Shares of Palantir Technologies (PLTR) are under pressure, dropping more than 38% from its 52-week high of $207.52. The decline reflects valuation concerns. Palantir's stock had been trading at a significant premium compared to its peers and large tech giants, leaving little room for disappointment. As concerns about competition and potential disruption surfaced, sentiment shifted, and the stock retreated sharply from its peak.

Despite the pullback, demand for Palantir’s Artificial Intelligence Platform (AIP) remains solid. The company continues to add new customers, and existing clients are expanding their spending. That combination of customer growth and higher average revenue from its large customers supports the case for continued revenue momentum into 2026.

Against this background, should investors buy PLTR stock or still stay away?

Palantir to Deliver Strong Growth in 2026

Palantir has entered 2026 with solid revenue momentum and expanding operating leverage. Over the last several quarters, the company’s top line has accelerated steadily. Revenue rose 36% year-over-year (YoY) in the fourth quarter of 2024, and growth continued to build throughout 2025, reaching approximately 70% YoY in the fourth quarter of 2025. This trend points to consistent, broad-based demand across both its government and commercial businesses.

The outlook for 2026 remains solid, led primarily by the significant demand in the U.S. market. Demand for the company’s AIP continues to scale, driven by higher adoption across federal agencies and enterprises. PLTR’s U.S. business revenue surpassed $1 billion in a single quarter for the first time in Q4. Within that segment, U.S. commercial revenue rose 137% YoY and 28% sequentially, while U.S. government revenue increased 66% YoY and 17% sequentially. These growth rates point to strong pipeline conversion and expanding share.

Contract activity further supports its investment case. Palantir reported its highest total contract value quarter on record at $4.3 billion in Q4, signaling solid demand entering 2026. Customer count expanded 34% YoY and 5% sequentially to 954 customers, reflecting both new client acquisition and broader platform penetration. Revenue concentration among large accounts is also trending higher, with trailing 12-month revenue from the top 20 customers rising 45% YoY to an average of $94 million per customer.

Large deal flow remains robust. During the fourth quarter, Palantir closed 180 contracts valued at $1 million or more, including 84 deals exceeding $5 million and 61 deals above $10 million. The mix of multi-million-dollar contracts strengthens revenue durability and enhances visibility for the coming quarters.

Palantir projects 2026 revenue of about $7.19 billion, implying 61% YoY growth. The forecast reflects continued acceleration in the U.S. market and sustained demand for AIP. As revenue scales, operating leverage is improving, with margin expansion contributing to stronger profitability. Wall Street analysts currently forecast earnings of $1.05 per share in 2026, a projected 67% YoY increase. They expect earnings growth to continue in 2027, with an additional 43.8% increase.

Overall, accelerating demand, record contract activity, expanding revenue from large customers, and improving margins position Palantir for another year of strong financial performance in 2026.

Should You Buy PLTR Stock or Stay Away?

PLTR stock has pulled back from its 52-week high. However, the company’s underlying business momentum remains solid. Revenue growth has accelerated, particularly in the U.S. commercial segment; contract values are hitting record levels, and customer expansion remains steady. With management guiding for 61% revenue growth in 2026 and analysts projecting strong earnings expansion, the company appears to be translating AI demand into solid financial performance.

Given the recent decline, PLTR stock trades at a price-to-sales multiple of 71.8. While the valuation is still high, the continued momentum in its business in the coming quarters could support its share price.

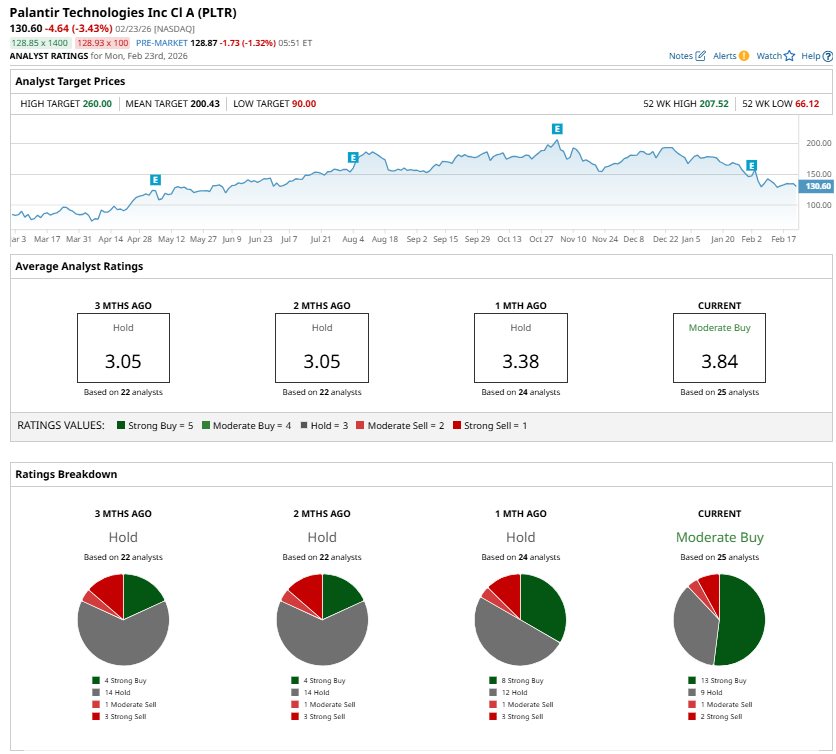

Wall Street analysts currently rate Palantir a consensus “Moderate Buy.”

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart