Memory chips are at the center of today’s digital world, powering everything from smartphones and laptops to the massive data centers running artificial intelligence (AI). One company deeply tied to this backbone is Micron Technology (MU), a leading maker of DRAM memory and NAND flash storage. As demand for AI infrastructure rose, a global memory shortage followed. And this pushed Micron into the spotlight, sending its stock soaring over 300% over the past year.

The next catalyst arrives on March 18, when Micron reports its fiscal second-quarter results after the bell. Investors are closely watching the update as memory prices have surged sharply in recent months, fueled by intense AI-driven demand from hyperscale data centers.

Analysts at Citi believe the momentum may still have room to run. The bank raised its price target on MU stock, citing stronger-than-expected memory pricing. Fueled by booming demand from data centers and enterprise SSDs, DRAM and NAND prices are projected to surge. And analysts say AI could trigger a longer memory cycle, much like the PC boom of the 1990s, potentially extending Micron’s run.

With Citi reiterating a “Buy” rating, investors may also want to take a closer look, especially since the stock still trades at a relatively attractive valuation.

About Micron Stock

Headquartered in Boise, Idaho, semiconductor powerhouse Micron Technology operates as the only U.S.-based manufacturer of DRAM, NAND, and NOR memory technologies. Micron designs and fabricates high-performance memory and storage solutions under the Micron and Crucial brands for AI, data centers, mobile, automotive, and industrial markets. The company currently has a market cap of approximately $438.2 billion.

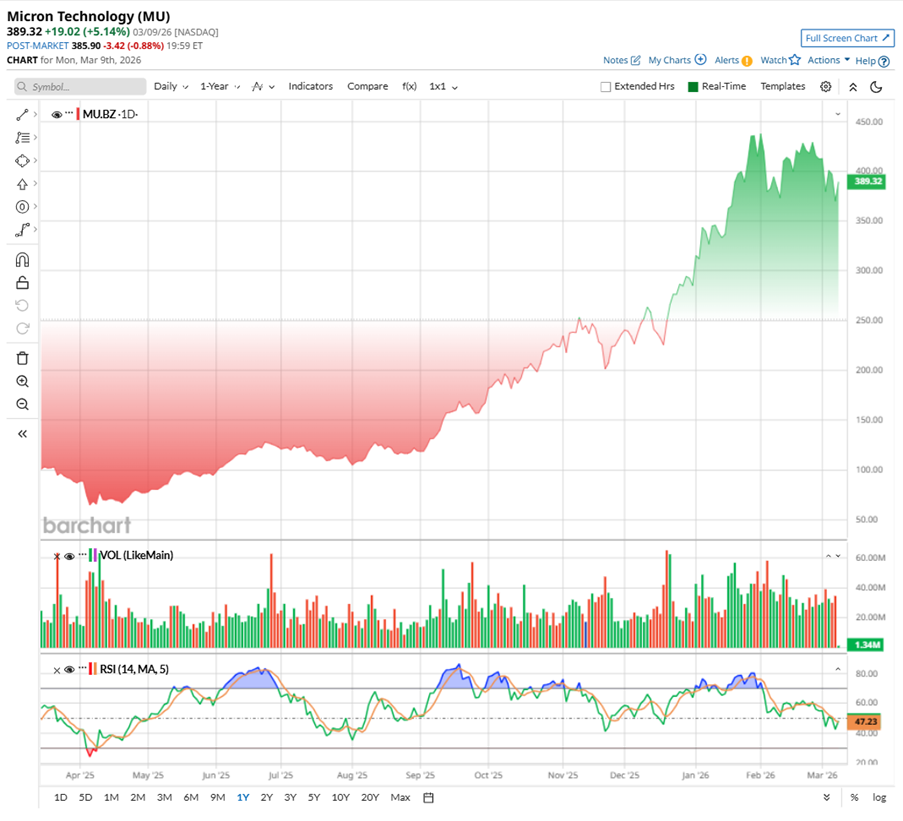

The rally in Micron Technology’s shares has been nothing short of remarkable. Over the past decade, the chipmaker skyrocketed more than 3,600%, riding multiple memory cycles. The latest surge pushed the stock to a record $455.50 in January, before it cooled about 10% from that peak. Over the past five days, MU is down 7.8%.

Even with the recent pause, the bigger picture still looks powerful. MU remains up roughly 370% over the past 52 weeks and has climbed 192.4% in just the last six months. Much of that momentum comes from the explosive growth in AI infrastructure, which requires massive amounts of memory and storage – areas where Micron is deeply entrenched. Tighter supply across the global memory market has also helped push prices higher, strengthening margins and boosting earnings expectations.

From a technical standpoint, the stock simply needed a breather after such a strong run. The 14-day RSI, which had entered overbought territory in January, has eased to 53.59, suggesting the stock is cooling off after a powerful run rather than reversing trend.

Valuation-wise, Micron Technology trades at about 10.74 times forward adjusted earnings, below semiconductor peers and its historical average. Despite concerns around memory cycles and supply swings, strengthening margins, rising cash flows, and solid AI-driven demand suggest the stock still looks reasonably priced. Plus, the company has been paying dividends for four consecutive years.

Micron’s Q1 Results Surpassed Projections

Micron delivered a standout first quarter for fiscal 2026 on Dec. 17, generating a revenue of $13.6 billion, up a striking 56.7% year-over-year (YOY), while non-GAAP EPS grew to $4.78 from last year’s quarter’s $1.79. Both comfortably cleared Wall Street’s bar.

DRAM remained the company’s biggest growth driver, with the segment revenue surging 69% YOY to $10.8 billion as demand from data centers and AI workloads continued to climb. Also, NAND flash contributed, generating $2.7 billion, up about 22% annually, signaling improving demand and firmer pricing across the memory market.

The strength was clearly reflected across Micron’s business units. The Cloud Memory Business Unit (CMBU) led the charge, delivering a record $5.3 billion in revenue, nearly doubling from a year earlier. Meanwhile, the Core Data Center segment posted $2.4 billion in revenue, rising sharply as AI-driven infrastructure spending accelerated.

Mobile and Client segment revenue reached $4.3 billion, supported mainly by stronger pricing despite softer shipment volumes. Even Micron’s Automotive and Embedded business, often a quieter contributor, hit a record $1.7 billion in revenue, with improving shipments and better pricing helping lift margins to 45%.

Cash flow capped a stellar quarter for Micron Technology. Adjusted FCF surged to a record $3.9 billion, topping its previous 2018 high by over 20%. The company also closed the quarter with $12 billion in cash, marketable investments, and restricted cash, giving it ample room for expansion.

Looking ahead, management expects strong momentum as tight supply and robust AI-driven demand keep memory markets firm, possibly beyond 2026. Micron is negotiating multiyear customer contracts, ramping advanced technology nodes, and expanding cleanroom capacity to boost supply.

While Q2 reports are set to release next week, the management forecasts revenue between $18.3 billion and $19.1 billion, EPS between $8.22 and $8.62, and gross margins near 68% (+/-1%). This represents a sharp leap from last year’s figures, signaling a powerful industry upcycle.

Meanwhile, analysts monitoring the company remain upbeat, expecting Micron to generate roughly $19.1 billion in revenue in Q2, while EPS could jump sharply to about $8.52, marking a 504% YOY growth. Looking further down the road, forecasts remain just as ambitious. Fiscal 2026 EPS is projected to be around $34.51, up 349% annually before surging by nearly 42% YOY to $48.98 in fiscal 2027.

What Do Analysts Expect for Micron Stock?

Ahead of Micron’s Q2 report, analysts appear increasingly bullish on MU stock. Citigroup’s analysts, led by Atif Malik, recently reiterated a “Buy” rating and raised the price target to $430 from $385. Their confidence largely stems from stronger-than-expected memory pricing so far this year.

Citi noted that YTD memory prices have climbed well above market expectations, prompting the firm to raise its estimates for Micron’s February and April quarters. The bank’s global memory analyst, Peter Lee, now expects DRAM average selling prices to surge 171% YOY in 2026, fueled by relentless demand from AI-focused data centers. Meanwhile, NAND prices could jump 127% annually, supported by rising demand for enterprise solid-state drives.

Analysts say the bigger debate among investors is whether the market has entered a longer memory supercycle, similar to the surge seen during the 1990s Windows PC boom. Malik and his team examined past cycles and compared MU stock’s performance with DRAM pricing trends. They anticipate that if pricing strength continues, MU’s rally could extend through the year, though gains may slow somewhat after the sharp price spike seen earlier in 2026.

Meanwhile, optimism is not limited to Citi. Analysts at Susquehanna turned more bullish, raising their price target on Micron to $525 from $345 while maintaining a “Positive” rating on the stock. Heading into Micron’s results, the brokerage firm updated its forecasts, lifting estimates as memory prices have been running stronger than expected. It sees DRAM prices leading early in 2026, while NAND could catch up and outperform later in the year as pricing trends evolve.

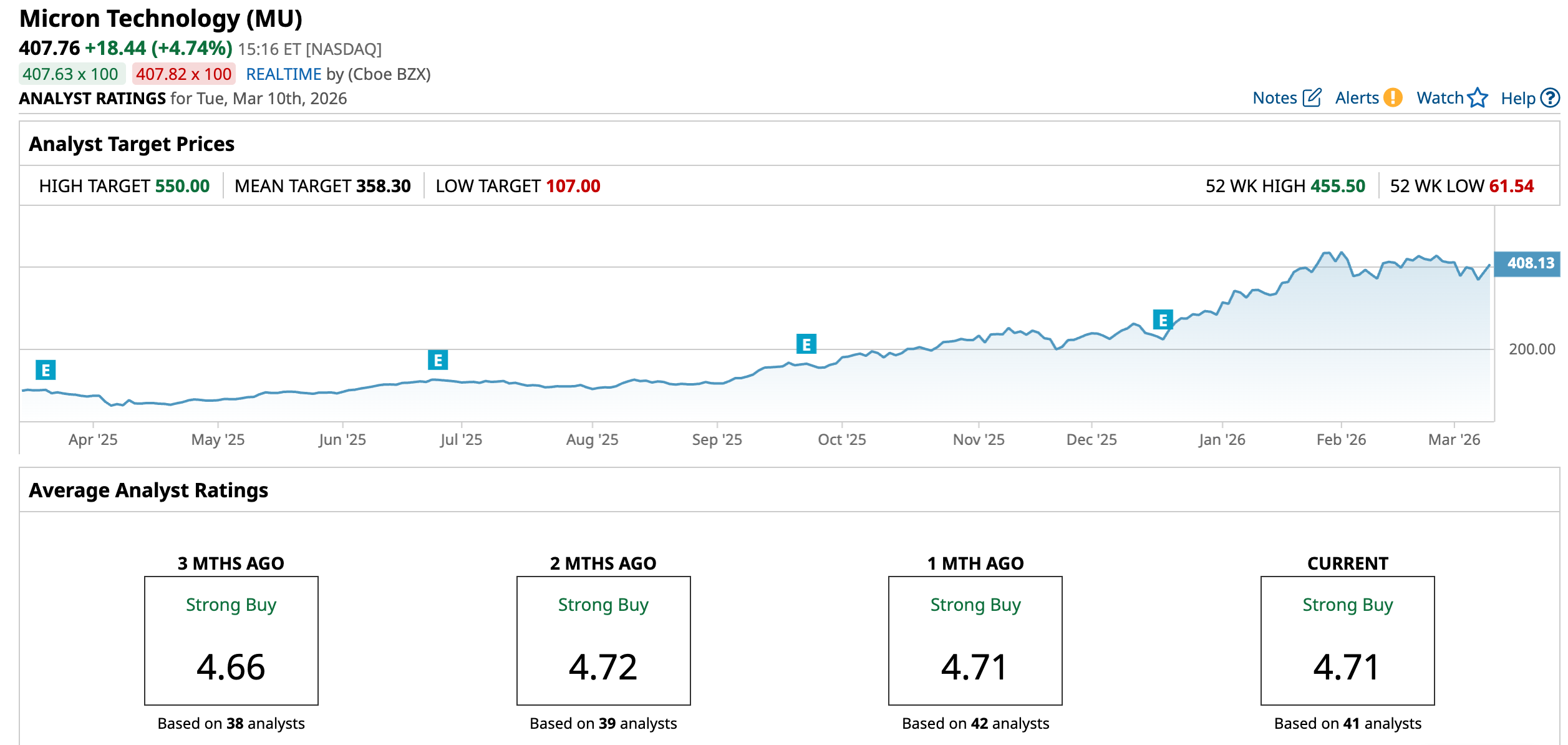

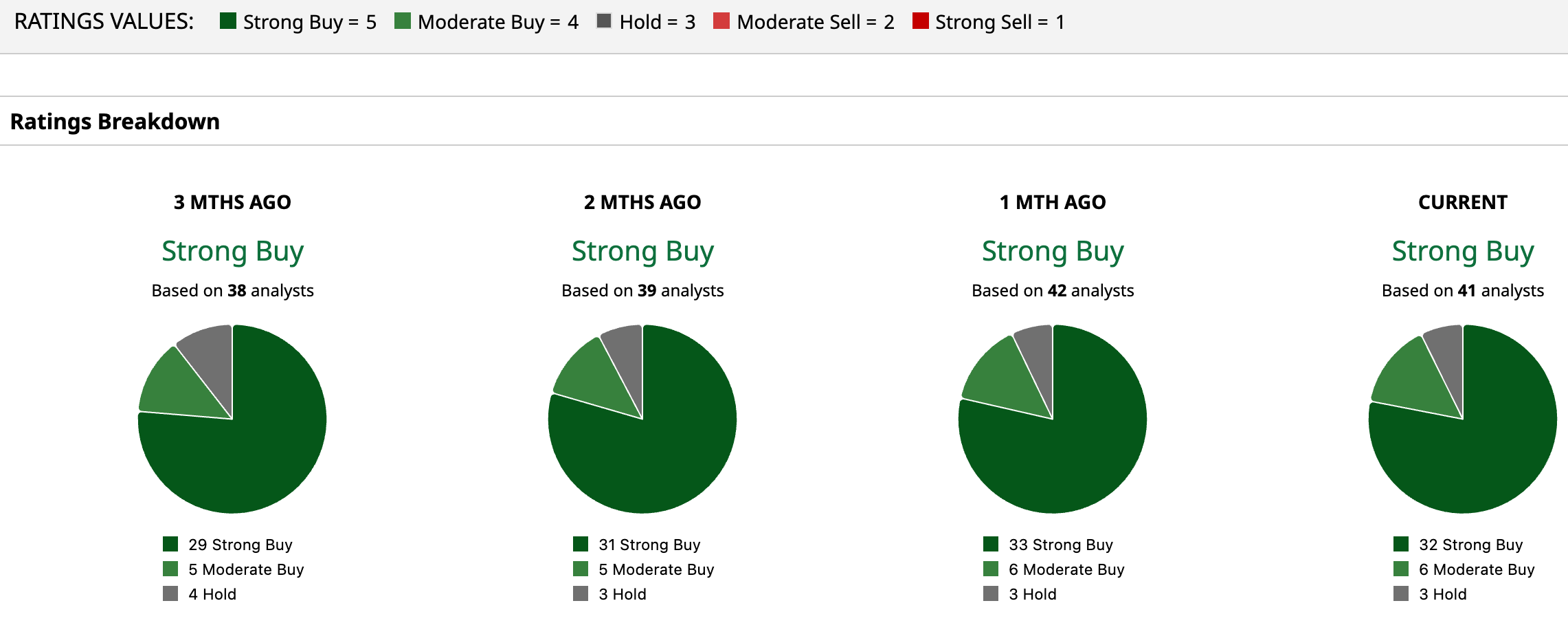

Wall Street’s optimism in Micron is strong. MU has a consensus “Strong Buy” rating overall. Out of 41 analysts covering the AI chip stock, 32 recommend a “Strong Buy,” six advise a “Moderate Buy,” and three analysts stay cautious with a “Hold” rating.

Interestingly, Micron’s rally has already pushed the stock past the average price target of about $358.30. Stifel’s Street-high target of $550 implies roughly 34.9% upside ahead. For many on Wall Street, that signals the AI-powered memory boom may still have plenty of runway.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart