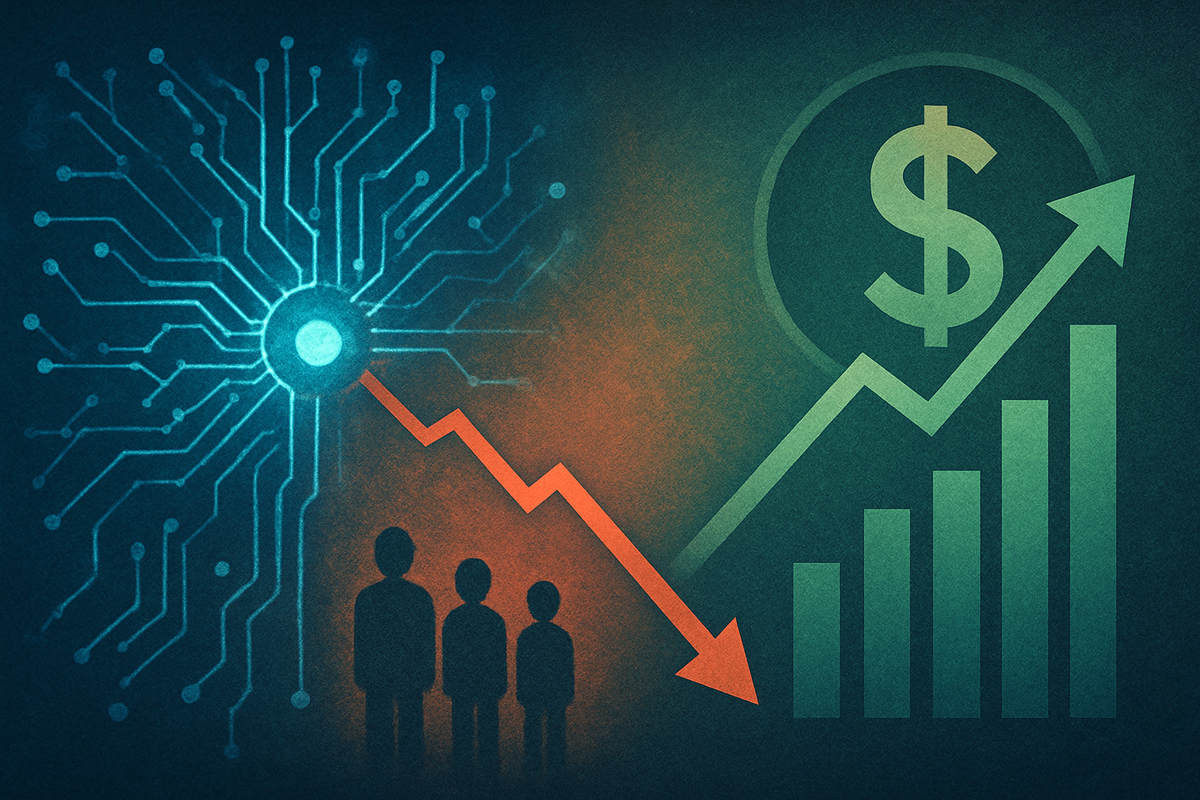

Financial markets are currently navigating a turbulent landscape, grappling with a potent combination of escalating artificial intelligence (AI) concerns and softer-than-expected labor market data. This dual pressure has triggered a significant downturn in equity markets, as investors reassess growth prospects and valuations, particularly within the high-flying tech sector. Simultaneously, the flight to safety has propelled government bond prices upward, driving yields lower, as market participants increasingly anticipate a more dovish stance from the Federal Reserve.

The immediate implication of these developments is a notable shift in market sentiment, with a growing consensus that the Federal Reserve will be compelled to initiate interest rate cuts in 2025. This expectation is fueled by the weakening economic signals emanating from the jobs market, which, when coupled with anxieties surrounding the sustainability and disruptive potential of AI, creates an environment ripe for monetary policy easing aimed at supporting economic stability.

