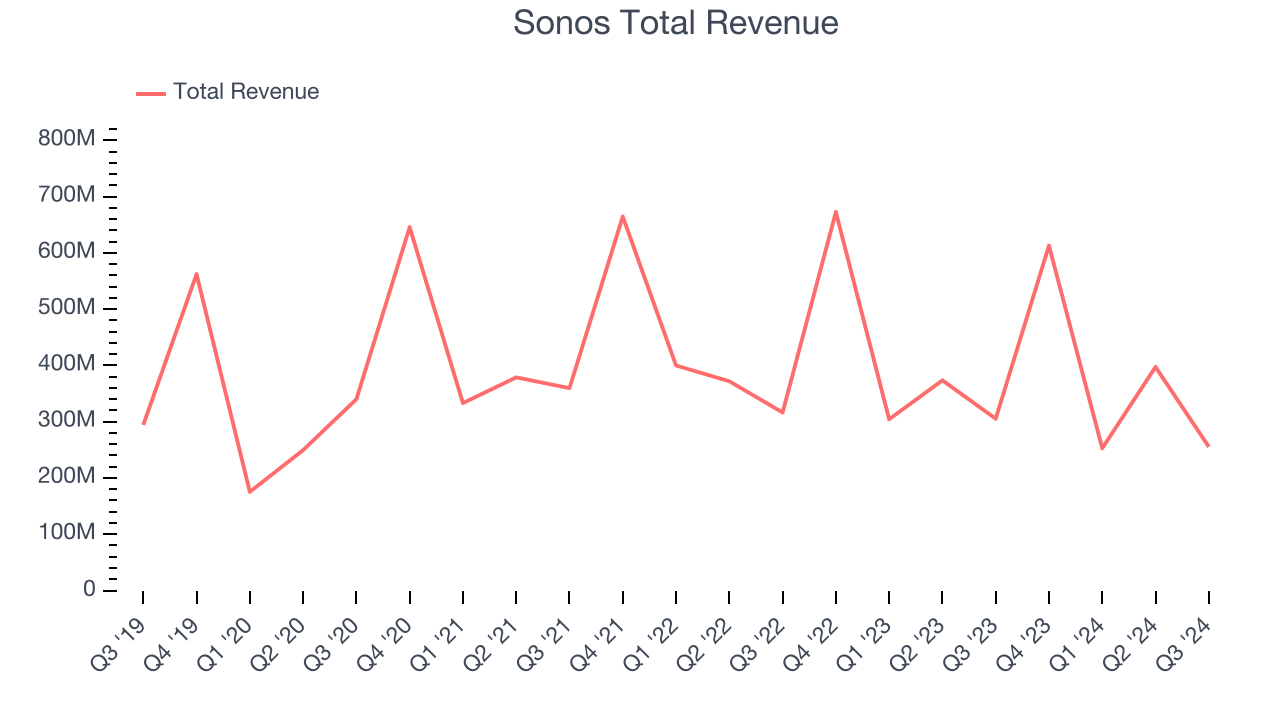

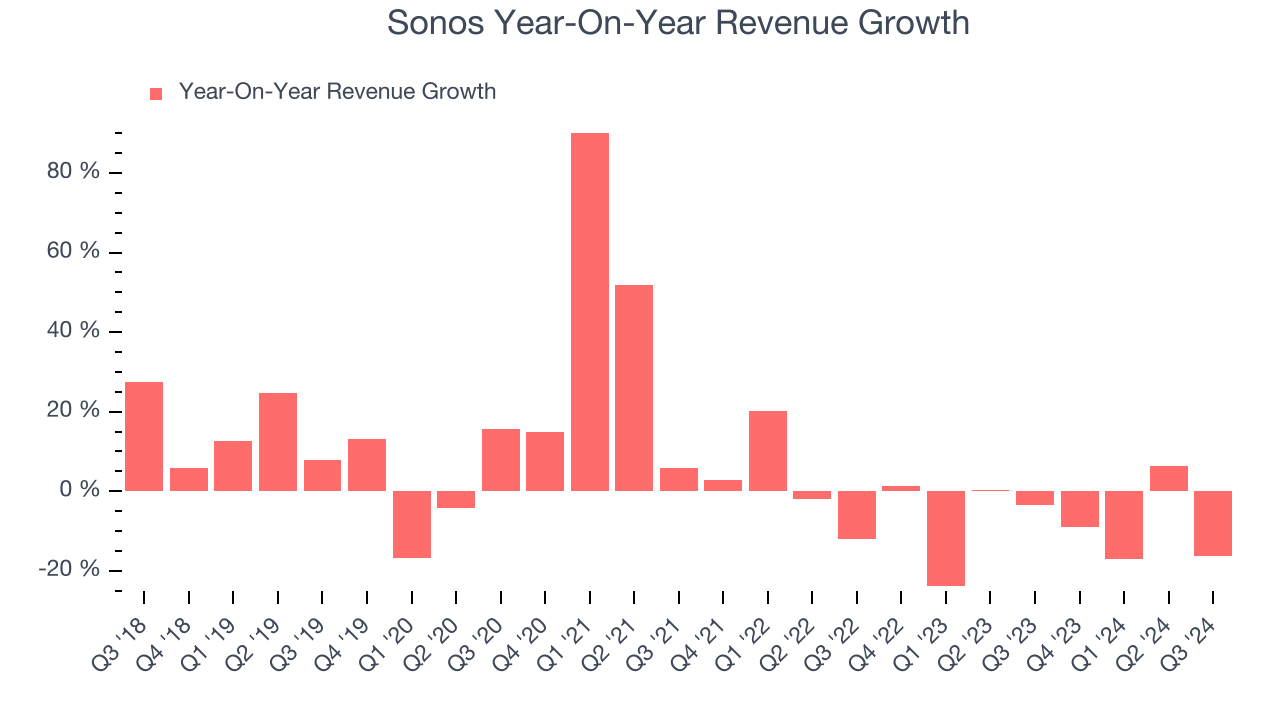

Audio technology Sonos company (NASDAQ: SONO) beat Wall Street’s revenue expectations in Q3 CY2024, but sales fell 16.3% year on year to $255.4 million. Its non-GAAP loss of $0.18 per share was in line with analysts’ consensus estimates.

Is now the time to buy Sonos? Find out by accessing our full research report, it’s free.

Sonos (SONO) Q3 CY2024 Highlights:

- Revenue: $255.4 million vs analyst estimates of $248.4 million (2.8% beat)

- Adjusted EPS: -$0.18 vs analyst expectations of -$0.18 (in line)

- Adjusted EBITDA: -$22.64 million vs analyst estimates of -$34.11 million (33.6% beat)

