Earnings results often indicate what direction a company will take in the months ahead. With Q3 behind us, let’s have a look at W.W. Grainger (NYSE: GWW) and its peers.

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Maintenance and repair distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to serve customers everywhere. Additionally, maintenance and repair distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

The 8 maintenance and repair distributors stocks we track reported a slower Q3. As a group, revenues were in line with analysts’ consensus estimates.

Thankfully, share prices of the companies have been resilient as they are up 8.2% on average since the latest earnings results.

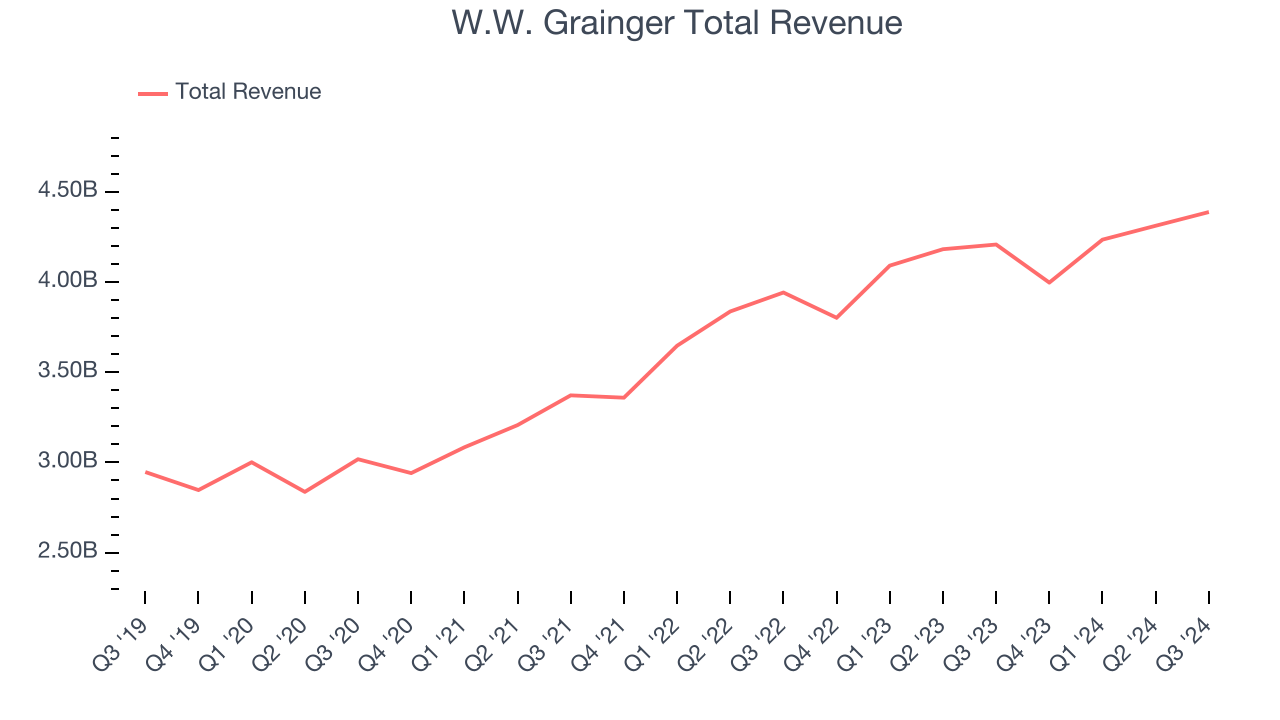

W.W. Grainger (NYSE: GWW)

Founded as a supplier of motors, W.W. Grainger (NYSE: GWW) provides maintenance, repair, and operating (MRO) supplies and services to businesses and institutions.

W.W. Grainger reported revenues of $4.39 billion, up 4.3% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with full-year EPS guidance slightly topping analysts’ expectations but a slight miss of analysts’ organic revenue estimates.

"From helping customers respond to natural disasters to supporting their safety needs, the team remains sharply focused on providing a flawless experience. As a result, throughout the third quarter, our customer relationships grew and results remained solid amidst a slow, but steady demand market, " said D.G. Macpherson, Chairman and CEO.

Interestingly, the stock is up 9.5% since reporting and currently trades at $1,206.

Is now the time to buy W.W. Grainger? Access our full analysis of the earnings results here, it’s free.

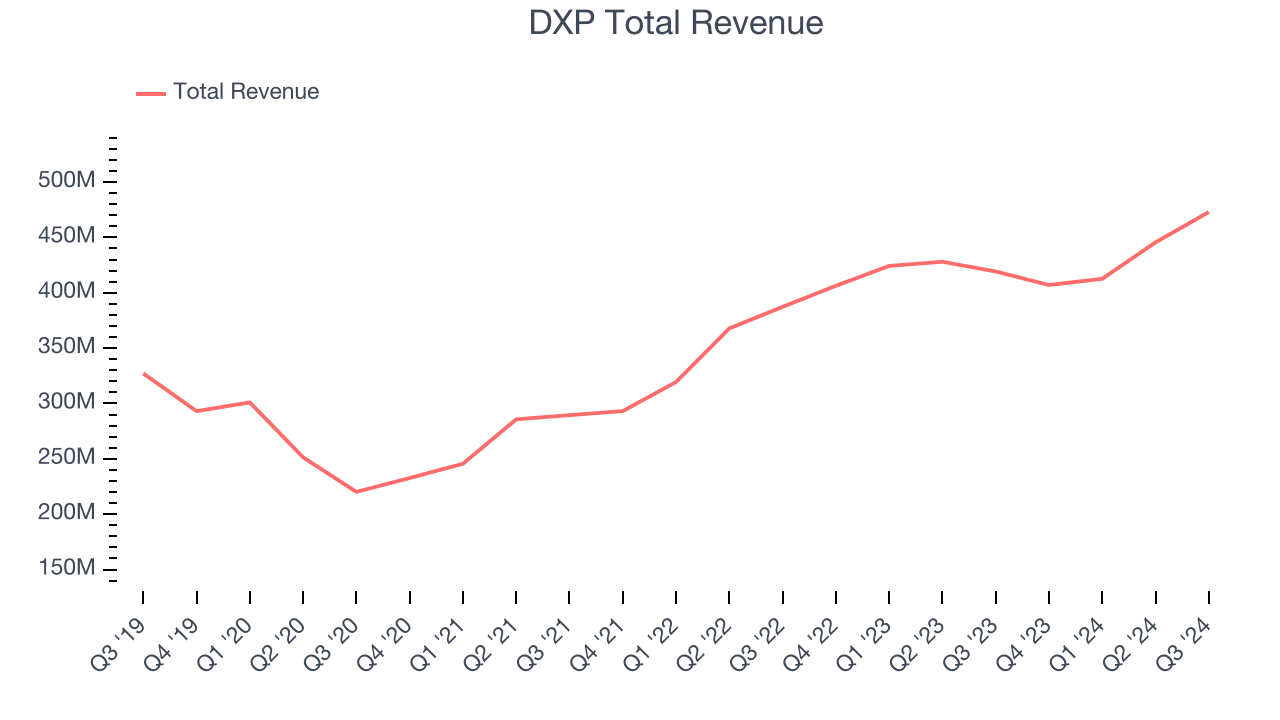

Best Q3: DXP (NASDAQ: DXPE)

Founded during the emergence of Big Oil in Texas, DXP (NASDAQ: DXPE) provides pumps, valves, and other industrial components.

DXP reported revenues of $472.9 million, up 12.8% year on year, outperforming analysts’ expectations by 6.8%. The business had an incredible quarter with a solid beat of analysts’ EPS and EBITDA estimates.

DXP delivered the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 41.3% since reporting. It currently trades at $71.93.

Is now the time to buy DXP? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Global Industrial (NYSE: GIC)

Formerly known as Systemax, Global Industrial (NYSE: GIC) distributes industrial and commercial products to businesses and institutions.

Global Industrial reported revenues of $342.4 million, down 3.4% year on year, falling short of analysts’ expectations by 3.1%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

As expected, the stock is down 13.9% since the results and currently trades at $28.49.

Read our full analysis of Global Industrial’s results here.

Fastenal (NASDAQ: FAST)

Founded in 1967, Fastenal (NASDAQ: FAST) provides industrial and construction supplies, including fasteners, tools, safety products, and many other product categories to businesses globally.

Fastenal reported revenues of $1.91 billion, up 3.5% year on year. This number was in line with analysts’ expectations. Aside from that, it was a mixed quarter as it also logged a narrow beat of analysts’ EPS estimates.

The stock is up 20.3% since reporting and currently trades at $84.20.

Read our full, actionable report on Fastenal here, it’s free.

Transcat (NASDAQ: TRNS)

Serving the pharmaceutical, industrial manufacturing, energy, and chemical process industries, Transcat (NASDAQ: TRNS) provides measurement instruments and supplies.

Transcat reported revenues of $67.83 million, up 8% year on year. This number lagged analysts' expectations by 3.5%. It was a disappointing quarter as it also logged a significant miss of analysts’ EBITDA and EPS estimates.

Transcat had the weakest performance against analyst estimates among its peers. The stock is down 11.9% since reporting and currently trades at $105.04.

Read our full, actionable report on Transcat here, it’s free.

Market Update

As a result of the Fed's rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed's 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump's victory in the US Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain. Said differently, there's still much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.