Detailed Coverage of the Event

The recent market turmoil is a direct result of several converging factors, primarily centered on evolving perceptions of AI's economic impact and a clear deceleration in the labor market. The initial unbridled optimism surrounding AI, which propelled many tech stocks to unprecedented highs, has begun to give way to a more cautious, and at times, skeptical outlook. Investors are increasingly scrutinizing the long-term profitability and widespread economic benefits of AI, with some fund managers openly voicing concerns about an "AI bubble" reminiscent of past tech booms. This shift in sentiment has led to profit-taking and increased volatility in major AI-linked stocks, dragging down broader market indices like the Dow Jones Industrial Average and the S&P 500.

Compounding these AI-related anxieties is a stream of weaker-than-anticipated jobs data. Recent employment reports have shown a clear deterioration in the labor market, with metrics such as job creation, wage growth, and worker confidence all signaling a slowdown. This data is critical because it directly impacts the Federal Reserve's dual mandate of maintaining maximum employment and price stability. A weakening labor market puts pressure on the Fed to prioritize employment, thus increasing the likelihood of interest rate reductions. The timeline of events saw a gradual build-up of AI valuation concerns throughout late 2024, which then converged with increasingly dovish jobs reports in late 2024 and early 2025, culminating in the current market reaction.

Key players in this scenario include the Federal Reserve, whose monetary policy decisions are now under intense scrutiny. The market is effectively betting that the Fed will respond to these economic signals by cutting rates, potentially as early as the first half of 2025. Other significant stakeholders include large institutional investors and hedge funds, who are actively repositioning their portfolios, moving out of riskier equity assets and into safer government bonds. Initial market reactions have been characterized by a surge in the Cboe Volatility Index (VIX), often referred to as the "fear index," indicating heightened investor anxiety. U.S. Treasury yields, particularly the benchmark 10-Year and the more rate-sensitive 2-Year, have fallen to multi-month lows, reflecting the increased demand for safe-haven assets and the market's anticipation of lower future interest rates. This "risk-off" sentiment has also impacted other asset classes, including cryptocurrencies, which have seen declines.

Companies Navigating the AI and Rate Cut Crossroads

The current economic currents are creating a distinct bifurcation in corporate fortunes, with some companies poised to thrive amidst the shifts while others face significant headwinds.

Potential Winners are largely found among the AI enablers and beneficiaries of lower interest rates. Despite the broader "AI worries," the fundamental demand for the infrastructure underpinning AI remains robust. Semiconductor companies like Nvidia (NASDAQ: NVDA), Broadcom (NASDAQ: AVGO), and Advanced Micro Devices (NASDAQ: AMD) are expected to continue benefiting from the insatiable need for high-end chips and data center components crucial for AI and cloud computing. Memory chip manufacturers such as Micron Technology (NASDAQ: MU), Samsung Electronics (KRX: 005930), and SK Hynix (KRX: 000660) are also seeing unprecedented demand for High-Bandwidth Memory (HBM) chips, with supplies reportedly sold out well into 2026. Data storage providers like Seagate Technology (NASDAQ: STX) also stand to gain from the massive data generation by AI.

Companies sensitive to interest rate cuts are also set to benefit. The home construction sector, including players like Pultegroup (NYSE: PHM), D.R. Horton (NYSE: DHI), and Lennar (NYSE: LEN), could see a resurgence as lower mortgage rates stimulate homebuying. Small-cap stocks, generally more sensitive to borrowing costs, may also experience a boost. Financial institutions such as JPMorgan (NYSE: JPM) and Goldman Sachs (NYSE: GS) could see increased capital market activity and lending, while utilities like NextEra Energy (NYSE: NEE) and NRG Energy (NYSE: NRG), with their capital-intensive operations, would welcome cheaper borrowing. Companies with manageable high debt loads, such as AT&T (NYSE: T) and Boeing (NYSE: BA), could also see improved earnings as refinancing becomes more affordable. In times of economic uncertainty, "defensive" stocks like Consumer Staples (e.g., Procter & Gamble (NYSE: PG), Coca-Cola (NYSE: KO)) and Healthcare (e.g., Johnson & Johnson (NYSE: JNJ)) are also favored as investors seek stable demand and consistent dividends. Gold mining companies like Barrick Gold (NYSE: GOLD) and Newmont (NYSE: NEM) may also benefit from a flight to safety and a weaker dollar.

Conversely, Potential Losers include some of the very Tech Giants leading the AI charge, due to intense scrutiny over their massive AI investments. While Amazon (NASDAQ: AMZN), Google (Alphabet) (NASDAQ: GOOGL), Meta (NASDAQ: META), and Microsoft (NASDAQ: MSFT) are pouring billions into AI infrastructure, investors are increasingly questioning the return on these capital expenditures. Concerns about a potential "AI bubble" and the challenges of translating AI investments into tangible, high-margin revenue are weighing on these giants. Even companies like OpenAI, despite high valuations, are reportedly incurring significant annual losses, raising questions about financial sustainability if the investment climate shifts. AI startups, heavily reliant on venture capital, are also vulnerable to a tightening funding environment.

Companies highly sensitive to economic slowdowns and weak jobs data are also at risk. The Consumer Discretionary sector, including retailers like Target (NYSE: TGT) and industries like hospitality and leisure, faces reduced consumer spending due to job insecurity and slower wage growth. Manufacturing, travel, tourism, and the restaurant industry are also likely to suffer from decreased demand. Staffing agencies like Robert Half International (NYSE: RHI) and ManpowerGroup (NYSE: MAN) will see their profitability directly impacted by reduced hiring volumes. Some financial institutions, particularly those heavily reliant on net interest margin, could also face pressure if interest rates fall too rapidly.

Wider Significance: A Confluence of Disruption and Adaptation

The interplay of AI worries, weakening jobs data, and the Federal Reserve's anticipated rate cuts represents a period of profound economic adjustment and technological transformation, with far-reaching implications across industries, regulatory landscapes, and competitive dynamics.

Broader Industry Trends are being reshaped by AI's dual nature: immense opportunity coupled with significant anxieties. While AI promises to boost labor productivity by an estimated 15% in developed markets, concerns about job displacement, particularly in routine cognitive tasks, are valid. Federal Reserve Chairman Jerome Powell acknowledges AI's potential for "significant changes" to the labor force. The global investment surge in AI, projected to reach $350 billion in 2025, highlights its transformative power, yet this growth is hampered by challenges like a severe global shortage of High-Bandwidth Memory (HBM) chips and increasing scrutiny over the actual profitability of AI initiatives. The weak jobs data, signaling a broader economic slowdown, could further dampen consumer spending and business investment across sectors, exacerbating the need for companies to adapt.

The Ripple Effects on Competitors and Partners are substantial. Tech giants' aggressive AI push, exemplified by Microsoft (NASDAQ: MSFT), creates a symbiotic relationship with suppliers like Nvidia (NASDAQ: NVDA), but also raises concerns about potential monopolistic tendencies and the long-term diversification of the AI supply chain. A slowdown in enterprise AI adoption could impact the entire AI ecosystem. Meanwhile, weakening demand due to poor jobs data will force companies across all sectors to innovate and find efficiencies to maintain competitiveness. Anticipated Fed rate cuts, while stimulating for some, could also intensify rivalry by making capital cheaper for new entrants and facilitating aggressive expansion or M&A activity among established players.

Regulatory and Policy Implications are rapidly evolving to address these shifts. The EU AI Act, a landmark regulation effective in stages through 2027, is setting a global precedent by defining comprehensive, risk-based rules for AI. It prohibits unacceptable risks, mandates stringent standards for high-risk AI systems (including cybersecurity, data governance, and human oversight), and establishes rules for general-purpose AI models. Non-compliance carries severe penalties, highlighting the growing importance of responsible AI development. The Federal Reserve is carefully navigating this environment. While acknowledging AI's "enormous capabilities," Chairman Powell also cautions that its widespread implementation may take longer than expected. The Fed's Financial Stability Report identifies AI as an emerging risk, particularly the potential for investor enthusiasm to inflate equity markets, warning of sharp losses and broader economic spillovers if sentiment reverses. The Fed is thus balancing its dual mandate amidst technological disruption and uncertain economic signals, wary of asset bubbles fueled by AI optimism.

Historical Precedents offer valuable context. The current AI-driven transformation draws parallels to the Industrial Revolution and the Digital Revolution, both of which dramatically increased productivity but also led to significant job displacement and required a fundamental shift in workforce skills. History generally shows technology as a net creator of jobs in the long run, albeit with often painful short-term transitions for displaced workers. The need for continuous learning, reskilling programs, and supportive policies is paramount to navigate these shifts. The impact of technological growth on interest rates has also been complex, sometimes pushing rates higher due to increased capital demand, but also influenced by factors like income distribution and precautionary savings.

What Comes Next: Navigating the New Economic Frontier

The confluence of AI worries, weak jobs data, and anticipated Federal Reserve rate cuts sets the stage for a dynamic and potentially volatile period for financial markets and the broader economy.

In the short-term, markets are likely to remain highly sensitive to incoming economic data, particularly labor market reports and inflation figures. Any further signs of economic weakness will reinforce expectations for Fed rate cuts, potentially providing a temporary boost to rate-sensitive sectors and continuing the bond rally. However, persistent AI valuation concerns could temper equity gains, especially in the tech sector, leading to increased sector rotation. Companies will face immediate pressure to demonstrate tangible returns on their AI investments, moving beyond pilot programs to proven monetization strategies. The implementation phases of the EU AI Act will begin to exert influence, forcing companies operating in or serving the EU market to prioritize AI governance and compliance.

Looking to the long-term, the trajectory of AI adoption will be a defining factor. While the current "worries" might lead to a more discerning investment approach, the underlying technological advancements are undeniable. Companies that successfully integrate AI to enhance productivity, create new products, and streamline operations, while also demonstrating ethical and responsible AI practices, will emerge as leaders. This will necessitate significant strategic pivots, with businesses potentially re-evaluating their workforce needs, investing heavily in reskilling programs, and forging new partnerships to navigate the evolving AI ecosystem. Market opportunities may emerge in areas such as AI governance solutions, specialized AI hardware beyond current leaders, and innovative applications in sectors previously untouched by advanced AI. Conversely, companies that fail to adapt, either by over-investing in unproven AI or by neglecting the ethical and regulatory landscape, face significant challenges.

Potential scenarios range from a "soft landing" where the Fed successfully engineers rate cuts to stimulate growth without reigniting inflation, leading to a gradual recovery in equities and sustained bond demand. Alternatively, a more severe economic slowdown, potentially exacerbated by AI-driven job displacement or a full-blown "AI bubble" burst, could lead to a deeper recession, prompting more aggressive Fed easing but also prolonged market volatility. Another scenario involves a "productivity boom" where AI's benefits materialize rapidly and broadly, leading to strong economic growth despite initial job market dislocations, potentially even pushing interest rates higher in the long run due to increased capital demand. The outcomes will hinge on the pace of AI integration, the effectiveness of monetary policy, and the resilience of the global economy.

Comprehensive Wrap-Up: A Market in Transition

The current financial landscape is undeniably shaped by the dual forces of evolving AI perceptions and a cooling labor market, compelling the Federal Reserve towards a more accommodative monetary policy in 2025. The key takeaway is a market in transition, moving from an era of aggressive rate hikes to one of anticipated easing, all while grappling with the profound, yet uncertain, impact of artificial intelligence.

For the market moving forward, investors should anticipate continued volatility, particularly as new economic data is released and as companies report on their AI initiatives. The "flight to quality" seen in bond markets is likely to persist until there is clearer evidence of economic stabilization or a definitive pivot from the Fed. Equity markets will likely favor companies with strong balance sheets, clear pathways to AI monetization, and those in defensive sectors or poised to benefit directly from lower interest rates. The performance differential between AI enablers and AI implementers (especially those struggling with ROI) could widen.

The lasting significance of this period lies in its potential to redefine economic growth drivers and corporate strategies. AI, despite its current "worries," remains a transformative technology, but its integration will be complex, requiring careful navigation of ethical, regulatory, and economic challenges. The Federal Reserve's response to weakening jobs data underscores the critical role of monetary policy in moderating economic cycles, but its effectiveness will be tested by the unique dynamics of AI-driven change.

What investors should watch for in the coming months includes the Federal Reserve's communications for clearer signals on the timing and magnitude of rate cuts, further labor market reports for signs of stabilization or continued weakening, and corporate earnings calls for insights into AI investment returns and integration progress. Additionally, global regulatory developments around AI, particularly the enforcement of the EU AI Act, will be crucial in shaping the operational environment for tech companies.

This content is intended for informational purposes only and is not financial advice