The AI data center market is projected to surge from $236.44 billion in 2025 to $933.76 billion by 2030, compounding at 31.6% annually. This growth reflects soaring demand for compute, storage, cooling, and power infrastructure as AI workloads spread across industries from finance to healthcare and manufacturing. That kind of expansion also means a sharp step‑up in round‑the‑clock electricity needs, putting energy supply at the center of the AI story.

This is where the conversation shifts from chips and cloud platforms to natural gas and pipelines. AI data centers need reliable power, and gas‑fired generation is still doing much of the heavy lifting as new facilities come online. Strategists at Morgan Stanley now argue that select gas producers and midstream operators are quietly becoming some of the most direct beneficiaries of this buildout.

Two names stand out in that framework as top ways analysts like to tap this theme without owning another tech stock. Could these energy names end up capturing more of the AI boom than many realize right now? Let’s dive in.

Top Analyst Stock #1: EQT Corp. (EQT)

EQT Corporation (EQT) is a roughly $37.8 billion natural gas producer headquartered in Pittsburgh, Pennsylvania, focused on Appalachian gas and increasingly on power demand from AI data centers. The stock offers a forward annual dividend of $0.66 per share, implying a yield of about 1.1%.

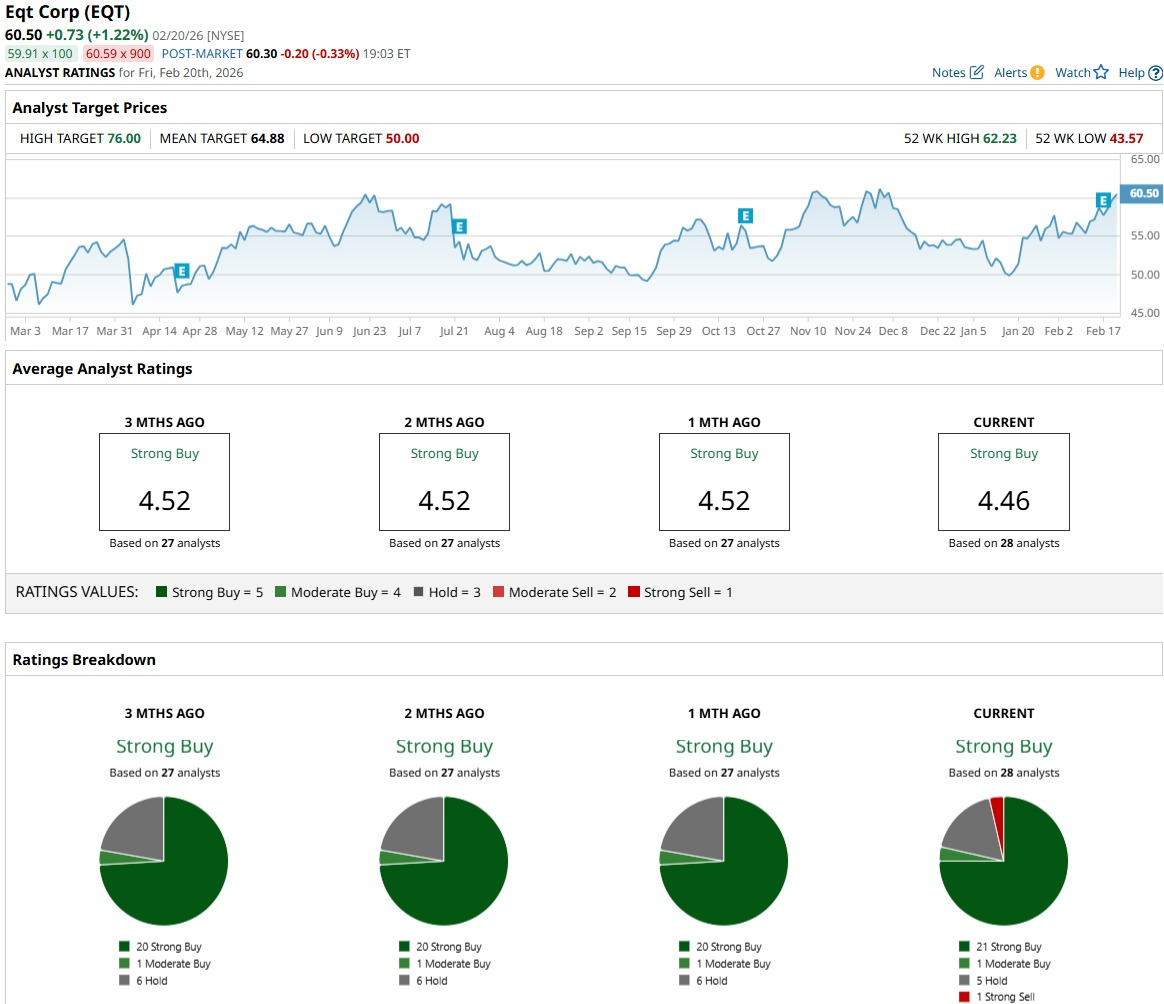

EQT trades at $60.50 as of Feb. 20, up about 13% year‑to‑date (YTD) and roughly 15% over the past 52 weeks.