- Gross Margin (GAAP): 40.3%, down from 42% in the same quarter last year

- Operating Margin: -27.2%, down from -9.3% in the same quarter last year

- EBITDA Margin: -8.9%, down from 2.1% in the same quarter last year

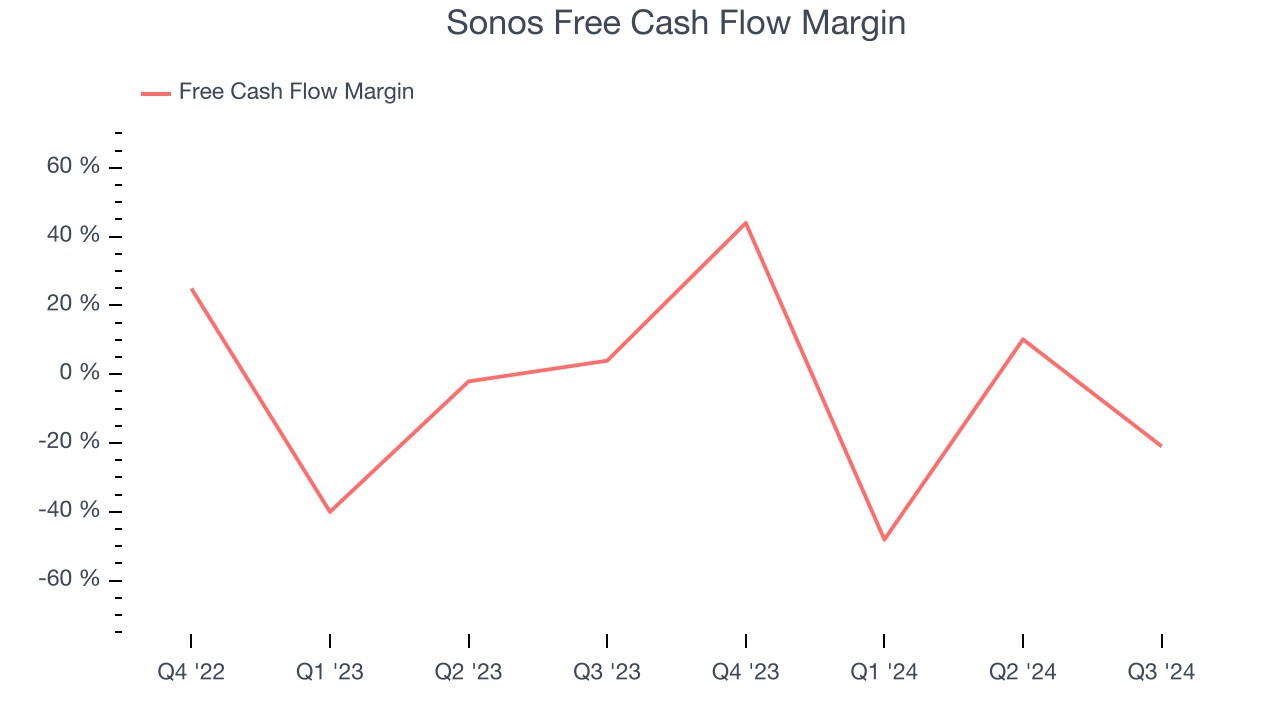

- Free Cash Flow was -$53.5 million, down from $11.99 million in the same quarter last year

- Market Capitalization: $1.70 billion

“Thanks to our team going all-in on our app recovery efforts, we made significant progress in bringing the quality of our software to a level that we’re all proud of, which enabled us to launch our highly anticipated new products, Arc Ultra and Sub 4, in time for the holidays,” Sonos CEO Patrick Spence commented.

Company Overview

A pioneer in connected home audio systems, Sonos (NASDAQ: SONO) offers a range of premium wireless speakers and sound systems.

Consumer Electronics

Consumer electronics companies aim to address the evolving leisure and entertainment needs of consumers, who are increasingly familiar with technology in everyday life. Whether it’s speakers for the home or specialized cameras to document everything from a surfing session to a wedding reception, these businesses are trying to provide innovative, high-quality products that are both useful and cool to own. Adding to the degree of difficulty for these companies is technological change, where the latest smartphone could disintermediate a whole category of consumer electronics. Companies that successfully serve customers and innovate can enjoy high customer loyalty and pricing power, while those that struggle with these may go the way of the VHS tape.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Sonos grew its sales at a sluggish 3.8% compounded annual growth rate. This shows it couldn’t expand in any major way, a sign of lacking business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Sonos’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.9% annually.

This quarter, Sonos’s revenue fell 16.3% year on year to $255.4 million but beat Wall Street’s estimates by 2.8%.

Looking ahead, sell-side analysts expect revenue to decline 5.1% over the next 12 months. While this projection is better than its two-year trend it's tough to feel optimistic about a company facing demand difficulties.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Sonos has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.8%, subpar for a consumer discretionary business.

Sonos burned through $53.5 million of cash in Q3, equivalent to a negative 21% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from Sonos’s Q3 Results

We were impressed by how significantly Sonos blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.8% to $14.33 immediately following the results.

Sonos put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.