Environmental solutions provider CECO Environmental (NASDAQ: CECO) announced better-than-expected revenue in Q2 CY2025, with sales up 34.8% year on year to $185.4 million. The company’s full-year revenue guidance of $750 million at the midpoint came in 3.2% above analysts’ estimates. Its non-GAAP profit of $0.24 per share was 35.8% above analysts’ consensus estimates.

Is now the time to buy CECO Environmental? Find out by accessing our full research report, it’s free.

CECO Environmental (CECO) Q2 CY2025 Highlights:

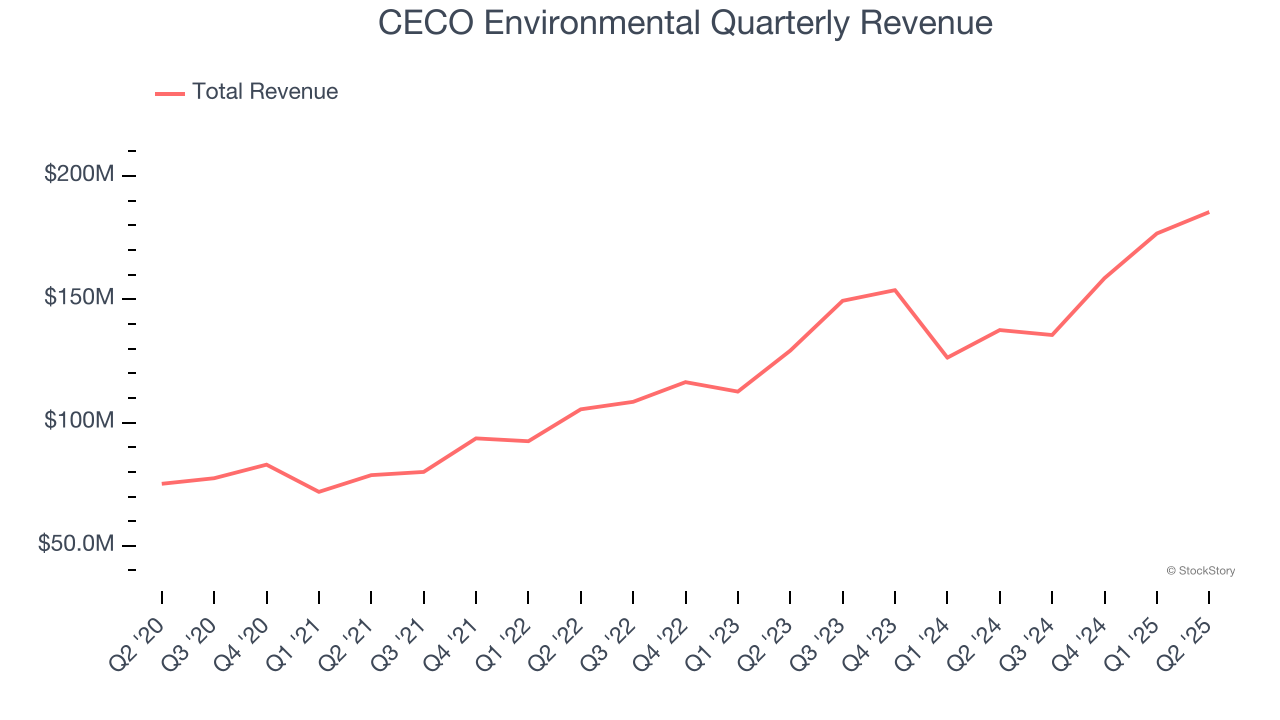

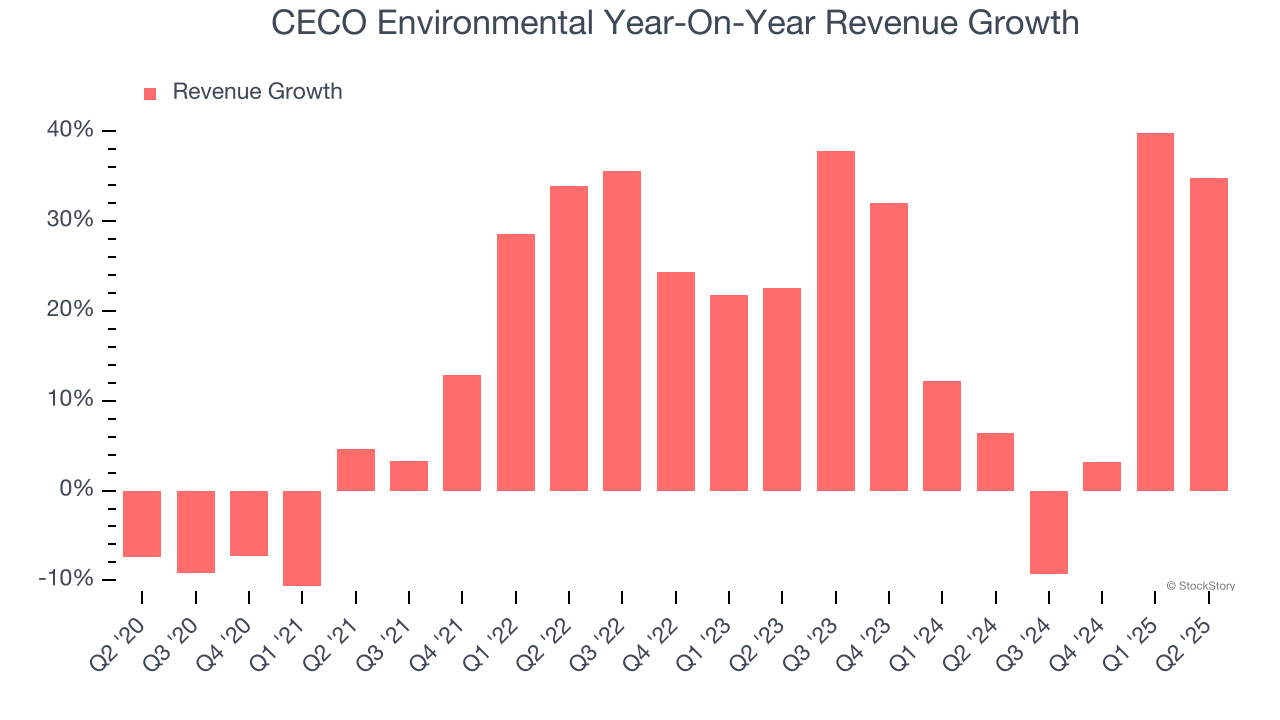

- Revenue: $185.4 million vs analyst estimates of $179.2 million (34.8% year-on-year growth, 3.5% beat)

- Adjusted EPS: $0.24 vs analyst estimates of $0.18 (35.8% beat)

- Adjusted EBITDA: $23.3 million vs analyst estimates of $20.63 million (12.6% margin, 13% beat)

- The company lifted its revenue guidance for the full year to $750 million at the midpoint from $725 million, a 3.4% increase

- EBITDA guidance for the full year is $95 million at the midpoint, above analyst estimates of $90.4 million

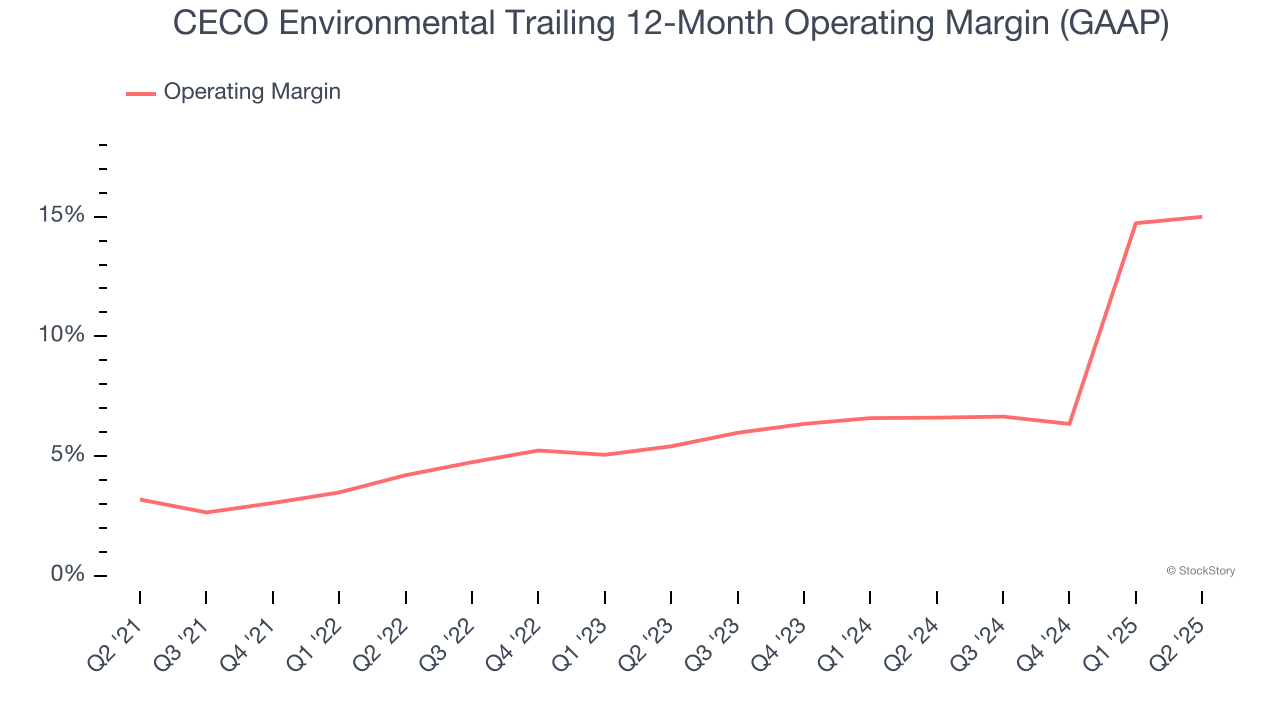

- Operating Margin: 9.7%, up from 6.7% in the same quarter last year

- Free Cash Flow was -$3 million, down from $2.6 million in the same quarter last year

- Market Capitalization: $1.22 billion

Todd Gleason, CECO's Chief Executive Officer commented, “We delivered another record quarter, led by tremendous orders, which were up 95 percent year-over-year. Our multi-quarter string of record bookings enabled our highest ever quarterly revenue and increased our backlog to an all-time high of $688 million, which is up 76 percent versus last year. Our diverse and well-positioned portfolio of leading environmental solutions for industrial air, industrial water and energy transition markets continue to gain traction in key markets and new geographies. In the quarter, we booked CECO's largest-ever order which will provide emissions management solutions for a large power generation project. That order, combined with continued strong natural gas and water infrastructure and other energy transition projects, helped push second quarter orders to the all-time record. We are excited about our ability to capitalize on these mega-theme opportunities as well as our steady return on investment associated with our ongoing portfolio transformation.”

Company Overview

With roots dating back to 1869 and a focus on creating cleaner industrial operations, CECO Environmental (NASDAQ: CECO) provides technology and expertise that helps industrial companies reduce emissions, treat water, and improve energy efficiency across various sectors.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $656.2 million in revenue over the past 12 months, CECO Environmental is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, CECO Environmental’s 14.7% annualized revenue growth over the last five years was exceptional. This is an encouraging starting point for our analysis because it shows CECO Environmental’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. CECO Environmental’s annualized revenue growth of 18.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, CECO Environmental reported wonderful year-on-year revenue growth of 34.8%, and its $185.4 million of revenue exceeded Wall Street’s estimates by 3.5%.

Looking ahead, sell-side analysts expect revenue to grow 15.8% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is noteworthy and suggests the market sees success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

CECO Environmental was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.9% was weak for a business services business.

On the plus side, CECO Environmental’s operating margin rose by 11.8 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q2, CECO Environmental generated an operating margin profit margin of 9.7%, up 3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

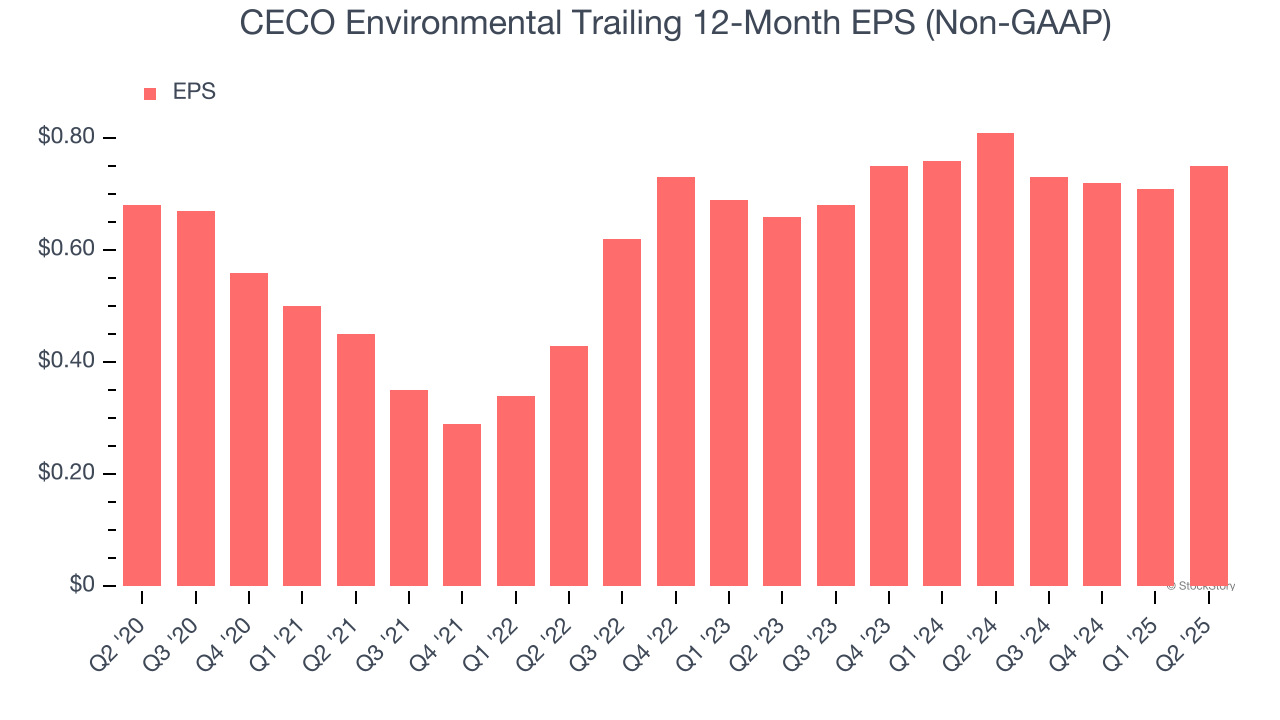

CECO Environmental’s EPS grew at a weak 2% compounded annual growth rate over the last five years, lower than its 14.7% annualized revenue growth. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

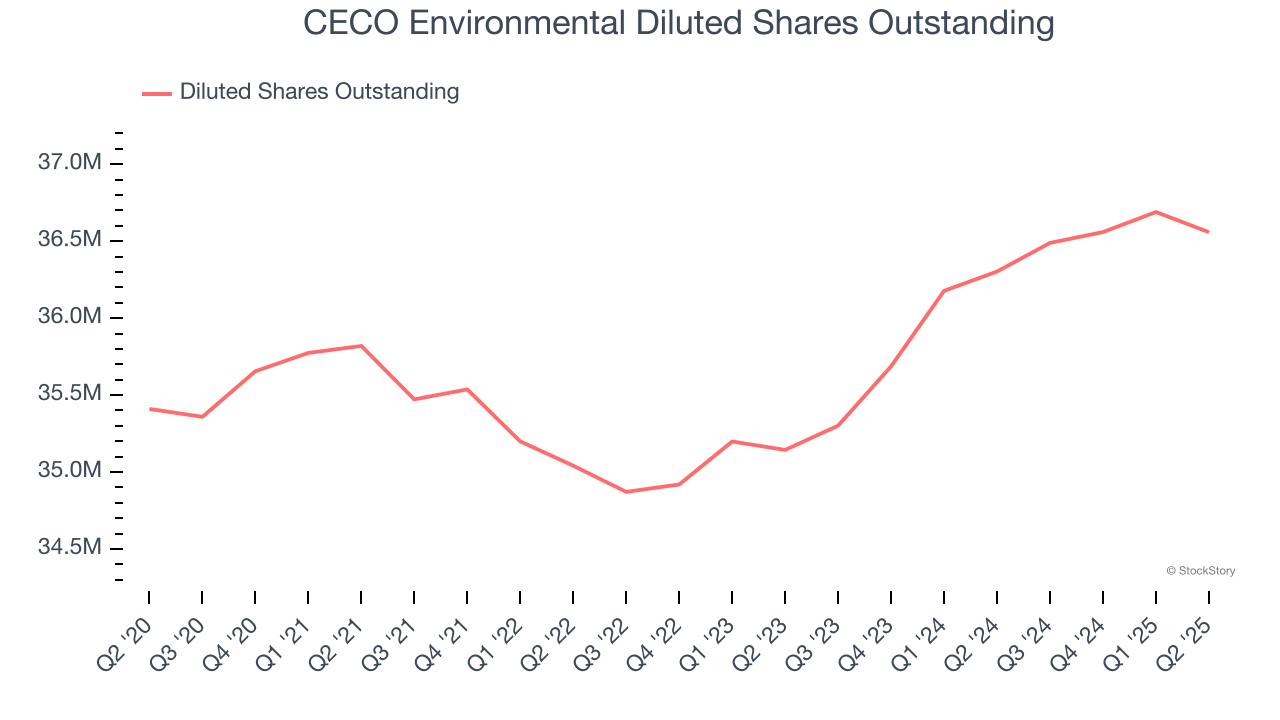

Diving into the nuances of CECO Environmental’s earnings can give us a better understanding of its performance. A five-year view shows CECO Environmental has diluted its shareholders, growing its share count by 3.2%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For CECO Environmental, its two-year annual EPS growth of 6.6% was higher than its five-year trend. Accelerating earnings growth is almost always a great sign.

In Q2, CECO Environmental reported EPS at $0.24, up from $0.20 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects CECO Environmental’s full-year EPS of $0.75 to grow 69%.

Key Takeaways from CECO Environmental’s Q2 Results

We were impressed by how significantly CECO Environmental blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also glad it lifted its full-year revenue guidance. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 5.3% to $36.50 immediately after reporting.

Indeed, CECO Environmental had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.