This pricing reflects a forward P/E of 16.03x and a price‑to‑book ratio of 1.34x versus sector medians of 15.73x and 1.77x, indicating a modest earnings premium for its growth profile with a discount on book value relative to peers.

EQT’s fourth‑quarter and full‑year 2025 results, released on Feb. 17, showed adjusted EPS of $0.90 versus a $0.73 consensus, a 23.3% upside surprise. This beat was driven by sales volumes of 609 Bcfe, which came in above the high end of guidance thanks to stronger well performance, system pressure optimization, and lower‑than‑expected price‑related curtailments.

The company recently exercised an option to purchase part of Con Edison’s interest in the Mountain Valley Pipeline (MVP) venture, gaining additional exposure to the mainline system and associated compression assets tied to the MVP Boost expansion project. That deal tightens EQT’s grip on critical infrastructure that can move molecules toward regions where data center build‑outs are accelerating.

EQT’s first‑quarter 2026 EPS is projected at $1.35 versus $1.18 in the prior‑year quarter, while full‑year 2026 EPS is estimated at $3.80 compared with $3.05 in 2025, implying expected growth of about 14.4% and 24.6%, respectively. The stock carries a consensus “Strong Buy” rating from 28 analysts, with an average price target of $64.88, which represents roughly 7.3% upside from its current price.

Top Analyst Stock #2: TC Energy (TRP)

TC Energy (TRP) is a Calgary‑based energy infrastructure company that owns and operates large natural gas pipeline networks across Canada, the U.S., and Mexico. The nearly $65 billion equity is supported by a forward annual dividend of $2.48 per share for a yield of about 4%, with the board approving a 3.2% increase for the quarter ending March 31.

