last five years. This profitability was mediocre for a healthcare business and caused by its suboptimal cost structure.

Analyzing the trend in its profitability, UnitedHealth’s operating margin of 7.3% for the trailing 12 months may be around the same as five years ago, but it has decreased by 1.5 percentage points over the last two years. Still, we’re optimistic that UnitedHealth can correct course and expand its profitability on a longer-term horizon due to its business quality.

This quarter, UnitedHealth generated an operating margin profit margin of 4.6%, down 3.4 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

UnitedHealth’s EPS grew at a decent 6.3% compounded annual growth rate over the last five years. However, this performance was lower than its 11.3% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q2, UnitedHealth reported EPS at $4.08, down from $6.80 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects UnitedHealth’s full-year EPS of $25.24 to shrink by 14.7%.

Key Takeaways from UnitedHealth’s Q2 Results

We struggled to find many positives in these results. Its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. “While we face challenges across our lines of business, we believe we can resolve these issues and recapture our earnings growth potential while ensuring people have access to high-quality, affordable health care,” UnitedHealthcare CEO Tim Noel said. Overall, this was a weaker quarter. The stock traded down 4.4% to $269.76 immediately following the results.

UnitedHealth underperformed this quarter, but does that create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.