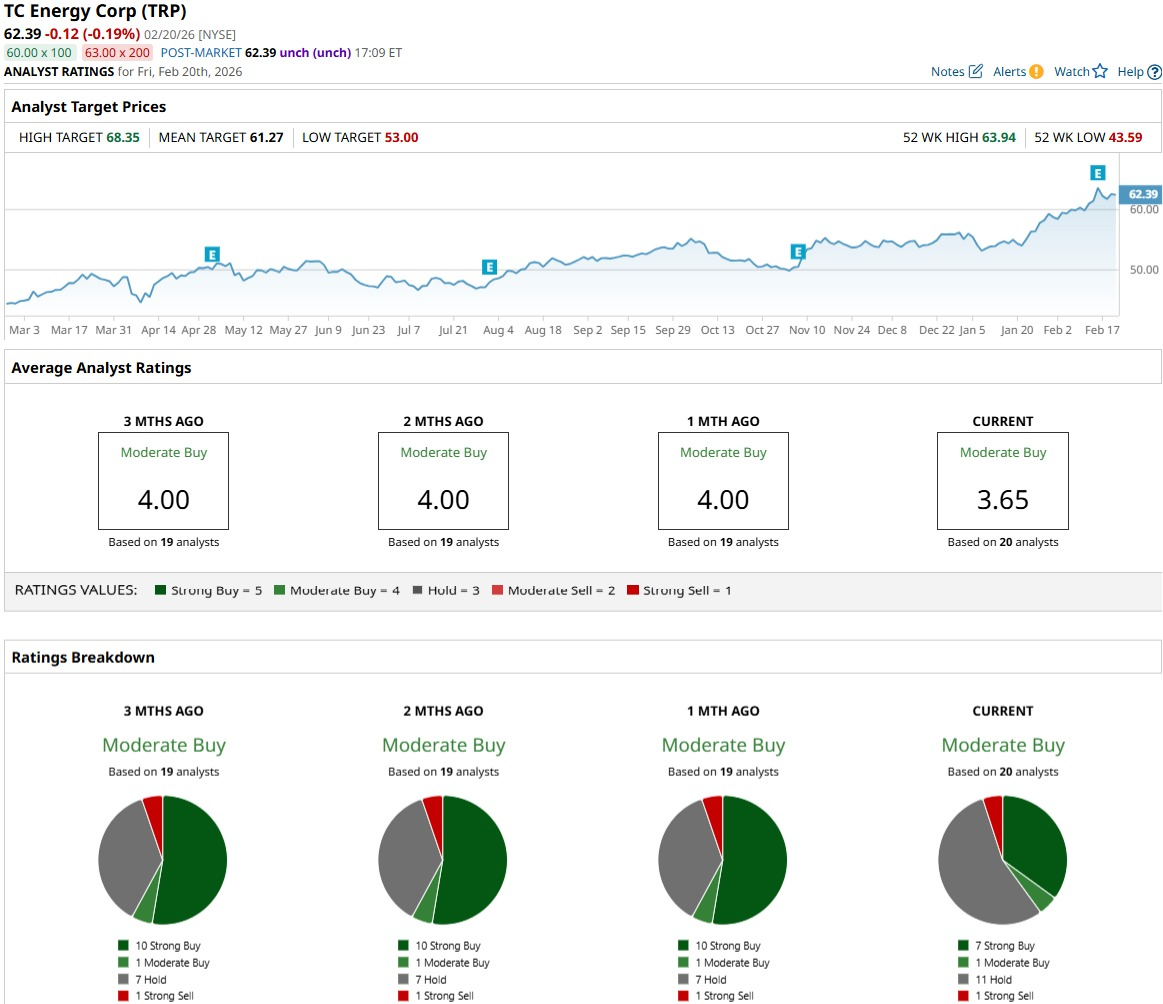

At $62.39 as of Feb. 20, TRP stock is up about 13.4% YTD and roughly 37% over the past 52 weeks.

This pricing translates into a trailing P/E of 24.90x and a price‑to‑sales ratio of 5.97x versus sector medians of 15.50x and 1.63x, signaling that investors are paying a premium.

TC Energy's latest earnings report shows why TRP sits in the middle. It reported fourth-quarter and full-year 2025 numbers on Feb. 13, with EPS of $0.70 versus a $0.65 estimate, a 7.7% positive surprise. The quarter generated revenue of $2.99 billion, while full-year revenue was $10.91 billion and profit totaled $2.52 billion, or $2.34 per share.

This performance ties directly to very high system utilization, as the U.S. natural gas network also saw strong demand, with daily average flows of 29.6 Bcf/d, up 9.5% year‑over‑year (YoY), and record deliveries of 39.9 Bcf on Jan. 29, 2026.

TC Energy’s footprint is feeding directly into growth projects, most notably the Feb. 9 launch of a non‑binding expansion open season on the Crossroads Pipeline system for up to 1.5 Bcf/d of additional capacity aimed at Northern Indiana, Illinois, Iowa, and South Dakota. This project is designed to serve recently announced power generation and data center developments in the U.S. Midwest and is scheduled to close in mid‑March 2026.

TC Energy’s next earnings release is scheduled for May 7, 2026, with first-quarter EPS estimated at $0.75 versus $0.66 in the prior-year period. That implies roughly 13.6% YoY growth, while 2026 EPS is projected at $2.81 compared with $2.51 in 2025, or about 12% growth.

The consensus on TRP stock from 20 analysts is a “Moderate Buy” rating with an average price target of $61.27, which sits about 2% below its current share price.

Conclusion

Both EQT and TRP are anchored to a clear thesis around the energy backbone of AI, with one securing a scalable gas supply and the other expanding high‑utilization pipeline routes to data center hubs. If AI data center construction and related power projects keep progressing, the risk‑reward for both stocks looks tilted toward gradual upside, with TRP leaning more to income stability and EQT to volume and price torque. The key question is how much anticipated demand becomes long‑term contracts and fully funded infrastructure.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart